Fundamental Value had its best year ever in 2021, returning 48.5% net of fees vs 28.7% for the S&P 500. The strategy has now compounded at 25.9% net of fees since inception in June of 2016, beating the market by 800 bps annually over more than half a decade. While this level of absolute returns is unlikely to be sustainable, we are as confident as ever in our ability to significantly outperform a still richly-valued equity market.1

Market commentary

It was only four months ago when we published Part III: Apex of a Bubble. We said that the US capital markets were mired in an “everything bubble,” presaging real returns that investors would find severely disappointing – and likely negative – for many years to come. And we predicted an imminent top and a proximate cause:

We believe inflation is likely to be the catalyst that ultimately pops the everything bubble. If we are correct, eventually the Fed will have to reverse course, tightening policy and raising interest rates. When this happens, investors who have speculated in low or no-yielding assets like SPACs, high-flying growth stocks, and NFTs may find their portfolios permanently impaired.

Since we wrote that letter, incoming data has confirmed our macroeconomic predictions. Back in September, traders were predicting less than one interest rate hike for 2022; now they are pricing in nearly five.

2 The idea that inflation is transitory now seems risible. Consumer price inflation is

running at 7.1%, a 40-year high, up sharply from 5.2% in September. The Fed has pivoted to a much more hawkish tone.

As we anticipated, the most speculative securities have been decimated. The ARK Innovation ETF, the standard-bearer for valuation-agnostic, meme-chasing investors everywhere, has plummeted 42% in the four months since we published Part III. Despite more than tripling in 2020, recent declines have

eliminated all of ARKK’s outperformance since the pandemic began. And because investors predictably piled money in near the top, ARKK holders have massively

underperformed the ETF and in fact have experienced deeply negative dollar-weighted returns.

The broader market has, somewhat surprisingly, fared well. The S&P 500 is down about 10% from its all-time high, but that is misleading – it is essentially flat since our letter. The fourth quarter saw a phenomenal 10% gain despite the mounting evidence of trouble ahead. Those returns evaporated in just a few days after the top on January 3rd.

As painful as the recent drawdown has been, the everything bubble has not popped. It has barely started deflating. Monetary tightening has not even begun; despite a hawkish turn in rhetoric, the Fed is still comically behind in action. Inflation is at a 40-year high. GDP

grew 5.7% in 2021, the fastest rate since 1984. The unemployment rate of 3.9% is one of the lowest levels ever recorded. Usually there are millions more unemployed persons than job openings; today, job openings

exceed unemployed persons by 2.8 million.

Nonetheless, overnight interest rates remain at zero – utterly inappropriate for a high inflation, high growth, low unemployment economy. And not only has the Fed yet to begin reducing its gargantuan balance sheet, it is actively engaged in quantitative easing at this very moment. While real interest rates are up sharply – the 10 year TIPS yield has gone from -1% to -0.6% since September – they are still deeply negative. To rein in inflation, real interest rates will need to rise several multiples of their increase thus far. This tightening will be devastating to capital markets that have become dependent on easy money.

The past decade has rewarded valuation-agnostic and meme-chasing investors, culminating in the unhinged growth stock mania that defined 2021. We think the next era will be marked by a return to sanity, rewarding disciplined, discerning and value-conscious investors – and we think that era has just begun.

It’s not too late to join us at Bireme. Please reach out.

Portfolio commentary

On the short side, we had an extremely profitable year despite at times enduring mark-to-market losses caused by the gyrations of the meme stock bubble in Q1. Nevertheless, shorts like FuboTV (FUBO), Virgin Galactic (SPCE), Teladoc (TDOC), Zoom (ZM), and Beyond Meats (BYND) fell more than 40%, trailing the market massively.

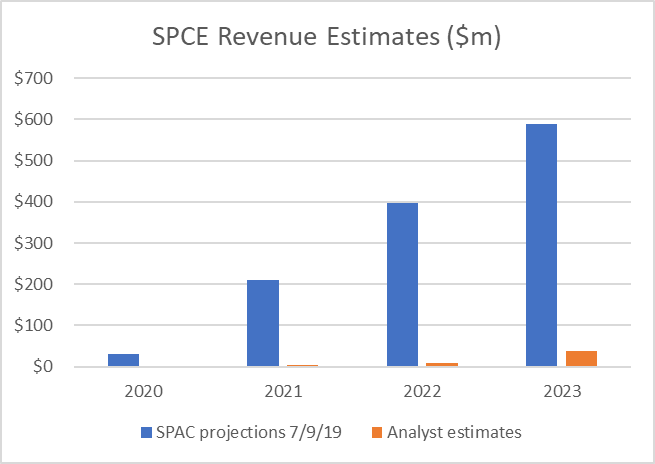

While some of these businesses simply suffered from valuation compression, others dramatically underperformed investor expectations. The worst offender was Virgin Galactic, the stock whose success

ignited the SPAC boom. During the merger process which would take it public, sponsors

projected $398m in 2022 sales. Due to the market-wide enthusiasm for such fairy tales, SPCE would eventually rocket from $10 to over $60 per share in early 2021.

