After struggling during much of 2020, Fundamental Value enjoyed a phenomenal fourth quarter, soaring 47.1% net of fees compared to a gain of 18.3% for the S&P 500. FV finished the year with a gain of 29.8%, outpacing the S&P by 11.5%. Since inception, FV has returned 21.4% annualized vs 15.6% for the S&P 500.1

Part II: Anatomy of a Bubble

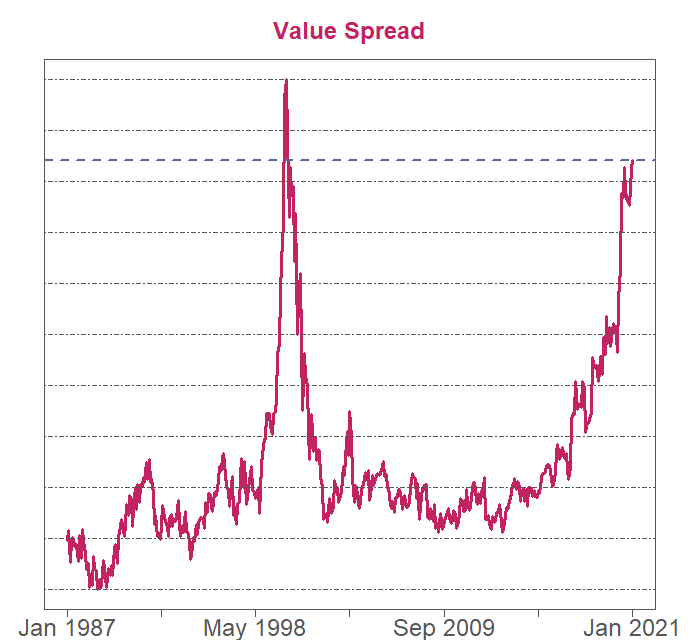

In our Q3 letter, Part I: Birth of a Bubble, we told a story of rampant speculation, untenable valuations for growth stocks, and historically attractive opportunities in value stocks. We presented our version of the “value spread,” the difference in valuation between the cheapest and most expensive stocks in the market. We said that the abnormally high value spread meant that future relative returns to value were likely to be exceptional. We issued a call to action:

We believe that the prospects have never been better for value investors than they are today… We are convinced that today is the day to go all-in on value.

In some ways, this call was prescient and perfectly timed. The Russell 1000 Pure Value Index was up 31.3% in the fourth quarter, including 22.9% in the month of November, by far its best month in history. The Dow Jones Market Neutral Value Index, a measure of the relative return of market- and sector-neutral value, was up 10.2%. FV was up nearly 50% in the quarter. FV was up 18% on November 11th alone after Pfizer’s Phase 3 vaccine results were released, as investors came to the belated conclusion that the pandemic would end one day after all.

You might think that this would be cause for a victory lap, that we would be congratulating ourselves on calling a top in the value spread. However, this saga is far from over. Despite value’s record-breaking quarter, the value spread is even higher than it was when we wrote Part I.

How is this possible?

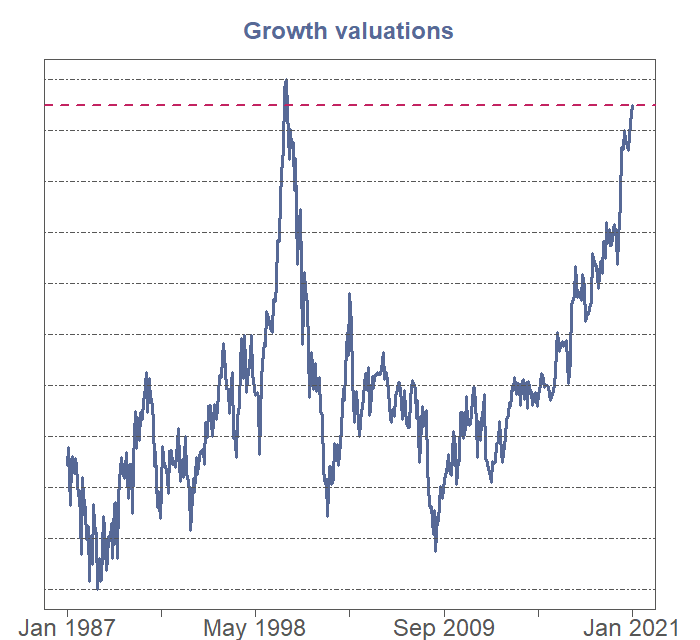

Value stocks did very well; the valuation of the median value stock increased from the 10th historical percentile at the end of Q3 to the 25th percentile at the end of Q4. But the valuation of the median growth stock exploded even higher. Growth valuations are now within shouting distance of the tech bubble peak.

