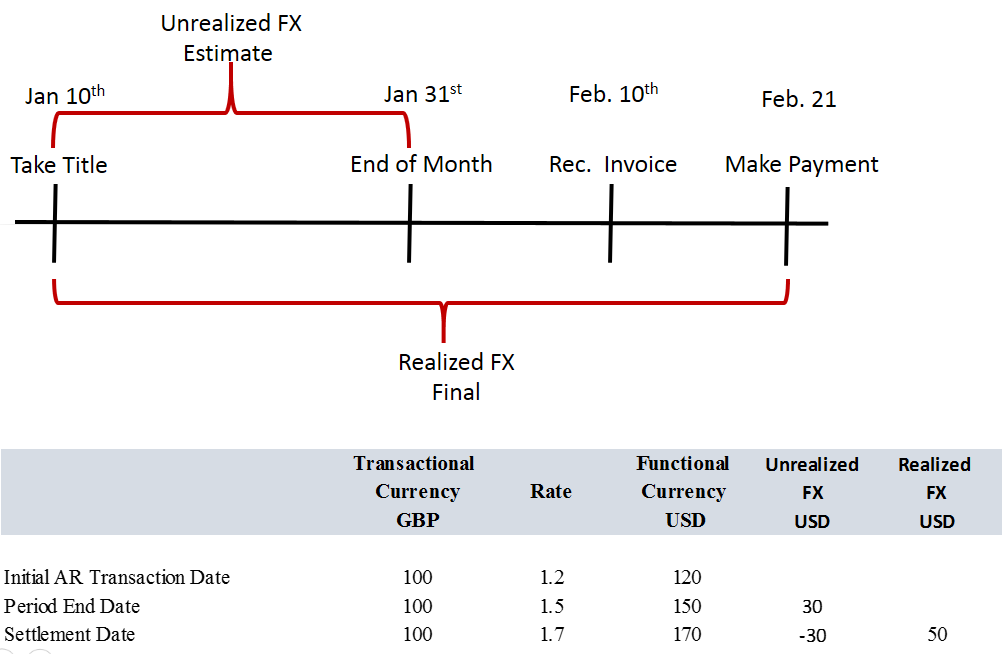

The following image illustrates the time line for an accounts payable transaction, and shows calculations applicable to unrealized foreign exchange gain for this transaction and the realized foreign exchange gain for this transaction:

In this example, 100 GBPs (Great Britain pounds) for an accounts receivable transaction is converted to 120 USDs (United States dollars) on January 10th, the initial transaction date. At the end of the period on January 31st, the 100 GBPs are worth 150 USDs. Consequently, the amount of functional currency for the initial transaction in accounts receivable is increased by 30 USDs. The offset to this increase is the account on the income statement for the unrealized foreign exchange gain.

When the transaction is settled on February 21st, the 100 GBPs are worth 170 USDs. Consequently, the previous entry for the unrealized foreign exchange gain is reversed because the amount for this entry is an estimate. Also, the amount of the functional currency for the initial transaction in accounts receivable is increased by 50 USDs. The offset to this increase is the account on the income statement for the realized foreign exchange gain.