The second quarter of 2019 saw positive returns across nearly the entire Fundamental Value portfolio, with the strategy up 5.3% after fees relative to the S&P 500 at 4.2%.

Since inception, FV has gained 18.8% annually net of fees, beating the market by 5.2% per year. A hypothetical investment of $100,000 in FV at inception would have turned into $169,000 at the end of Q2, compared to $148,000 if invested in the SPY ETF.1

Market commentary

Active value investing is the core of our philosophy at Bireme Capital. We believe that even naive value investing offers superior long-term return prospects relative to passive investing. That is, we think evidence and theory suggests that merely overweighting the cheapest stocks according to valuation summary statistics (e.g., price to book) should be enough to outperform over the long term. Since 1926, value has outperformed growth by 3.7% annually according to the canonical Fama-French HML portfolio.2

Further, we believe there is significant room for intelligent, disciplined managers to improve on naive value investing with sophisticated security selection. At Bireme, we hope to capture the classical value premium, plus add our own alpha by finding assets that are inappropriately valued in the marketplace.

Nonetheless, our relative returns will tend to be correlated with the value factor. Since Bireme’s inception in June of 2016 through the end of the second quarter, returns to value have been distressing: measured by the HML portfolio, value has underperformed growth by -5.4% annually. In fact, HML was 36.8% below the all-time high it reached back in 2006 -- well over a decade ago. Despite its value tilt, FV has been able to outperform the broad S&P 500 by 5.2% annually net of fees, and the S&P Value Index by 8.5% annually.

From time to time, we must reevaluate our value-oriented philosophy in light of new evidence, especially during periods of prolonged underperformance like the current one. Rather than recap the extensive literature on value investing, here we examine the likely causes of value’s underperformance since 2006.

In our view, value's returns have been driven primarily by a widening of the value spread; growth stocks have simply gotten more expensive. But why has that occurred? We think a key factor has been the level and structure of interest rates.

The value spread

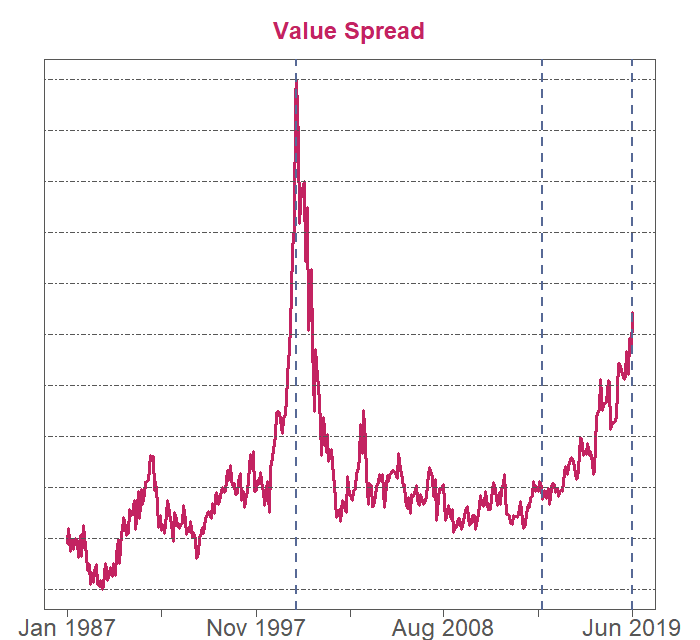

The “value spread” is the difference between the valuations of the cheapest and most expensive stocks in the market. While it is an imperfect and incomplete tool, the value spread can give us some indication of the likely returns to value. If value stocks aren’t actually trading much cheaper than the rest of the market, value is likely to disappoint. If, however, value stocks are trading at a large discount, there is more value than usual in value stocks -- a good sign for future returns.

There’s no single, correct way to measure the value spread. At Bireme, we maintain a proprietary metric that we think better represents the discount to value than many of the alternatives.3

There are three vertical lines on the chart. The first is March 2001, the height of the internet bubble, and also the all-time top in the value spread. Value (the cheapest third of the market, according to our metric) went on to outperform growth (the most expensive third) by nearly 20% annually over the next 5 years, resulting in a phenomenal 147% of total outperformance.

Compare to the last vertical line, the end of the second quarter of 2019. While not as extreme as the peak in 2001, the value spread today is quite elevated.