Thus, despite value’s run in the fourth quarter, value still massively underperformed in 2020. The canonical Fama-French value factor, which measures the relative return of cheap versus expensive stocks,

declined 30.8%, making 2020 the worst year on record in nearly a full century of data. The Russell 1000 Pure Value Index underperformed the Pure Growth Index by a shocking 65.6%.

We feel like a broken record at this point, having discussed little but the value spread for

many quarters now. We recognize the incoherence of breaking down the equity universe into mutually exclusive and simplistic “growth” and “value” categories. It is not how we invest; in the end, every potential investment needs to be evaluated on its own merits.

However, the seemingly arbitrary distinction between growth and value has unprecedented importance in the marketplace today. The average daily move up or down for the Dow Jones Market Neutral Value Index was 1.18% in 2020. This is nearly three times the average daily move prior to 2020, and nearly twice the prior annual high of .62% from 2008. Unsurprisingly, our US value strategy saw unprecedented volatility. FV’s best twenty days all took place in 2020 -- as did its worst twenty.

Below, we break down the value and growth dynamics into more refined categories and discuss some representatives.

The anatomy of a bubble.

In Part I, we described the positive feedback loop that takes a plausible narrative and transforms it from a compelling investment thesis to a bubble:

Rising expectations beget new investors, new investors beget higher valuations, and higher valuations beget rising expectations.

This valuation flywheel has been spinning in overdrive over the past year, a phenomenon maybe best exemplified by the Goldman Sachs Non-Profitable Technology Index. Established in 2014, this index was flat and uneventful until 2020, when it went parabolic,

quadrupling in less than a year.

We shared an exhaustive list of signs of speculative excess

last quarter. Since then, the list has become more numerous and more extreme. We share only a few more below.

As we noted above, the value spread is at its most extreme excluding a brief period at the height of the tech bubble in 2000. A number of other indicators share that dubious distinction. The average first-day IPO pop was the

highest since the tech bubble. The S&P 500 and Nasdaq 100 are both trading at

higher valuations than any time other than the tech bubble. Short interest in the median S&P 500 stock is

nearly at tech bubble lows, indicating a nearly universal lack of healthy skepticism and disagreement among investors.

And many more indicators are at their highest levels ever. US companies

sold $368b in new stock last year, 54% more than the prior annual high. Stock funds saw the largest week of equity inflows

ever. Yet corporate insiders aren’t buying it; in fact, they are selling at a

record pace. The volume of bullish call options traded is

exploding off the charts. Citigroup’s Panic/Euphoria Index set new

euphoric highs.

Investors have lost any shred of fear. Daily returns of 50% and 100% in companies worth tens of billions of dollars have become the

norm. In search of a fortune, investors reach higher and higher up the speculative pyramid, each level more rickety than the last. We start at the base.

2

The transcenders.

The five megacap tech companies are truly transcendent businesses. They dominate huge markets and earn enormous -- and growing -- profits.

For much of 2020, Apple, Amazon, Microsoft, Facebook and Alphabet (Google) made up

roughly 22% of the S&P 500, an unprecedented total for five companies. This is not due to outsize valuations: four of the five trade at lower earnings multiples than the Nasdaq 100, with Amazon the lone exception.

At times, some have traded at even lower valuations, valuations more appropriate for troubled companies than transcendent ones. When they did, we were thrilled to have big positions in them (see our

Apple thesis from 2017 and our

Facebook thesis from 2019).

These stocks are not without their risks -- their success has led to big targets on their backs. Regulators in the

US and

elsewhere seek to rein in their power.

Upstart competitors and

tax authorities seek a piece of the pie. Intra-big-tech

squabbling is on the rise.

Nevertheless, these companies seem neither especially cheap nor outrageously expensive to us today. Instead, their size, quality, and relatively reasonable valuations have obfuscated the true extent of the bubble in more speculative securities: when you believe that every company that calls itself a “tech disruptor” will one day rake in hundreds of billions of dollars in revenue at >50% gross margins like Google, it is easy to justify nearly any multiple on today’s figures. But we think investors have wildly unrealistic expectations for the success of the average growth stock. We believe truly transcendent companies are few and far between.

