23

Meanwhile, smaller “insurtech”

companies are starting from scratch

with disruptive business models.

The Texas-based startup, Bestow,

underscores the potential.

It claims that 85 percent of

Americans believe they should have

life insurance, but only 41 percent

do. Why not? Consumers don’t

understand it, don’t like the perceived

cost or the hassle of purchasing.

That’s why Bestow is readying what

it says will be the “consumer-first” life

insurance solution driven by analytics

and technology.

Look for many more such

announcements, and not only

from the insurance industry but

from technology and consumer

innovators, too.

Bestow, for instance, describes itself

as a “band of finance experts, tech

specialists, and data nerds.”

Big Disasters

Needs Big Helpers

Disruptive technologies and

innovators will help push the rest

of the industry forward. But with

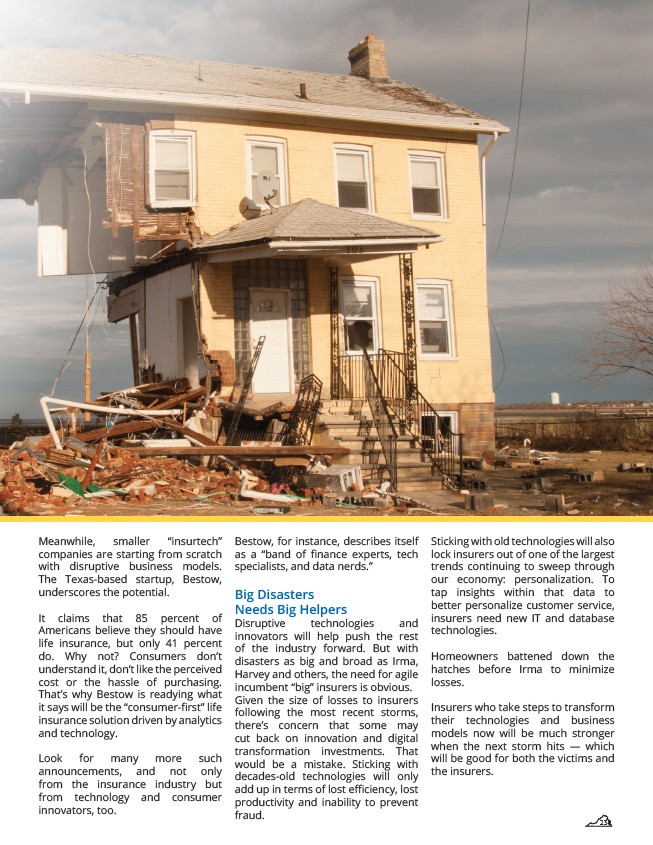

disasters as big and broad as Irma,

Harvey and others, the need for agile

incumbent “big” insurers is obvious.

Given the size of losses to insurers

following the most recent storms,

there’s concern that some may

cut back on innovation and digital

transformation investments. That

would be a mistake. Sticking with

decades-old technologies will only

add up in terms of lost efficiency, lost

productivity and inability to prevent

fraud.

Sticking with old technologies will also

lock insurers out of one of the largest

trends continuing to sweep through

our economy: personalization. To

tap insights within that data to

better personalize customer service,

insurers need new IT and database

technologies.

Homeowners battened down the

hatches before Irma to minimize

losses.

Insurers who take steps to transform

their technologies and business

models now will be much stronger

when the next storm hits — which

will be good for both the victims and

the insurers.