The middle vertical line, April 2014, marked the peak cumulative outperformance for the Bireme-defined value portfolio relative to growth. Value proceeded to underperform growth by -32% over the next 5 years. Though the value spread wasn’t very attractive in April 2014, it wasn’t at all-time lows either. Why the large drawdown? Why has the value spread been driven to such extremes since 2014? We think a major reason is a change in the structure of interest rates.

Interest rates

When calculating the value of an asset, investors use interest rates to decide how much to discount future expected earnings. Higher interest rates means earnings far in the future are highly discounted, and thus earnings today are relatively more important.

Interest rates are intricately linked to nearly everything in the economy, and the value factor is no exception. Since the financial crisis, we’ve been in a period of exceptionally low interest rates, and long-term rates have fallen some since 2014. This has favored growth stocks, whose earnings are expected to grow more than value stocks, and thus have longer duration: more of their net present value is tied up far in the future. Due to lower rates, growth’s expected future earnings are not being discounted as much as they were in the past.

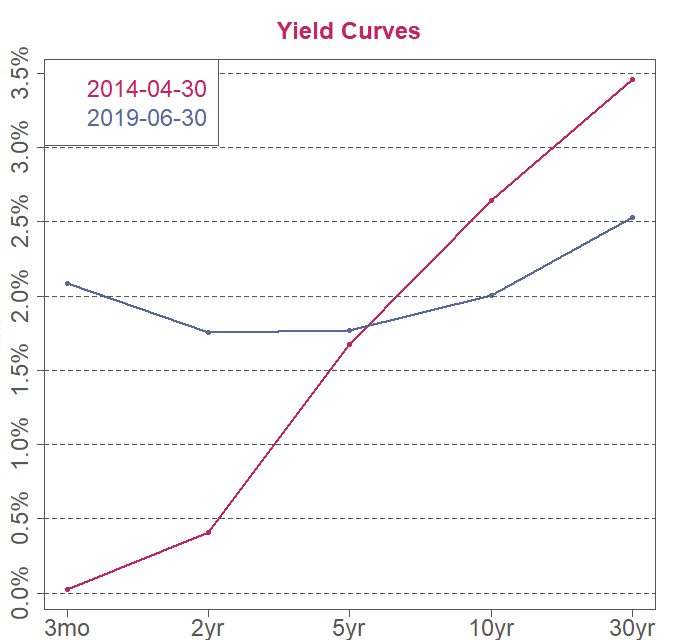

Not only are we in a period of exceptionally low interest rates, but since 2014, the term structure of interest rates has changed drastically. Usually, long-term interest rates are higher than short-term rates, representing the inducement necessary to lock up one’s money for a longer period of time. This shows up as an upward sloping yield curve.

In the five years since 2014, the yield curve has flattened substantially. The yield curve has even been inverted at times (i.e., shorter rates higher than longer rates).4

Like low interest rates, a flat yield curve favors growth over value. If the yield curve is flat, earnings far in the future are discounted at the same annual rate as near-term earnings, rather than at higher and higher annual rates each year. Because value represents the segment of the market where near-term earnings, dividends and current assets are relatively more important than long-term growth plans, value is disadvantaged.

The data confirms this theory. We use the spread between the interest rates on the 2yr and 10yr US Treasury bonds as a proxy for the entire yield curve. Since 1976, in the third of months when the yield curve flattened the most, value underperformed growth by -21bps on average, resulting in -30% total underperformance. In stark contrast, in the third of months with the most steepening, value outperformed growth by 52bps on average, resulting in 146% of total outperformance.

A final note: yield curve inversions are considered a strong recession indicator. If a recession occurs, growth expectations will be lowered, and this will further favor value.

Conclusion

Value has underperformed growth significantly over the past decade-plus. As a value manager, this has been frustrating and disappointing. However, we think better times are ahead. Value is especially cheap: the value spread is higher than at any time except the internet bubble. The flattening yield curve has significantly contributed to this spike in the value spread, but the term premium is near zero, and we think this trend is closer to its end than its beginning.

Investors cost themselves dearly when they abandon a well-reasoned investment strategy to chase hot funds and asset classes. Though value’s underperformance over the past decade has been trying, we think value investors will be rewarded, sooner rather than later, for sticking with their discipline.

Portfolio commentary

Our largest gainer in the quarter was Facebook, which rose 16.6%, approaching all-time highs. Despite this advance, we still find Facebook cheap. After backing out net cash, the company’s market value of $500b is about 20x 2019 estimated earnings. Given that the business will probably grow revenues 25% this year and has a long growth runway ahead, we find this inexpensive relative to the S&P 500’s 17.5x PE and estimated growth of 4.9%.