The contenders.

Investors who climb to the next level of the speculative pyramid will find the contenders, companies like Shopify, Zoom and Teladoc. These firms build promising technology and deliver compelling products, but have market caps in the hundreds of billions despite negligible profits. The pandemic has propelled these stocks to absurd heights, as investors believe that lockdown-driven shifts in consumer behavior will persist over the very long term. While we believe this thesis has merit in some cases, we do not think that the pandemic has materially changed the long-term prospects of most of these firms. Instead, it has merely shifted forward demand. Over the past two years, the share prices of these companies have soared: TDOC is up >4x, ZM is up >6x, and SHOP is up >7x. It is difficult to comprehend how the long-term value of these companies could have increased by as much as their stock prices just because demand has been pulled forward.

Of all the contenders, Tesla may have the most unrealistic expectations. Now Tesla inarguably deserves a ton of credit for driving forward the frontiers of electric vehicles, car design, and consumer adoption of autonomous driving. However, as we said in Part I, “There’s a difference between a great company and a great investment.”

Tesla’s worldwide market share is only about 1%, but its market cap is

higher than the nine largest car companies

combined. Growing into this market cap is going to be impossible. Bending metal just isn’t that good of a business: car manufacturers generally earn single-digit net margins. Hopes of recurring high-margin revenue from software sales and robotaxis are pipe dreams -- in a third-party ranking, Tesla’s much-ballyhooed autonomous driving system recently came in

dead last out of 18 competitors.

Tesla did eke out a profit for the first time this year, but only because of $1.5b in pure-margin revenue from sales of automotive regulatory credits to other car manufacturers that did not meet emissions standards. This pure-margin revenue will disappear shortly as competing EVs enter the market. Nearly a hundred EV models are set to

debut in the next few years, from large and established industry players like Ford, Toyota and GM, as well as upstarts like NIO, Fisker, Lucid, Rivian, and many, many others.

Tesla does have a market share lead in the EV market, but we find it hard to believe that the technology lead is insurmountable -- Tesla’s latest annual report

revealed that it spent more on bitcoin than on research and development. (We would be remiss not to mention the incongruity of a company focused on sustainability buying bitcoin, the energy-intensive mining of which produces

more greenhouse gases than many medium-sized countries.)

We suspect that for many stockholders a share of Tesla is more of a collectible than an investment. Jim Cramer recently tried to

explain Tesla’s astonishing stock gains (up 13x in the past two years). He said, “The analysts couldn’t understand that Tesla is more than just a vehicle. It’s a vehicle of hope in a miasma of gloom.” That may be true, but if you are looking for a solid investment rather than a manifestation of optimism, we suggest you look elsewhere.

We are short Zoom, Teladoc and Tesla.

The pretenders.

Those who dare venture further up the speculative pyramid find the pretenders. At this level, companies are devoid of solid business models, meaningful proprietary technology, or even working products. However, these companies are skilled at mimicking the signals of other more successful companies. They absorb the zeitgeist and learn the relevant buzzwords -- electric vehicles, blockchain, disruption -- and spend more energy marketing their stock than building a business.

Recently, we received two voicemails from an employee in the investor relations department of Electrameccanica Vehicles Corp. He told us that they were an electric vehicle company, that the ticker was SOLO, and that he had sent us some materials and would be happy to talk about it.

In case the absurdity of this does not strike you immediately, let me be blunt: no one calls us. Not just no publicly listed companies! Virtually no one at all. This isn’t a thing that happens. We’re a small

boat in a very, very big sea. To receive a solicitous cold call from a publicly listed company with a market cap of $750m is scarcely credible -- but we have the voicemails to prove it. If anything in the history of the world has ever screamed “stock promotion,” it is this. SOLO has assembled a cold calling team not to sell its $18,500 single-seat EV, but to sell its stock.

Similar companies are everywhere in today’s overly credulous marketplace. And their share prices are soaring. SOLO is trading over $7 today; it traded under $1 for several months last summer. Such companies exist in every phase of the economic cycle, but today, their ubiquity and their share price performance are indicative of late-cycle behavior.

The EV space in particular is rife with pretenders.

