Fundamental Value was up 9.1% net of fees in the third quarter, handily eclipsing the S&P 500’s return of 0.6%. FV has had a spectacular first three quarters of the year, returning 38.6% net vs 15.9% for the S&P. FV has now generated a net return of 25.6% annualized since inception in 2016, outperforming the S&P by 9.2% annually.1

Market commentary

In our last letter, Part III: Apex of a Bubble, we warned that an “everything bubble” had emerged in financial assets in response to decades of increasingly reckless fiscal and monetary policy. Valuations are at historical extremes in every corner of the US equity and fixed income markets. These extreme valuations presage real returns that investors will find severely disappointing -- and likely negative -- for many asset classes over years to come. Our warning remains as urgent as ever.

A leading candidate to pop the everything bubble is persistent inflation. In Part III, we posited that inflation was likely not transitory, despite the Fed’s insistence otherwise. Incoming data since publication has supported that view. Inflation pressures are broadening. Proponents of the transitory narrative had pointed to restrained median CPI inflation as evidence that only a few reopening sectors were driving the increase in headline inflation; now the median CPI exceeds the headline figure. Commodities and energy prices are soaring. Supply chain snarls are worsening rather than improving.

We said that both shelter and wage inflation were almost certain to rise. Since then, the Case-Shiller National Home Price Index rose by 19.8% YoY, setting yet another new all-time high. The shelter component of CPI rose from 2.8% YoY to 3.2% -- a large change in one month, but still only beginning to reflect the underlying price pressures. Wage pressures have continued to escalate as well. Every month, small employers report off-the-charts new records on nearly every employment metric: compensation increases, difficulty filling job openings, etc. The Atlanta Fed’s Wage Growth Tracker reported a sharp rise to a 4.2% YoY pace, the highest since 2007, but still significantly lower than headline inflation. We think both shelter and wages have more room to run.

Most worryingly, inflation expectations are soaring. 5-year TIPS breakevens rose more than 0.5% in the past month alone to an all-time high. Long-term breakevens (inflation expectations for the 5-year period that begins 5-years hence) broke out to their highest level since 2014.

The Fed is beginning to acknowledge the reality: several Fed governors have dramatically changed their tune on inflation in just the last few days. In our view, an increasingly hawkish Fed is a good sign for the long-term health of our economy, but a very troublesome sign for asset prices that rely on excessively easy monetary policy.

Despite the dismal return prospects for the bond and equity markets as a whole, we believe Bireme clients are well positioned to outperform. For more detail, please see Part III: Apex of a Bubble.

Portfolio commentary

Long book

The biggest driver of YTD returns was RCI Hospitality (RICK), which is up 80% -- from $39 to $70 on the back of extremely strong operating results. Their nightclubs grew revenue 8% vs 2019 to record highs. In their restaurant segment, sales increased 80-90% vs both 2020 and 2019 as they opened new locations and notched large gains in same store sales.

During the third quarter, the company announced a transaction which demonstrates the firm’s long-term opportunity to roll up mom-and-pop operators. This deal, for 11 mostly Colorado-based nightclubs, cost a total of $88m and amounted to an EBITDA multiple of 6.3x, far lower than the median 11.4x multiple paid by private equity firms in 2020. When we run the math, it appears that RICK’s $40m in equity invested will generate about $7.5m in additional free cash flow to stockholders (net of interest payments on the $48m in debt), indicating a return of about 18.6%. Companies with this sort of reinvestment opportunity are rare, and don’t typically trade at less than 20x free cash flow multiple, like RICK does. RICK remains a large position.

Bollore has also had a very good year, with the stock appreciating from 3.3 EUR to 5.0 EUR, a gain of more than 50% per share. This increase has been helped by strong operating results as well as the spinoff of their largest asset, Universal Music Group.

We’ve been talking about Bollore for years. We first presented the company at ValueX Vail in 2017, where we highlighted the strength of their core transportation and logistics business. This segment operates worldwide, with 34,000 employees coordinating the transportation of commercial goods between more than 100 countries. Their Africa operation is the largest on the continent, and includes 16 container terminal concessions. At those ports Bollore is paid a substantial fee every time a shipping container is unloaded.

