The World's No. 1 Inflation Protection Investment

By: Dr. David Eifrig

I'm sure you've noticed that prices for almost everything are absolutely soaring.

At the same time, we're running out of... well... practically everything from computer chips to appliances to building supplies.

Maybe you've heard the stories of crazy bidding wars for houses...

Like a simple three-bedroom house in Covina, California, selling for $650,000, which had 126 showings and 50 offers in four days. One bid was even $100,000 over the asking price. In the most desirable parts of Texas, real estate agents now bring in food trucks and coffee vendors to make the lines more bearable at open houses. This scenario is playing out all over the country.

Vacation rentals are going through the roof as well. As hard as this is to imagine, a home in the Hamptons just rented for the summer for a whopping $2 million. Rental prices across the board are up 100% or more. In resort towns nationwide, rentals are completely booked.

The more you dig into the numbers, you see soaring prices and shortages for practically everything we need and value in our society.

Oil prices are up more than 90% in the past year. Food prices are up 5.5%. Paper prices are up 20%. Copper prices are at an all-time high.

Car prices are sky-high, too. The average price of a new car topped $45,000 for the first time earlier this year, and the average used car now costs more than $26,000.

The Kaiser Family Foundation reports the average cost for employer-based family health coverage is now a whopping $21,342 per year.

Prices for food, health care, commodities, shipping, electricity... it's all rocketing higher.

Why?

There are many reasons for the soaring prices of all these things. The economy is returning to normal. People want to live in bigger houses. The supply chain is a mess. And people want to get out and spend again.

But there's something else really happening here. Here's what you need to know...

It doesn't matter how the White House, the U.S. Treasury, or the Federal Reserve are creating new money and new credit. It doesn't matter what tricks they are using or how they spin it.

America is about to experience one of the greatest inflationary periods in our nation's history.

And make no mistake about it: Inflation will push millions of Americans down... out of the middle class, out of private retirement, out of private health care, and out of a decent life based on independence and privacy.

When a currency collapses, people are trapped by their own dollars and their own deeply indebted government.

I know you probably think this sounds outlandish. You probably think this is all just temporary.

Most Americans, I'm sure, are feeling pretty good.

Home values are sky-high. So are stocks. Your brokerage account may have never looked better.

But here's the truth no politician will bother sharing:

Prices for all of these goods and services... prices for stocks and houses and art are NOT going up the way you think they are. Instead, it's the value of our money going down.

This is what ALWAYS happens at the start of a period of massive inflation and a collapsing currency.

Economists call it the "Money Illusion."

It's what happens when people start to measure their wealth in simple numeric terms instead of real terms – in other words, how many dollars you have instead of what your dollars can buy.

This is what happens when people don't take into account money-printing, increased debt, and inflation, and wrongly believe a dollar today is worth the same as it was last year, even after the Fed has pumped trillions and trillions of new dollars into the system.

Think of anything of significance you've bought recently... a washing machine or refrigerator... tires... furniture... it's all soaring in price – and that's if you can find it, because supply shortages are rampant.

Inflation causes huge economic distortions, which is one of the reasons why, as Bloomberg recently reported, we are "suddenly running low on everything." And while you may have more money in your bank or stock account, it's definitely not worth anything close to what it was just a year or so ago.

I estimate that more than 90% of the American public is falling for the Money Illusion today... Most folks are in complete denial about what is really happening in our financial system.

But when you look back at financial history, you realize this is nothing new...

Massive inflations are always incredibly confusing to the general public.

Look at Germany's Weimar Republic in the early 1900s, for example... the most famous case of inflation and currency collapse in history.

Over a period of about 10 years, the German mark eventually became worth one million-millionth of its former self, surging from an exchange rate of 4.2 marks per U.S. dollar in 1919 to 4.2 trillion marks per U.S. dollar just four years later.

To outsiders, it was obvious Germany was destroying its currency. But locals simply held on, in a state of confusion and denial... even as inflation exploded exponentially.

As a German woman told Nobel and Pulitzer Prize-winning writer Pearl Buck:

We used to say, "The dollar is going up again," while in reality the dollar remained stable but our mark was falling. But... we could hardly say our mark was falling since in figures it was constantly going up – and so were the prices – and this was much more visible than the realization that the value of our money was going down... It all seemed just madness, and it made the people mad.

Economic historian Adam Ferguson explained why in his book When Money Dies:

It was the natural reaction of most Germans, or Austrians, or Hungarians – indeed, as for any victims of inflation – to assume not so much that their money was falling in value as that the goods which it bought were becoming more expensive in absolute terms.

And this is exactly what's happening in America right now.

Unfortunately, the sad truth is most Americans will do the exact same thing Germans, Hungarians, and Austrians did with their soon-to-be-worthless currencies, even after they'd been devalued for the umpteenth time...