Nikola Corporation (NKLA) is a poor-man's facsimile of Tesla. Even the name is a blatant ripoff: both are named after the inventor Nikola Tesla. NKLA is a pre-revenue company founded in 2014 that has yet to bring a product to market, despite the promotion of a

dizzying array of concepts:

- Nikola Badger: pickup with both fuel-cell and electric variants

- Nikola One: fuel-cell commercial semi-truck

- Nikola Two: fuel-cell commercial semi-truck

- Nikola Tre: electric commercial semi-truck

- Nikola NZT: electric four-wheel drive utility vehicle

- Nikola Reckless: electric military grade off-highway vehicle

- Nikola WAV: electric watersports vehicle

As far as we can tell from their

latest investor communications, only the Nikola Tre Commercial semi-truck is still in development.

NKLA’s history is full of deception and vaporware. They showed a video of the Nikola One in motion; they later

admitted that it didn’t work and was just rolling down a hill. NKA’s founder Trevor Milton resigned in disgrace after Hindenburg Research published a

report calling NKLA an “intricate fraud.” NKLA is currently under investigation by

both the SEC and DoJ. Partnerships with

GM,

Republic Services and

BP have been canceled. Nevertheless, the company sports an $8b market cap, because “electric vehicles.”

Though pretenders are particularly ubiquitous in the

bubbly EV industry, pretenders are to be found in many other industries as well.

Vaxart (VXRT) was a biotech penny stock until COVID-19 hit, when it released a series of announcements about the progress of its oral tablet coronavirus vaccine. In late June, VXRT

claimed to have been selected for the federal government’s Operation Warp Speed vaccine development program despite having only 15 employees. The stock traded more than 60x higher than where it started the year.

This announcement was profitably timed for insiders. In early June, just weeks before the Operation Warp Speed announcement, the CEO was awarded stock options worth $4m, and a hedge fund renegotiated accelerated warrants. By the end of the month, the CEO’s options were worth $28m and the hedge fund had exercised the warrants and sold the shares for a profit of nearly $200m.

Oh, and the claim that VXRT was selected for Operation Warp Speed turned out to be

false and misleading. The company is currently under investigation for fraud.

VXRT is still exhibiting classic pretender signals. In a vaccine progress roundup from January, Science

commented that they could find “no updates at all about its clinical progress -- just excited talk about its prospects as an investment.” Numerous press releases talked up its partnerships, like a manufacturing

agreement with KindredBio -- a tiny company with less than $5m in revenue, self-described as “focused on saving and improving the lives of pets.”

Since then, VXRT has released their Phase I trial

results. The press release is titled “Positive Preliminary Data,” but near the bottom it revealed that no neutralizing antibodies were found. The stock price tumbled.

There are now a handful of vaccines approved, with several more likely to be approved shortly. And there are dozens more in development, all from larger and more sophisticated companies than VXRT. Each incremental vaccine will find it harder and harder to make it through the grueling approval process as competitors cross the finish line first and coronavirus prevalence declines. Even vaccine developers with highly promising candidates may not be able to recruit tens of thousands of Phase 3 trial participants given the increasing supply of approved and highly effective COVID-19 vaccines.

We find it nearly inconceivable that VXRT will develop a commercially successful coronavirus vaccine, which it desperately needs to justify it’s valuation. VXRT’s Q3 revenues were under $300,000. Nevertheless, it sports a market cap of over $800m, because “vaccines.”

Kodak (KODK) is a dying photography and printing company. The company has had declining revenue and negative free cash flow every year since 2007. In August, KODK announced that the Trump administration would give it a $765m loan to manufacture key pharmaceutical ingredients, a capital-intensive and low-margin business dominated by Chinese firms. KODK’s shares went parabolic,

soaring as much as 20x in two days -- a preposterous ~$2.5b increase in market cap based on a purported entry into this challenging industry.

Not that KODK is likely to get that loan anyway. The loan is on

indefinite hold. The inspector general of the government agency that approved the loans is investigating the terms. The SEC is also investigating allegations of insider trading: the day before the loan was announced, the KODK CEO was

given 1.75 million stock options, some of which were immediately exercisable. Within days these options would be worth $50m.

KODK is a perennial pretender. Comically, KODK’s shares briefly tripled in January of 2018 when it attempted to

capitalize on the first cryptocurrency bubble by announcing “KodakCoin,” a cryptocurrency to “empower photographers and agencies to take greater control in image rights management.” Needless to say, that never came to fruition.