This business has generated more than 500m EUR of EBITA each year since 2016. This is despite a tremendous drop in global commodity prices during that period. Revenues were even resilient during the COVID-19 pandemic, growing 1% in 2020. And 2021 has been even better, with the segment seeing sales growth of 13% and EBITA growth of 17% for the first half of the year.

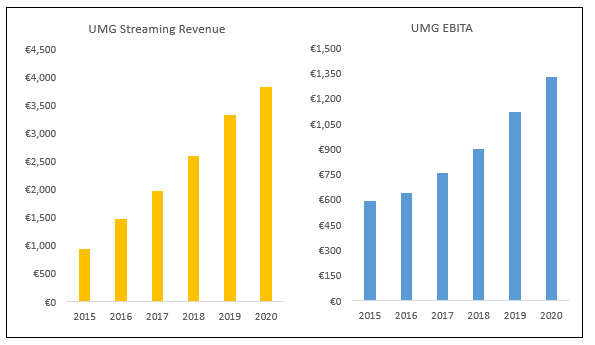

But the gem in Bollore’s portfolio is its stake in Vivendi SA which was the focus of our 2019 writeup. Vivendi has doubled EBITDA since 2016 from 1.2b EUR to 2.4b EUR in 2021. The primary driver has been their subsidiary Universal Music Group (“UMG”), one of the largest owners of recorded music in the world. Along with the two other major labels, UMG collects the majority of music royalties worldwide and has been a beneficiary of the boom in streaming audio. Streaming revenues at UMG have rocketed from 1.5b EUR in 2016 to 3.8b EUR last year, more than making up for a decline in album sales.

There are few industries that seem as certain to grow as streaming music.

We are of course not the first people to realize this, and outside investors have been clamoring for a piece of UMG for years. Vivendi finally began to monetize this interest in late 2019, with a Tencent-led consortium eventually

taking a 20% stake at a 30b EUR valuation. Most of the remaining shares were

spun off to Vivendi shareholders (including Bollore) in September 2021 and are now publicly traded on the Euronext exchange. Universal Music’s market cap is currently 45b EUR, a massive premium to Vivendi’s year-end market valuation of 28b EUR.

Post spin, Bollore became UMG’s largest shareholder, controlling 326.5m shares or 18% of the total. These shares are worth 8.1b EUR to Bollore at UMG’s current share price or about 5.78 EUR per Bollore share. So despite the rise in share price, Bollore still trades at a substantial discount to its holding in UMG, ignoring the substantial value of the transport and logistics assets.

Old Republic (ORI) shares rose 34.6% in the first half of the year, from $18.51 to $23.31, yet it is still one of the cheapest stocks in our portfolio. We added to our position earlier in the year.

For the current market capitalization of just over $7b, Old Republic investors own the following:

- An $11.2b fixed income portfolio (part of the insurance float)

- A $5.2b stock portfolio (also float)

- A title insurance business with about $400m of trailing underwriting profits

- A general insurance business with $150m of trailing underwriting profits

Even if you haircut the bond portfolio by 50% to account for double taxation and only value the underwriting profits at 10x earnings, the intrinsic value of these pieces would still be over $14.3 billion dollars, nearly double the current market price. On a PE basis ORI trades at just 11x the record 2020 earnings of $670m.

Sellers of this stock seem to be falling prey to representativeness bias, lumping the firm in with other title insurers despite that business being a minority of its profits. While it may make sense for pure play title insurers to trade at 10x earnings or so since that business has historically been cyclical, this is an extremely low multiple for a well-run general insurance company. In fact, ORI’s general insurance business has such a strong track record of underwriting profits -- 14 of the last 15 years -- that it may even be worth a premium to peers trading at 15x or 18x earnings. On a book value basis, most comps trade at 1.5-1.8x book value, 30-50% higher than ORI’s price today (before even considering the value of the title insurance segment).