That said, the specter of regulation continues to loom over the company, with news coming out after quarter-end that the FTC is probing the company’s acquisition history. These headlines frighten investors, but are unlikely to impact long-term value. We expect that increased regulation will not lessen the company’s dominance of social media. In fact, costly new regulations may deepen Facebook’s competitive moat by making it more expensive for sub-scale challengers to operate.

Our investment strategy is predicated on finding situations where investor cognitive biases have created a divergence between price and value. Availability bias, one of our staples, is the proclivity of investors to focus on the salient rather than the important. In Facebook’s case, the steady drumbeat of negative headlines has obscured the strength of the underlying business. To read our Facebook thesis in more detail, please see our note from April here.

German pharmaceutical company Bayer was our second-largest contributor for the quarter, with shares returning 10.1% including dividends. But while this investment notched a gain in Q2, Bayer is actually down for the year.

Like Facebook, Bayer’s decline was due to a drumbeat of negative headlines. On March 20th, a jury in San Francisco found that Roundup was a “substantial factor” in the cancer of a plaintiff. Bayer fell nearly 10% on the news. That plaintiff was initially awarded $80m in damages, though it was reduced to $24m on appeal.

On May 13th, shares fell further when a jury awarded the comically large figure of $2 billion to a husband/wife plaintiff. In July, a judge refused to throw out that verdict, although he did reduce the damages to $87m. Business results have not been perfect either: recently Bayer warned investors that earnings might be lower than forecasted due to severe US farm belt weather pressuring its Crop Science division. On that earnings call the company also revealed that the number of lawsuits against Monsanto had ballooned to 18,400 from 13,200 in April.

In May, Judge Chhabria, the CA judge assigned to the largest group of cases, appointed Ken Feinberg to mediate negotiations between the two sides. Mr. Feinberg, the man who famously ran the 9/11 victim’s fund, has a reputation as a fair arbiter. In our view, he is likely to look at previous product settlements to determine a range of fair values, which implies about $250-400k per plaintiff at the upper end. This suggests Bayer’s exposure may be about $8b before legal expenses.

To get a better sense of how Monsanto’s case compares to those listed above, it is instructive to look at an individual case. Let’s take Merck’s Vioxx.

Merck withdrew Vioxx voluntarily in 2004 after a study confirmed that the drug roughly doubled the risk of heart attacks. Lawsuits mounted soon after, and Wall Street began to ponder Merck’s total liability. As the NYT wrote later, “In 2005, most analysts estimated that Merck’s ultimate liability in Vioxx would be between $10 billion and $25 billion.”

There were good reasons for sell-side analysts to be concerned. Long-term trials had confirmed Vioxx’s danger, and the number of patients was huge: Merck ended up facing 47,000 total plaintiffs. But at the end of the day, Merck settled for $4.8b, much lower than initial estimates. We think this figure, adjusted for inflation up to $7b, is a good upper bound for Monstanto’s risk. And there are reasons to think Monsanto may settle for less.

In contrast to Vioxx, Monsanto has not admitted Roundup is dangerous when used properly. In fact, the EPA stated in May that glyphosate (the active ingredient in Roundup) poses “no risk to public health when used in accordance with its current label and is not a carcinogen.” Monsanto is also facing about half the number of plaintiffs. In fact, Vioxx is estimated to have caused more deaths (25,000) than Monsanto faces today in total lawsuits (<20,000).

Even if a settlement rose to $10b, more than double the largest single-product settlement in history (Vioxx), it would pale in comparison to the roughly $50b decline in Bayer’s market capitalization since the first trial. We think this discrepancy is driven by investors myopically extrapolating a small number of early cases across a multi-thousand case class action without considering the proper base-rate values for product liability settlements. This is understandable, given that most of Bayer’s investors reside outside of the United States and probably aren’t aware of how frequently large jury awards are reversed on appeal in this country.

We estimate Bayer will do more than €6 billion in free cash flow by 2022 (>€6 per share), at which point we think the stock could be worth €100 from about €60 at quarter’s end.

We made two significant trades in the quarter. The first was a sale of our position in Samsung Electronics. When we first invested in the company in 2016, we thought investors in Samsung fell prey to “representativeness bias,” whereby they had mentally grouped the company with its less-profitable semiconductor peers. Despite consistent full-cycle margins of >20% and industry-leading semiconductor technology, Samsung’s business was valued like a melting ice cube, with common shares trading at only 5x trailing earnings after backing out net cash.