Though well down from their most absurd highs, KODK shares persist at >4x unaffected August levels, because “pharmaceuticals.”

MicroStrategy (MSTR) is the latest firm with shrinking revenues and negligible profits to pivot to the blockchain. Rather than attempt to start a cryptocurrency business, MSTR pivoted in the most straightforward way possible: it simply bought hundreds of millions of dollars worth of bitcoin overnight. In one light, this is an utter abdication of all the principles of corporate finance. Why not return the money to shareholders, who can decide for themselves whether or not they want to own bitcoin? But in another light, this was a brilliant end run around the SEC, who has been denying bitcoin ETF proposals left and right for years. MSTR went from being a mere stagnant software business to the de facto bitcoin ETF.

MSTR has made a ~$3b windfall on its bitcoin purchases. However, its market cap has increased by roughly $9b. While nonsensical, this massive premium is unsurprising, given the froth in the cryptocurrency market and the paucity of publicly listed vehicles for bitcoin speculation. According to our calculations, MSTR’s current share price implies a bitcoin price of $122,000, more than double current levels.

We calculate the fair value of MSTR shares to be $450 at current bitcoin prices. It trades at nearly $1000, because “bitcoin.”

We are short NKLA, VXRT, KODK and MSTR.

The pump-and-dumpers.

At the apex of the speculative pyramid are the pump-and-dumpers. In your typical pump-and-dump scam, one informed party attempts to get rich quick by cynically duping others into buying stock off them at inflated prices.

Today’s pump-and-dumps are far more collegial. Very few people are duped. Instead, traders on Robinhood, Reddit and Twitter coalesce around a stock. The company has virtually no role in the scheme; it is merely an abstract vehicle for gambling. Maybe there was once an underlying investment thesis related to the company and its cash flows, but at some point, everyone forgot what it was. Some of these stocks

aren’t even really businesses at all -- they don’t have working phone numbers or file annual reports.

Instead, the stock serves as a

Schelling point for an informed and cooperative Ponzi scheme -- a Ponzi game, or a Ponzi party, if you will. These Ponzi parties can be triggered by anything. A frequent trigger is an Elon Musk

tweet. Those who get in early are hoping to get rich quick off those who get in later. And those who get in later are hoping to get rich quick off others who get in even later, and so on. Nobody is buying these stocks for their future cash flows.

Accompanying Ponzi parties at the apex of the speculative pyramid is the SPAC. SPAC stands for Special Purpose Acquisition Company -- or as we like to call them, Sponsors Pilfering Average Consumers. These blank-check companies are the logical conclusion of a bubble: they are the pure abstraction of the IPO pop. A SPAC is a

meta-IPO, an IPO without the annoying distraction of an actual operating company. These shell companies are shell games, a virtually no-lose situation for SPAC sponsors, investment banks, and hedge funds, subsidized by retail investors who believe they finally have an opportunity to participate in the heralded and elusive first-day IPO pop.

This would all be amusing were it not so dangerous to the health and wealth of retail investors, our capital markets, and our capitalist system as a whole.

We have much more to say on these issues. But as this letter is already quite unwieldy -- and because this developing story gets continually

more absurd every day -- we will reluctantly push more discussion off until Part III.

The other end of the barbell.

Despite the inanity at the top of the speculative pyramid, opportunities remain to own unsexy but proven businesses on the cheap. This is the other side of the value spread, the other end of the “barbell market” we mentioned in Part I. There are lots of very expensive stocks, but lots of very cheap stocks as well.

We believe both ends of the barbell are symptoms of a single cause: extrapolation bias. Extrapolation bias is the tendency for investors to uncritically assume that recent trends will persist into the indefinite future. It is one of the many cognitive biases we seek to exploit in

Fundamental Value. Both the overvaluation of many growth stocks and the undervaluation of many value stocks have been driven by COVID-19 extrapolation, by investors uncritically assuming that the pandemic-borne benefits or burdens to businesses would continue indefinitely.

We have been willing to take the other side of that bet. Since March we have increasingly tilted the long book towards stocks whose businesses will improve as the pandemic fades, a strategy we first discussed in our

1Q20 letter. Now that 2020 is -- thankfully -- over, let’s take a look back at some of our predictions from Q1.