They will cling to their increasingly worthless money.

You see, the Money Illusion inevitably creates a frenzy... encouraging massive gambling, hoarding, and speculation... as everyone attempts to keep up with the "get-rich-quick" stories reported in the press.

I'm sure you know what I'm talking about in our country today...

What Happened 50 Years Ago Is About to Happen Again

From 1961 through 1965, annual U.S. inflation averaged just 1.28%.

Then in 1965, President Lyndon Johnson began massive spending and took on huge budget deficits for the Vietnam war and his "Great Society" benefits... which included Medicare, Medicaid, Head Start, urban renewal, environmental initiatives, new immigration policies, and more.

It sure sounds a lot like the new programs being proposed today, doesn't it?

Back then, just like today, inflation was gradual at first. It climbed to 3% in 1966 and 2.8% in 1967. And in large part because of the Money Illusion, people continued to feel richer and richer as the S&P 500 Index hit an all-time high in late 1968.

Then things began to spin out of control...

Inflation reached 5.97% in 1970. By 1974, inflation hit more than 11%, and the stock market had lost 35% of its value. Inflation finally peaked at 13.5% in 1980.

In one incredible five-year stretch from 1977 to 1981, cumulative inflation was over 50%... In other words, the value of your savings was essentially cut by a third.

Even so, U.S. citizens during this period made the same analytical mistake Germans, Austrians, and Hungarians made in the 1920s.

Their initial perception was that prices were going up – but what was really happening was just the opposite: our currency was collapsing.

As currency expert Jim Rickards says, "Higher prices are the symptom, not the cause, of currency collapse."

Few Americans today recall that the dollar nearly ceased to function as the world's reserve currency back in 1978.

In fact, that year, the U.S. Treasury was forced to issue government bonds denominated in Swiss francs.

The point here is that inflation always gains substantial momentum before the general public notices, and before politicians act – and that's exactly what's happening right now in America.

The last time we saw serious inflation, it was not until 1974 – nine years after the inflationary cycle began – that it became a big political issue and prominent public policy concern.

Millions of Americans lost a fortune in stocks. Their savings were worth just a fraction of their previous values.

That's why you need to learn about inflation, how it works, and how it may happen in the coming years.

And you also need to know just how it may change our politics and society. Money is important. If the value of everyone's cash is changing drastically, there are winners and losers... and people get agitated.

The No. 1 Inflation Protection You Can Buy Today

Today, there is one simple thing that every single American should do with their cash...

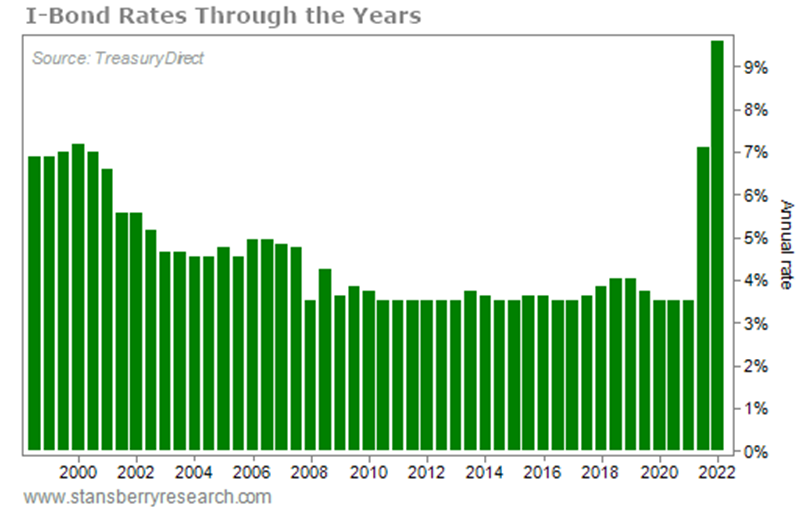

Buy the maximum amount of I-bonds you can.

The U.S. government created I-bonds in 1998 to offer savers a way to stash their savings, earn a decent yield, and remain protected from inflation.

They've long paid a generous rate... so generous that the government had to limit how much you could buy. However, directing a portion of your tax return allows you to get even more cash into I-bonds.

After checking the newest yields – rates which look almost unbelievable in today's zero-yield world – I fired off an email to my research team...

This is FOR EVERYONE who's ever thought about investing...

This should be DESIGNED up with RED, WHITE, and BLUE colors, GREEN BACK colors... shouted from the mountain top...

Inflation STOPPER courtesy of Uncle Sam... we WANT YOU!!

This is an income investor's dream. And we're not the only ones to realize it... even though most people are still in the dark.