We bought the preferred shares which, at a 20% discount to common, offered an even better deal at a ~4x PE. As it turns out (and on this, we got lucky), earnings were set to skyrocket due to a supply crunch in the semiconductor segment. Earnings went from $20b in 2016 to $43b in 2018, and the price of the preferred ADRs doubled to over $900 per share. We ended up selling at between $750 and $800, as shares now trade at about a 10x multiple of our estimated full-cycle earnings.

With the cash we generated from the sale of Samsung preferreds, we doubled our stake in the French holding company Bollore SA. We are bullish on Bollore for a couple of reasons. First, due to a complicated web of crossholdings, the company’s true share count is roughly half of what is reported on its financial statements. We suspect that many investors have overlooked this information due to its obscurity, or ignored it due to its complexity, causing them to undervalue Bollore by a factor of two. Familiarity bias is at work here: investors are familiar with looking up reported share counts, and sometimes adjusting them upwards for outstanding warrants and options. But they probably haven’t seen many companies with a byzantine subsidiary self-ownership structure that decreases shares outstanding.

We’ve analyzed and transformed the crossholding data into the graphic below that we think demonstrates our claim about the share count in a clear and intuitive way.

The company also has a large and seemingly unappreciated stake in Vivendi SA, which owns the world’s most profitable music label Universal Music Group (UMG). Although shares of Vivendi trade at 25x street estimates for 2019e, we find this undemanding. With UMG accounting for >70% of profits, streaming revenues growing 30% year-on-year, and, according to our estimates, Vivendi EPS set to more than double between 2018 and 2023, we think it could trade much higher.

Investors may be suffering from anchoring bias, allowing the music industry’s mediocre past to anchor their expectations. Instead, we think that the business’s recent history -- which includes the rise of piracy and a concomitant drop in album sales -- are a terrible guide to a future that will soon see 200m paid streaming subscribers.

There are also fears that content owners will fail to profit from music’s streaming boom, similar to how cable networks ceded value to Netflix over the past decade. However, the structure of the music industry is not at all representative of the video industry. Music subscribers expect full coverage of the back catalog, and just three labels control the vast majority of that content. As such, we think labels are very well positioned to capture an outsized share of streaming revenues, evidenced by the 40% annual growth in streaming revenues at UMG over the past 3 years.

We aren’t alone in seeing the value at UMG, and Vivendi is currently in negotiations to sell Tencent a stake at a €30B valuation. Vivendi will likely use these funds to repurchase its own stock, increasing Bollore’s stake in the company. For our full thesis on Bollore, see our blog post.

After quarter end, Evan and his wife Sarah were elated to welcome their second daughter Sorenne into the world. All three are healthy and enjoying her first weeks of life.

We are grateful for your business and your trust, and a special thank you to those who have referred friends and family. There is no greater compliment.

- Bireme Capital

1 Net calculations assume a 1.75% management fee. Fee structures and returns vary between clients. FV inception was 6/6/2016.

2 Data from Ken French’s data library.

3 Data from Bloomberg, Compustat and FRED. To create the value spread, we screen out securities for which a simple summary statistic is unlikely to accurately reflect the market’s true valuation of a tradable security. For example, maybe a company’s fundamentals are wildly variable from year to year, or its accounting has some strange quirks, or the company is too small to really be investable, etc. We also exclude financials as they are substantially different than the rest of the market. Then we calculate fundamentals and market cap, making adjustments where appropriate (returnable cash, minority ownership, dilution, recent M&A, etc).

This results in three summary statistics (price to sales, price to gross profits, and price to book value) for a universe of roughly 1,000 investable US stocks every month-end since 1987. The most expensive third of this universe becomes our growth basket, and the cheapest third becomes our value basket. Taking the difference in valuations between the two baskets averaged across all three statistics gives us our value spread. To convert the value spread into a value factor return, we simply subtract the average one-month total return of stocks in the growth basket from those in the value basket, and rebalance every month.

We don’t actually use this metric in our investing; we do much more in-depth work on each security than merely the screening, adjusting and sorting seen here. But this metric is a useful tool to get a sense of the current opportunity set available in the market, and as an initial screen for high-quality ideas.

4 Data from Bloomberg.