HCA Healthcare (HCA) runs for-profit hospitals. In Q1, we said:

We were shocked to see HCA initially trade down more than 50% in mid-March, in line with hotel companies and online travel agents. HCA will likely earn $11-12 in EPS when the COVID-19 crisis recedes, and we think the stock will trade back towards $150. Therefore, during Q1 we added we added ~80% to our shareholdings at an average price of roughly $90.

If anything, this prediction was pessimistic. Despite the raging pandemic, 2020 revenue of $51.5b was actually up year-over-year. Earnings increased as well, with 2020 EPS of $10.93 and guidance of $12.10-13.10 in EPS for 2021. Said another way, in March HCA was trading for about 5 times 2021 earnings. We think that at $175 this stock is still cheap today and should trade at well over $200 per share.

Kite Realty Group (KRG) is a Real Estate Investment Trust that owns grocery-anchored strip malls. In Q1, we said:

Unfortunately, COVID-19 has severely impacted service businesses, including restaurants, most of whom have been forced to close or reduce capacity. As a result, KRG stock fell as much as 63%, from $19 to $7… At $7 per share, KRG traded for an 18% dividend yield and an implied 12.3% capitalization rate, rare numbers in the real estate world outside of failing properties. We do not think KRG is failing. We do not think this is the last time that people will work out in gyms, sit down at restaurants, get their nails done, or pick up their dry cleaning. It is our view that most of these businesses will survive and eventually pay rent again, although there will likely be a 6-12 month period of shared pain between tenants, employees, landlords, banks, and taxpayers… As consumers slowly return to service businesses, we think KRG will return to trading at much higher prices.

If anything, this prediction was pessimistic. While many of KRG’s tenants were closed in April, almost all of them were operating as of

late October. The company continues to sign new leases with >10% price increases; tenants realize the importance of good locations irrespective of COVID-19. We think KRG will soon return to paying a $1.10-1.30 annual dividend as they did prior to the pandemic. This is an attractive 6-7% yield on the $18 share price.

RCI Hospitality (RICK) is a publicly-traded owner of night clubs and restaurants. In Q1, we said:

The company has been dramatically impacted by COVID-19, with all of its locations unsurprisingly deemed “non-essential.” The stock has fallen from a pre-COVID level of about $25 per share to an intraday low of $7 per share, the largest decline in any stock we own. Prior to this drop, we had a tiny toehold position of <.5% of NAV with a cost basis of around $15. We began buying in earnest when the price dropped below $10 per share… We believe RICK will make it through the crisis and that investors buying it at less than 3x potential FCF will be handsomely rewarded.

If anything, this prediction was pessimistic. RICK has blown past the estimates we made early in the pandemic, when its very existence was in question. In fact, while only 10 of the company’s 45 locations were open in Q2, the company still managed to generate positive operating cash flow due to the stellar results at their “Bombshells” brand restaurants. These locations continued to perform well into the second half of 2020, with Bombshells same-store-sales up 50% for the third quarter and 18% for the trailing twelve months. RICK was trading at $10 at the end of March; it trades at $60 today.

Ryman Hospitality Properties.

In Q3, we purchased shares of Ryman Hospitality Properties (RHP), another company whose business and stock price were temporarily crushed by the pandemic. Ryman is an owner of large, convention-focused hotels under the “Gaylord” banner. Prior to 2020, the company had grown EBITDA every year since 2012, and has a demonstrated ability to profitably develop new hotels from scratch, having opened 5 since the year 2000. These hotels

dominate their niche in the conference and convention segment: they have more meeting space square footage than almost all of their competitors.

Ryman also operates a fast-growing music venue business, which includes the Ryman Auditorium, the Grand Ole Opry, and a chain of bar and concert venues called “Ole Red.” These comprise RHP’s “entertainment” segment, which grew EBITDA from $14.5m in 2011 to $58m in 2019, an 18% CAGR.

We think the company will do more than $300m of free cash flow in 2022. When we were buying RHP at the end of Q3, it had a market cap of $2.0b, a mere 6x multiple of FCF. While the market cap has recently increased to $3.7b, we still find the valuation very attractive for a company with their track record.

Regional banks.

In Q4, we made a significant long bet on a basket of regional banks.

Small banks are about the furthest possible thing from the hyped-up growth companies that dominate the headlines today. You will not catch any of these in the ARK Innovation ETF, but that does not make them bad companies, or bad investments. In fact, after many years of underperformance, it is time for these businesses to shine. They trade for significant discounts to market multiples, with the KRX Regional Bank Index trading at just 14x 2021 earnings and the S&P 500 trading at 23x.