Today, analysts estimate just $8m in 2022 sales.

Insiders have cynically capitalized on these absurd projections: to date they have

unloaded more than $1.7b worth of shares on the public. Despite enriching themselves, they have beggared the public; at $8 per share, SPCE trades well below both its $10 IPO price and $19.50

secondary offering price. However, the market cap of SPCE remains over $2.5b, and thus we remain short.

We did have a few short positions move against us in 2021, most notably Tesla. Tesla beat expectations for the year, delivering more than $50b of sales and a profit of $5b. These results sent the stock up about 50% for the year. While we think Tesla will continue to have success in the EV market, its valuation of over $1 trillion is roughly 12x the peak profit pool of the entire pre-pandemic auto industry.

Tesla will also fight a huge increase in competition over the next few years, with every major car maker now focused on delivering electric vehicles. We remain skeptical of the purportedly imminent robo-taxi business, which CEO Elon Musk has consistently over-promised and under-delivered on.

We think Tesla will materially underperform the market from here. But we are even more skeptical of the second- and third-tier EV companies, those with little-to-no revenue and multi-billion dollar valuations. The stocks of these companies have been buoyed by the strong price action of Tesla as investors try to catch “the next one.” We think few, if any, of these companies will generate the profits implied by their valuations.

One that we’ve

talked about in the past is Nikola, the (allegedly) hydrogen fuel cell company with zero revenue, a former CEO

arrested for fraud, and a >$4b market valuation. It has fallen materially from its peak, but NKLA still sits close to its SPAC deal price of $10 per share. We think it has farther to fall.

We are also short Lucid, which trades at a valuation over $40b USD – more than half the value of Ford and GM – despite its lack of material revenue.

The most egregious valuations in the EV space probably belong to the retail charging companies, like EVgo and Blink Charging. While we have no doubt that the retail EV charging industry will grow over time, we fail to see any competitive advantage for these firms. Competition in this sector will likely prove to be even more cutthroat than the legacy gas station industry it seeks to replace, because:

- Consumers can charge their EVs at home and at work.

- Large amounts of capital have already been raised to build these charging stations.

- Additional competition will come from manufacturers like Tesla and Ford.

Would you pay 50-100x sales for a gas station operator with large capital requirements and massively negative margins? That’s essentially what investors are doing when they buy stock in BLNK and EVGO today. We are happy to be short these companies at $1b+ valuations.

We opened a more idiosyncratic short position in a company called Affirm (AFRM) in Q4.

Affirm is a “Buy Now, Pay Later” (BNPL) company founded by former PayPal CTO and cofounder Max Levchin. They provide installment loans to consumers, partnering with retail companies looking to drive higher sales. They have two primary products: a zero-fee installment loan for consumers with the best credit scores, and a more traditional product with 20%+ interest rates for subprime borrowers. Their stated plan is to disrupt the credit industry with more transparent, lower-fee loans.

At a roughly $28b market cap at the start of 2022, AFRM stock was priced at more than 20x trailing sales, a steep price for a money-losing lender. While their early lead in online BNPL transactions and partnerships with fast-growing retailers like Peloton has fueled significant historical growth, a wave of competition has arrived.

Some examples include:

We think returns on capital are likely to disappoint in this business over the long term. Eventually, BNPL companies may be forced to compete in bake-offs to secure a spot as the preferred provider of retailers like Walmart, as they do in the

store-card business. This is not an industry that is likely to receive a high market multiple at maturity, and we think AFRM eventually trades down to the 8-10x PE ratios of Capital One, Synchrony, and Discover.

While the stock has already fallen sharply from where we initiated our short position, we think it could fall another ~40% to trade at 8x FY2022 sales.

We initiated one material long position during Q4, in a Chinese company called Tencent Music (TME).

One of the largest positions of the since-imploded Archegos fund, TME has fallen from $20 in Jan 2021 to less than $7 today, implying an enterprise value (net of cash) of less than $8b. We think this is extremely cheap for the dominant online music platform in China that currently generates $5b in revenue and $570m of trailing net profits.

