Triple Your Money on the Dividend King of the Dow

I became an investor at an incredibly early age – three days old. My grandfather bought me five shares of AT&T (NYSE: T).

I became an investor at an incredibly early age – three days old. My grandfather bought me five shares of AT&T (NYSE: T).

Throughout my childhood, I would get a dividend check for a few bucks every quarter.

Unfortunately, no one told me about the power of reinvesting dividends back then (if only someone had given me a copy of Get Rich with Dividends).

The dividend money probably went towards baseball cards that my mother ultimately threw away when I was older.

In my early twenties, living in Manhattan on $500 a week but with a girlfriend who had expensive tastes, I had an epiphany.

I've got those shares of AT&T I could sell for a few hundred bucks. That would help pay a month's rent or, what it was likely used for, keeping the girlfriend happy for the weekend.

If I had held onto those shares and reinvested the dividend, I'd be sitting pretty today.

AT&T is one of the highest-yielding non-REIT or MLP stocks in the market, currently sporting a fat 5.5% yield.

In fact, it is the biggest dividend payer in the Dow Jones Industrial Average.

Fortunately, you understand how reinvesting dividends can make you wealthy. Even today, AT&T is a perfect stock for this strategy.

Over the next few minutes, I'm going to show you how you could more than triple your money on the stock. All you'll need is a little bit of time.

But first, let's talk about AT&T.

It's Really Not Complicated

In addition to its 5.5% yield, AT&T has raised its dividend every year for 30 years.

That was the same year "Terms of Endearment" won the Oscar for best picture, Culture Club's "Karma Chameleon" hit No. 1 on the Billboard charts and when the Bell System broke up and AT&T divested itself from local phone companies.

That was a long time ago. And it has raised the dividend every year of its current existence.

The company provides service to 30 million landline customers, 16 million internet customers and 5 million television customers.

It is also the largest wireless provider in the world with an incredible 109.5 million subscribers. That compares to No. 2 provider Verizon's (NYSE: VZ) 101.2 million.

AT&T and Verizon dominate the wireless market. And when it comes to business services, AT&T's scale makes it a formidable foe.

Additionally, it operates the fastest and most reliable 4G LTE network with voice coverage in 225 countries and data roaming in 210 countries.

Despite its enormity, AT&T is still in growth mode. Wireless revenue was up 5.1% in the third quarter of 2013 and the company has experienced 19 consecutive quarters of Average Revenue Per User growth.

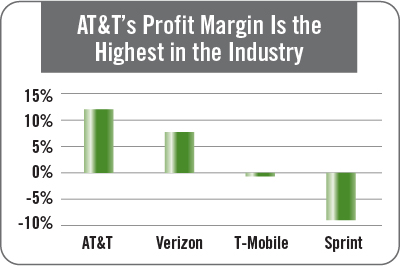

It also has the best profit margin in the business – by far.

T-Mobile (NYSE: TMUS) and Sprint (NYSE: S) aren't even profitable.

Verizon's net margin was 7.4% in the third quarter, versus AT&T's at 11.9% (which was higher than the 11.6% it recorded a year ago).

Collect, Reinvest, Repeat

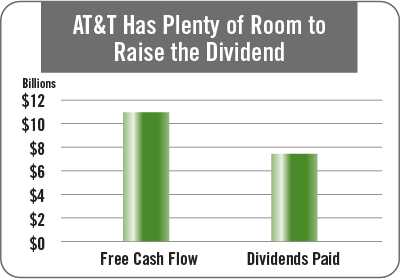

As you can probably imagine when you pay your wireless bill every month, AT&T generates tons of cash. In the first nine months of 2013, free cash flow (cash flow from operations minus capital expenditures) totaled $11.1 billion.

During that period, it paid out $7.3 billion in dividends for a payout ratio of 66%.

And the growth should continue, as well.

AT&T is expected to generate over $17 billion in free cash flow in 2014 and 2015.

Earnings per share are projected to grow to $2.66 in 2014 from $2.48 in 2013, giving the stock a forward P/E of just 12.7. That compares with 13.7 for Verizon.

You won't get huge dividend growth out of AT&T but, with a starting yield of 5.5%, you don't need to in order for the stock to qualify for the 10-11-12 System.

Assuming the same average 2.3% annual dividend increase of the past three years and that the stock trades in line with the market average, over the next 10 years, AT&T investors should see an average annual return of over 12.2% (with dividends reinvested).

That will more than triple your money in 10 years in a safe, high-yielding stock. Now if only I started reinvesting that dividend 40 years ago.

Action to Take: Buy AT&T (NYSE: T) at the market for the Compound Income Portfolio.

"Superfy" Your Dividends

AT&T's 5.5% yield is strong in today's market. But some investors are looking for even more.

Fortunately, there's a way to capture an even higher yield. And no, you don't have to go investing in a different stock.

It's a different mindset than the Compound Income Portfolio strategy where we're buying the stock with a plan to hold it for years... decades even.

In this other strategy, we're going to "rent" the stocks instead of buying them – meaning we'll be fine if we have to sell it as we're simply using the stocks to capture extra income.

Here's how it works:

- Buy a stock with an upcoming ex-dividend date.

- Sell a covered call slightly out of the money that expires right after the ex-dividend date.

Let's use AT&T as our example.

As I write this, the stock is trading at $33.70. So we buy 100 shares at $33.70.

The company's most recent ex-dividend date was January 8.

It hasn't announced the next one, but it will likely be in early April.

So we'll sell the AT&T April $34 call for $0.80.

That means the investor will collect $80 (options are priced in 100 share contracts).

By selling the call, he is selling the right for the buyer to purchase his stock for $34 by the third Friday in April (options expire on the third Friday of the month), no matter where the stock is trading.

By selling the call, the investor collects the $0.80 per share option premium plus the $0.46 per share dividend.

Because the ex-dividend date will probably be before options expiration, the shareholder will likely still own the shares and be entitled to the dividend.

If, at expiration, the stock is not above $34, the investor keeps his stock and has collected $1.26 or $126 for every 100 shares, or 3.73%.

Remember, that's 3.73% in just three months.

That's the equivalent of the full-year yields for many quality stocks.

Annualized, that comes out to 14.9%.

If the stock is trading above $34, the stock will be called away and the investor sells his shares at $34, capturing an additional $0.30 capital gain.

In that case, the $0.30 is added to the $1.26 and the investor has earned 4.6% in just three months or 18.5% annualized.

Let me emphasize that to use this strategy, the investor has to be OK with selling his stock.

It is simply a vehicle for earning extra income, not a long-term investment – although an investor can easily reinvest his dividends and the option premium into the stock to increase the share count to generate even more dividends and option premiums.

Yields of 14.9% or 18.5% probably sound pretty good.

But using this strategy, I'm targeting 20% annualized yields at a minimum.

If this sounds interesting to you, check out my new service Dividend Multiplier. Give it a try and let me know what you think.

(Please note: The above covered call example using AT&T is not a recommended trade, it's just an example. The recommendation to add AT&T to the Compound Income Portfolio is official, however.)