Investors appear to have two major concerns when it comes to smaller banks: COVID-related loan losses and declining net interest margins. We think the former will prove immaterial and the latter is overly discounted in today’s prices.

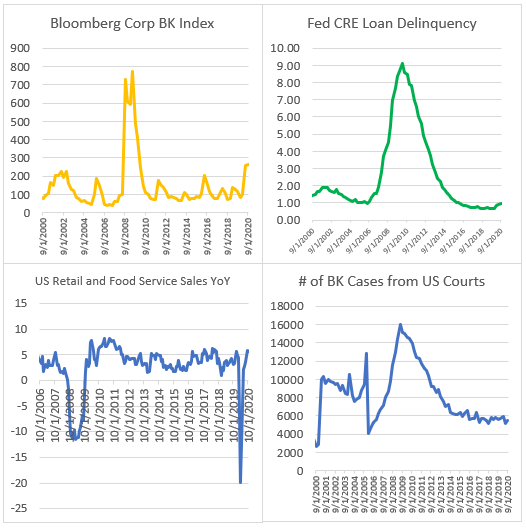

On the balance sheet side, we see multiple indicators that banks will enter the second half of 2021 in a relatively healthy lending environment. Personal bankruptcies and loan delinquencies are at near-term lows; perversely, the savings rate has

soared due to the pandemic, as trillions in government aid has more than offset income declines and spending opportunities continue to be few and far between. Corporate bankruptcies, while seeing an uptick, are still far below the level of 2009 according to the Bloomberg Corporate Bankruptcy Index. And retail sales, which dropped precipitously in April, have notched seven consecutive months of year-over-year growth.

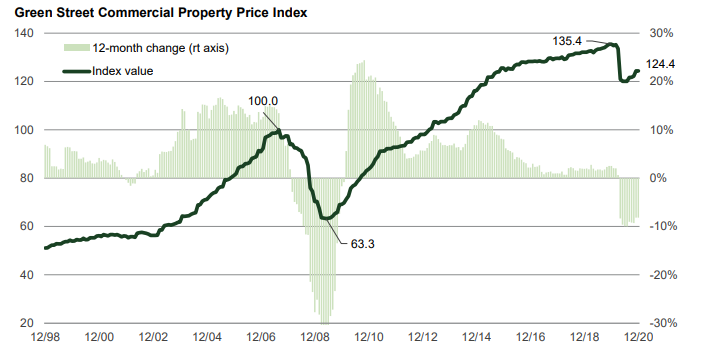

Even if borrowers do default, we expect the vast majority of loans to be well-covered by the commercial real estate (CRE) assets that typically secure them. CRE prices have held up well thus far in the pandemic, with overall prices falling just 8% and the hardest hit sectors falling 15-25% per

Green Street. This is a much smaller drop than the 40% plunge we saw during the financial crisis. Our banks typically have LTVs averaging <50%. Thus, an 8% drop in real estate prices indicates that these loans retain a substantial margin of safety.

The risk of falling interest rates is another common concern that we feel is unlikely to dramatically impact regional bank earnings in the near term. For one, these banks -- unlike large money center banks -- still pay substantial average deposit yields of 0.50% to 1.00%. This gives them a natural hedge if rates fall.

Second, loans to small businesses comprise nearly all of regional bank balance sheets. These loans tend to be relationship-based, and require knowledge of the local business landscape. Because these loans are less commoditized, their yields tend to be slightly less sensitive to falling market interest rates than the home mortgages and debt securities which typically make up a large segment of the balance sheets of bigger banks.