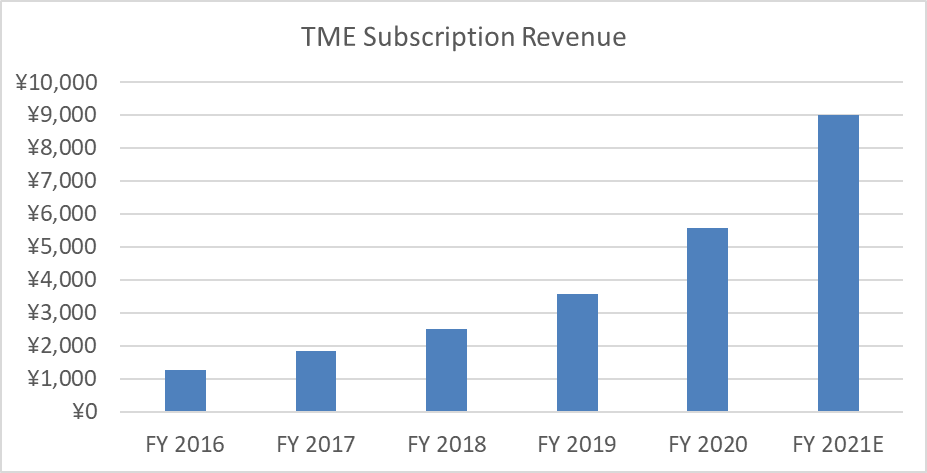

With over 800m users across its many apps, Tencent Music is the primary way that people in China interact with online music. Today, the majority of revenue comes from virtual gifts sent to streamers in its “Social Entertainment” segment, which has grown revenue from $300m in 2016 to $2.9b in 2020. Within this segment, the most popular app is WeSing, a karaoke app with hundreds of millions of users in China. While competition from platforms such as Douyin (the Chinese version of TikTok) is increasing, WeSing continues to generate substantial profits for TME.

The smaller segment (by revenue) is a subscription-based business similar to Spotify, utilizing a “freemium” model and providing Chinese users access to millions of songs. Their apps Kugou, Kuwo, and QQ Music have more than 600m users, but as of Q2 2019 more than 95% of them were on the free tier. Since then an aggressive effort has been made to grow subscription revenue, and 30% of songs are now behind a paywall. This shift has driven rapid growth in paid users, and today almost 11% of users pay for access to these songs. The size and consistency of this segment’s growth is extremely impressive. How many other companies can add 5m paid users per quarter?

We think this business could quadruple in size, eventually reaching Spotify’s level of 45% paid, and generate $5b in annualized revenue. We expect this segment to be quite profitable at maturity due to TME’s tremendous negotiating power with the major music labels in China.

Yet despite the many advantages of TME’s position in the Chinese music industry, investors have punished the stock along with those of many other Chinese companies. These stocks are languishing at multi-year lows in reaction to a string of regulatory actions undertaken by the Chinese Communist Party against the Chinese consumer internet giants. The US media has fanned the flames of this decline, couching the regulatory actions as a

“sweeping crackdown” designed to crush competing centers of power and

cement the CCP’s control.

This narrative is enticing: it provides a clean good-versus-evil story and permits reductive conclusions like

“China is uninvestable.” But that doesn’t make it true. This simplistic thinking is an example of “narrative bias,” and is precisely the type of mistake we seek to

exploit in the Fundamental Value strategy.

While we don’t dispute that the CCP’s primary goal is to maintain its own power, we take a less cynical view of these regulatory actions. Rather than trying to destroy these homegrown champions, we think the CCP is attempting to bring some common-sense antitrust regulation to the unrestrained land grab that is the Chinese tech sector. This is not dissimilar to recent antitrust actions brought by regulators in the West.

For example, take the

record $2.8b fine recently levied on Alibaba. This penalty was assessed because of

years of blatantly anti-competitive policies by Alibaba, such as requiring vendors to sign exclusive contracts. Here the CCP is merely following the example of Western regulatory authorities; the charges are eerily similar to those

filed against Amazon for punishing vendors who sell their products cheaper on other websites.

At the end of the day, we don’t see the change in regulatory regime having a large impact on TME’s business. We are confident in the growth of the subscription music segment, and foresee a company with $8-10b in revenues and hundreds of million of paid subscribers in just a few years. We will be surprised if the company’s enterprise value is less than $20b (from <$8b today), and it could be much higher. For more on this opportunity, see our full

pitch.

Finally, our investee Bollore has received a bid for its African operations. At 5.7b EUR, the valuation offered is substantial. We think the implied total value for all of Bollore is now around 17b EUR, or 12 EUR per share versus a current market price of less than 5 EUR. To see our full analysis of the bid and the implications for Bollore, please check out our full

post.

We are grateful for your business and your trust, and a special thank you to those who have referred friends and family. There is no greater compliment.

- Bireme Capital

Follow our content by subscribing here.

1 Net calculations assume a 1.75% management fee. Fee structures and returns vary between clients. FV inception was 6/6/2016.

2 Bloomberg’s World Interest Rate Probabilities function using Fed funds futures curve from 9/22/21 and 1/28/22.