The always-insightful Jason Zweig recently published a column in the Wall Street Journal highlighting I-bonds as well.

We don't like to repeat advice published in the newspaper, but delivering our readers the best investment opportunities trumps our desire to be original or have the story first.

Zweig notes that almost no one ever thinks of I-bonds when they look for yields...

Zvi Bodie, a consultant on retirement issues who formerly taught finance at Boston University, says he regularly speaks to groups of financial advisers. When he asks how many are familiar with I-bonds, "less than half the hands go up" in the audience.

But I-bonds are a phenomenal place to park cash safely and earn returns hundreds of multiples of what you'd get in a bank account, and four times what you'd get in a certificate of deposit.

Here are the key points:

You can earn a whopping, incredible return of 9.62%, which is indexed to inflation. Also, returns aren't subject to local taxes. And the bonds are backed by the "full faith and credit" of the United States government.

The biggest hurdle here is that any single account holder can only buy $10,000 worth of I-bonds per calendar year. However, you can also buy up to $5,000 with your tax refund, meaning you can total $15,000.

You can't build your entire portfolio around I-bonds, but it's a great place to park $10,000.

You buy I-bonds directly through the U.S. Treasury at treasurydirect.gov.

But to ensure they make sense for you, let's walk through all the details...

- The interest on bonds is recalculated every six months. The rate is a combination of a fixed rate plus an inflation rate based on the Consumer Price Index ("CPI"). You will earn the headline rate for six months, it will be recalculated, and you'll earn that for the next six months.

- If inflation turns negative, the bonds can yield zero, but they never have negative rates.

- Interest earned is added to the principal value for the next six months, so you will see the benefits of compound growth.

- These are intended as long-term holdings. You cannot redeem your bonds for 12 months. After that, if you redeem within five years, you will forfeit the last three months of interest you collected. After five years, you pay no penalties and can hold for a total of 30 years.

- Tax situations are highly personalized, but in general there is no state or local income tax on interest earned. Federal income tax is due, but it's possible in some instances to avoid that by using the bonds to pay for education.

Today's bond starts with a fixed rate of zero, given the prevailing low rates of the day. The annual rate is currently 9.62%.

If inflation or interest rates pick up, I-bonds can pay even more. (While we're certainly expecting higher inflation, an increase in short-term interest rates by the Fed to choke it off is possible as well.)

Again, to buy I-bonds, you need to set up an account at treasurydirect.gov. You buy them directly from Uncle Sam. There are no brokerage fees. Your financial adviser won't take 2% of your assets under management. (This may be why Wall Street hasn't been telling you about it.)

If you buy with your tax return by using IRS Form 8888, you can actually get paper bonds. These bonds are registered in your name and are non-transferrable, so there's not really any advantage to holding the certificates. But we do think the nostalgia of having a few paper bonds in the safe is enjoyable.

We give I-bonds our full recommendation. You're going to earn a healthy, inflation-adjusted return you really can't get anywhere else. If you've got some cash on hand, you can protect your purchasing power and earn a real return in the safest of securities.

What About the Rest of Your Portfolio?

Of course, there is one downside to I-bonds...

You can only buy $10,000 per person.

So what do you do to protect the rest of your retirement from inflation?

We talked earlier about the many similarities between the inflation unfolding today and what happened in America in the 1970s. But the inflationary script for the next few years in America will look quite different than it has in the past.

We are on a dangerous path in America.

Our government has set us on the road to currency devaluation and a new era of inflation.

Some assets are going to suffer, big time. Others will skyrocket in value. The wealth gap will get wider than ever before.

But you can potentially grow and protect your wealth in the years to come.

Sadly, this crisis is all going to tear our country apart over the next few years...

On one side will be those who understand what's happening, who take the necessary steps. These folks will continue to get richer and richer.

On the other side... well... unfortunately, that's most Americans... who won't understand what's going on... and will cling to a collapsing currency, falling further and further behind.

For yourself, and your family, get the facts. Learn how to take advantage of this trend so you are not left behind.

There's no doubt we're in for huge changes to our financial system in the next few years.

If you are counting on IRAs, 401ks, insurance policies, annuities, pension plans, stocks, or bonds, this information is critical.

I believe we'll have an extraordinary retirement crisis, and programs retirees are counting on today (such as IRAs, 401 k s, insurance policies, annuities, pension plans, etc.) collapse in REAL value.

Consider this your final wake-up call...

Billionaires including Warren Buffett, Stanley Druckenmiller, Paul Tudor Jones, Bill Ackman, and more have stated publicly that Americans aren't paying enough attention to this development.

That's why I have gone public with what I believe is the most important and useful analysis on this situation in the financial world today. You can access my latest analysis by clicking right here.