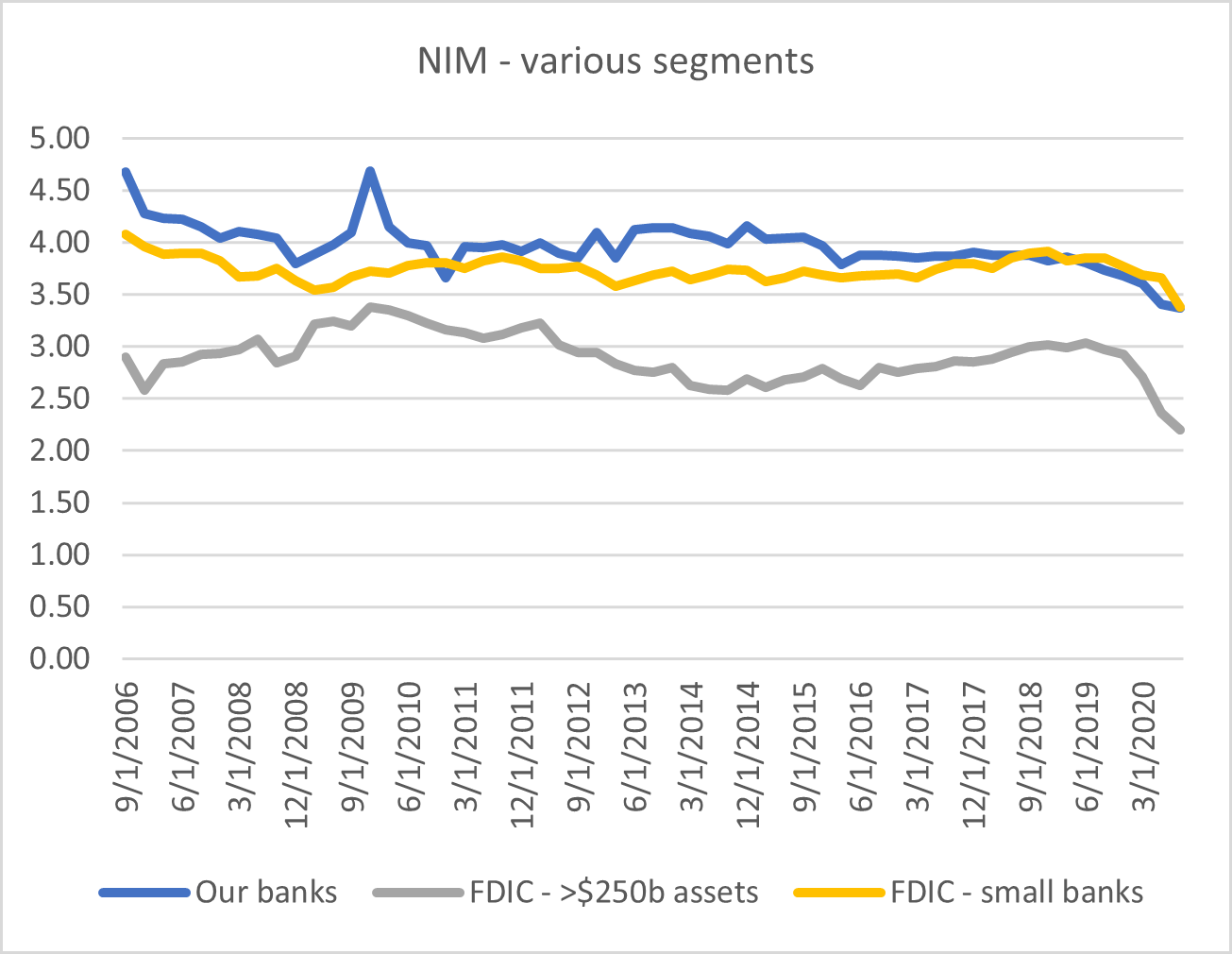

These factors have allowed for more stable net interest margins at smaller banks relative to their larger peers, as

data from the Federal Reserve shows.

After speaking with the management teams from numerous small banks, the consensus is that net interest margins (NIM) should be relatively flat from current levels. Some of these banks actually expect NIM to increase in the coming quarters due to the roll-off of higher yielding certificates of deposit.

Overall, we feel that owners are well compensated for these risks given the 8-12x PE ratios. We invested in a group of six regional banks with position sizes ranging from 1% to 2.5%.

Conclusion.

Despite value’s recent revival, the value spread remains near all-time highs. The barbell market presents enormous opportunities for discerning active managers on both the long side and the short side. We have never been so enamored with the available opportunity set.

Please reach out to us if you would like to get involved at such an opportune time.

Look out for Part III: Apex of a Bubble.

- Bireme Capital

Follow our content by subscribing here.

1 Net calculations assume a 1.75% management fee. Fee structures and returns vary between clients. FV inception was 6/6/2016.

2 The share price and market capitalization data throughout is as of February 19th unless otherwise noted.

{kind=link}

{kind=link}