This discrepancy was recently highlighted by an activist shareholder named Owl Creek partners. In their

letter dated 4/6/21, they lay out the investment case for Old Republic shares, concluding that the company should spend less money on dividends and more money buying back the undervalued stock. We wholeheartedly agree. We also welcome the proposal of a declassified, diversified board with an independent chairperson. The time has come for a more modern approach to governance and capital allocation at this nearly 100-year-old business.

During the third quarter, we added one new long position to the portfolio, a tobacco company called Imperial Brands. At less than 7x earnings, this centuries-old firm is one of the cheapest stocks (relative to current earnings) we have ever invested in. Investors selling at these levels appear to be falling prey to social conformity bias, following the herd out of supposedly unsavory industries without considering financial returns.

We see Imperial as a company with solid brands and consistent profits, and hardly deserving of one of the lowest multiples in the entire stock market. While the company has struggled to build a profitable business in so-called “next-generation” products like smokeless tobacco, we think their traditional brands and growing cigar business should provide plenty of profits to sustain, and perhaps even grow, the 9% dividend yield.

If you are interested in diving into this idea further, please see our full writeup

here.

Short book

In

Part II: Anatomy of a Bubble, we discussed the epic bubble in highly speculative securities. Much of that excess still persists. While we believe there is still a long way down ahead of us, individual bubbles have begun to deflate.

GSX (now GOTU), a Chinese education company which was

accused of falsifying a majority of its online customer base, has seen its share price whipsaw in 2021 from $50 to $140 to today’s price of below $4. The plunge began in early March, as GSX announced earnings

results that included a wider quarterly loss and a 30% weaker Q2 revenue forecast than Wall Street had expected.

Then a few weeks later

rumors surfaced of an impending regulatory crackdown on for-profit education companies in China. Simultaneously one of their largest shareholders, Archegos Capital Management, was collapsing. Archegos’s margin calls

forced their brokers to sell massive blocks of shares in various tech and media stocks, including GSX, which seems to have hastened the price decline.The final nail in the coffin for GSX came on 7/23, when Chinese regulators

banned for-profit after-school tutoring.

FuboTV, an over-the-top TV company, also saw its price collapse from a February peak, in this case from $50 down to about $26 today. We remain convinced that this business is the classic case of selling a dollar for 90c. The company did not even make a gross profit in 2020, with subscriber expenses and broadcasting costs totalling $234m against just $218m of revenue. And since content costs for vMVPDs tend to increase nearly linearly with subscribers, we expect the company to continue to lose money.

Yet the market cap for FuboTV remains at nearly $4b, as investors pray that a future sportsbook slapped onto their TV business will somehow stem the tide of red ink. To get there the company may need to raise significant capital given that the firm had a $149m operating cash outflow in 2020. We remain short FUBO.

But while a few stocks have cratered, the vast majority of overpriced stocks continue to levitate, which we have used as an opportunity to initiate new short positions. Let’s first talk about Gamestop, the focal point of the Reddit WallStreetBets mania which peaked earlier in the year.

Remarkably, Reddit traders have initiated not one but two stratospheric climbs in the GME share price since the start of the year.

In January, the shares reached $300, up from $10 last October. This surge entered the national conversation as almost no other stock run in history, prompting both a Congressional investigation and a

mention on Saturday Night Live. Short interest

collapsed from 71m shares to 10m shares and eventually the share price did too, settling at $50 by the end of February. What’s more impressive is that the Reddit crowd has fueled a second rise in GME, with shares now trading at over $170.

Gamestop (GME) has no realistic chance of meeting the expectations implied by these prices.

Gamestop’s current market capitalization is about $13.5b. This means that one day the firm will likely need to earn >$500m in profits (implying a ~4% earnings yield) to generate a positive return. But Gamestop has never earned $500m in a single year. The company’s peak profitability was way back in 2016 when it netted $415m. Profits have been declining ever since, including massive operating losses of $400m in 2019 and $238m in 2020. Revenues have declined precipitously as well, from $8.3b in 2018, to $6.5b in 2019, to just $5.1b in 2020.

