21 / 88

21 / 88

• Geely Emgrand, meanwhile, also

saw sales increase y-o-y in FY14,

capturing a 7.8% share of the mar-

ket, up from 7.3% the previous year.

• Mazda continues to report increas-

es in unit sales, revenues and con-

tributions to the LOB’s gross profit.

• The Passenger Cars After-Sales divi-

sion improved in FY14 in terms of

revenue, gross profit and customer

satisfaction, as expected given GB

Auto’s sustained investment in soft

skills, technical knowledge and

retention. The division is expected

to further increase its contribution

in 2015 and 2016 as the company

looks to make full use of new After-

Sales facilities on the Ring Road and

Suez Road in particular. Moreover,

a sharp increase in Units in Op-

eration (UIO) from both 2014 sales

and anticipated sales in 2015 will

bolster performance of After-Sales.

Iraq

• On a full-year basis, gross profits for

Iraqi operations dropped 10.1% y-

o-y, while the division’s After-Sales

operations report a y-o-y growth

rate of 24.2%.

• GB Auto continues to operate in

Iraq despite adverse conditions,

and is exploring contingency

plans that should see operations

remain steady in 2015, the secu-

rity situation permitting. Opera-

tions in central and southern Iraq

have been relatively less affected

by challenges in the second half

of 2014 and into 2015 than were

operations in the north, GB Auto’s

traditional base of strength in

Iraq. As with all other companies

operating in the Iraqi market, GB

Auto has reasonably low visibility

at present on the expected pace of

operations in 2015.

Algeria

• After successfully learning the intri-

cacies of and settling into this unique

market, management continues to

target a modest increase in sales in

the near term and a gradual ramp

up in the medium term. New models

are filtering into themarket following

the liquidation of an overstock of less

popular models, and they have thus

far been well-received by consumers.

Libya

•

Conditions in Libya are increasingly

volatile and management is simply

maintaining its foothold in the coun-

try so that GB Auto will be in position

to capitalize on a recovery when the

political and security situation stabi-

lizes. In themeantime, it is noteworthy

that the company does not have any

personnel in Libya. All inventory pres-

ently in Libya remains fully insured.

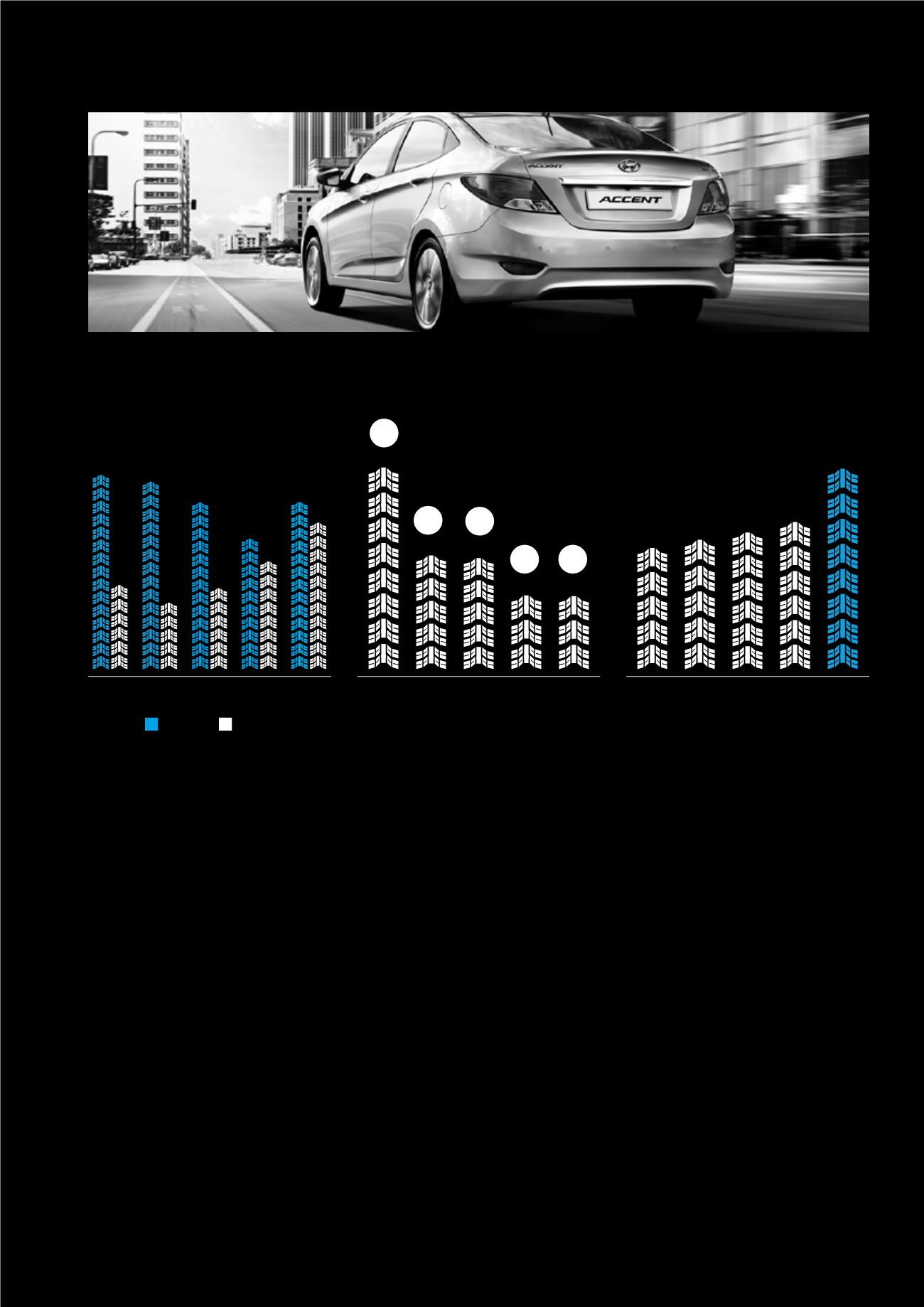

Revenues by Year

(LE million)

2010 2011 2012 2013

2014

Segmentation of the Egyptian

Passenger Car Market*

(Units sold and % Market Share as of

Year-End 2014)

Hyundai

Nissan

Chevrolet

Kia

Geely

Emgrand

GB Auto Sales Volume Across

All Brands and Markets

(Vehicle Units)

5,383.0

5,741.9

6,072.3

6,536.9

8,909.9

2010 2011 2012 2013 2014

25,320 24,737

16,410 16,265

44,935

51,924

50,103

44,562

34,869

17,749

21,598

28,764

44,645

39,135

22,439

CBU CKD

21.6

%

12.2

%

11.9

%

7.9

%

7.8

%

* Source: Automotive Marketing Information Council (AMIC). Please note that AMIC figures are based on individual companies willingly contributing /

reporting their sales and that GB Auto cannot check the full accuracy of these or guarantee that all companies operating in Egypt report to AMIC.

Ghabbour Auto | 2014 ANNUAL REPORT

19