The problem is not the video game industry, which is booming. Here are 2020 sales results for the major game companies:

- Activision Blizzard: $8.1b revenue, +24.6%

- Electronic Arts: $6.1b, +16.8%

- Nintendo: $15.6b, +29.9%

- Take-Two Interactive: $3.4b, +14.0%

Plenty of video games are being sold -- just not at Gamestop. Most of them are being downloaded. For example, AAA console game publisher Take-Two Interactive

generated more than 90% of revenue via digital channels in Q2 2021. This trend spells doom for Gamestop, and the likelihood of this outcome is why GME traded at single-digit PE multiples even when the company was profitable.

Gamestop’s new management team cannot stop this trend. And while we respect what Ryan Cohen, the new chairman and major shareholder, was able to do at Chewy.com, we think he will find the business of selling discs to be much different than pet food.

At Chewy, his business was the disruptor, selling online against store-based incumbents like PetSmart. This involved setting up distribution centers and shipping physical products to end users. But in video games, shipping a physical product -- even if the item was purchased online -- is the outmoded method of distribution. Gamestop, and even Amazon itself, are the ones being disintermediated in video games.

The disruptors are the owners of the digital platforms: Sony, Microsoft, Nintendo, Facebook, and a few others. Gamestop cannot sell downloadable Playstation games. The closest they get to participating in digital downloads is selling Xbox game codes, which must be redeemed on the Xbox platform. This means that you pay on Gamestop.com, wait for an email, write down the code, bring it to your Xbox, and enter the code. This cumbersome process cannot compete with the simple act of hitting “purchase” on your console, where any gamer worth his salt has already saved a credit card. Gamestop will never be a significant player in this market, and we think there remains massive downside for Gamestop shares. We are short.

Another short position we initiated was in Skillz (SKLZ), a mobile game publisher with $230m in 2020 revenue, and $98m of 2020 EBITDA losses. When we shorted it, SKLZ had a ~$6b valuation; it is now down to $4.5b, and we believe it has much more room to fall.

SKLZ is a great example of investors getting hyped up over a quickly-growing company employing misleading industry jargon. In this case, the jargon is “eSports.” eSports is, in fact, a large and growing industry, and the term describes the business of competitive video games. Typically, this involves hosting tournaments, either live or online, where spectators can watch professional gamers compete at high levels. Prize pools are often in the millions. Ticket sales, sponsorships, and advertising revenue from such events

totaled over $1b in 2020.

Skillz games are not eSports, despite the following website headline:

As you can see from this

list, Skillz apps are simple games like Solitaire and Bingo. What supposedly makes this “eSports” is the fact that players can bet on their own games. We have nothing against simple games, but this is not remotely the same business generating millions of dollars from hosting a League of Legends or Madden tournament. Calling Skillz games “eSports” is like calling the game at the local fair where you take jump shots to win a stuffed animal “professional basketball.”

Skillz is actually just an online casino.

In fact, the Skillz business model is similar to an online poker game: players bet money against one another, with most of the pot going to the winner and the operator taking a small cut. And every casino operator knows that poker is the

least profitable game that they offer.

The obfuscation of the word “eSports” is deliberate, because investing in an online casino business doesn’t get most people excited. The casino business is extremely competitive, requiring large customer bonuses and marketing spend to ensure more players are coming in than going out. This is probably why SKLZ spent more on sales and marketing than they had in total revenue in 2020, Q1 2021, and Q2 2021. It is difficult to generate profits with this model. And let’s be clear: this is not some sticky software business, where customer acquisition spend can legitimately be amortized over a period of many years. In the online casino world, customers often run to the app with the best deposit bonuses.

We remain short SKLZ.

- Bireme Capital

Follow our content by subscribing here.

1 Net calculations assume a 1.75% management fee. Fee structures and returns vary between clients. FV inception was 6/6/2016.