Creating income for today, wealth for tomorrow | Issue 56, November 2017

Cash In on the Crypto Craze Without the Insane Risks

This 3.9% Yielder Is a Leader in Blockchain Technology

Dear Member,

My dad isn’t a big risk taker.

So it was no surprise that, when I graduated, he strongly urged me to look for a job with a big, safe company.

Back then, IBM (NYSE: IBM) was considered the model of stability. And its global headquarters is located just a few miles from where I grew up.

At the time, its revenue was $62.7 billion and it had nearly 400,000 employees worldwide. It was the fifth-largest company on the planet and the most profitable one.

I had zero interest in working for a giant computer company as I knew nothing about computers other than what I’d learned in a class I took in BASIC my sophomore year

in college.

So every time my dad asked if I’d sent my resume to IBM, my answer was “not yet.”

Today, I find it ironic that this company is viewed as a slow-moving behemoth, when in fact it is the world leader in a new technology that is going to revolutionize the way business is conducted.

I’m talking about blockchain technology.

If you’ve heard about blockchain, it’s probably been in relation to cryptocurrency – bitcoin and the like.

While it’s true that cryptocurrencies use blockchain, it’s not crypto that has me excited. It’s the other blockchain uses that are going to generate enormous profits for companies that use the technology as well as those that provide and/or service it.

What Is Blockchain?

Blockchain is basically a ledger that is used for keeping track of transactions. But rather than being hosted on a central server, the blockchain is hosted on tens of thousands of computers around the world. This decentralized network of individuals’ computers verifies transactions and keeps track of everything from cash to mangoes to container ships full of oil.

Blockchain is safer than most systems. Its biggest supporters say it’s impossible to hack. I won’t go that far, but it is difficult to hack thanks to the large number of computers needed to confirm a transaction.

The blockchain confirms that any cash, mango, ship full of oil or other store of value belongs to the person who is sending it. It’s as if every time you paid for something in cash, someone verified that the serial number on the bill you were spending rightfully belonged to you.

In a supply chain, there is a long paper trail and each player has their own systems. That causes delays and headaches. The blockchain is transparent and allows everyone involved in the transaction to see each step.

This has major implications for commerce.

Wal-Mart is now experimenting with blockchain. A Wal-Mart executive wanted to find out where a package of mangoes originated from. It took nearly a full week to get an answer. Using blockchain technology, he was able to find out instantly. He learned not only where the mangoes were picked but who had possession of the fruit every step along the way.

Imagine the safety benefits of information that can be retrieved that quickly – especially when there’s an outbreak of foodborne illnesses.

It can speed up the delivery of important goods like oil. When a ship full of oil leaves port, that oil is often bought and sold many times en route to its final destination. Each transaction has loads of paperwork and takes hours to complete.

But recently a cargo ship containing $25 million of African crude delivered the oil to China. Along the way, the oil was sold three times. Using blockchain technology, each trade was done in less than 25 minutes.

Blockchain’s growth is about to explode. Two-thirds of the world’s largest companies expect to deploy blockchain technology by the end of next year. And 91% of financial services executives say blockchain is critical to the future of their firms.

And there’s little doubt who the global blockchain leader is.

“They’re Still a Company?”

IBM was created more than 100 years ago and has reinvented itself several times. In 1911, the company that became IBM sold scales, meat slicers and time recording products. From there, it went on to make giant mainframe computers, PCs and the supercomputer Watson.

And with blockchain, IBM will begin another chapter in its prestigious history. It is already in collaboration with Wal-Mart, Unilever, Nestlé and several other large companies to track the movement of food. The mango example earlier was done with IBM’s technology.

It has teamed up with four international banks to help facilitate trade finance, as with the African oil example. And it was recently selected to build a blockchain-based trading platform for seven of the world’s largest banks.

Tell your friends at a cocktail party you’re investing in IBM, and they’ll likely have the same reaction my hedge fund buddy did when I mentioned the name... “They’re still a company?” he asked sarcastically.

However, ask any technology executive about IBM and they will have a very different response. In fact, 43% of tech executives say IBM is the best-positioned company when it comes to blockchain.

According to trade publication Data Center Knowledge, “IBM definitely has a lead when it comes to blockchain technology, having been involved in its development almost since the day people first realized that distributed databases might be useful outside the realm of cryptocurrencies.”

Of course, IBM isn’t only about blockchain. It has invested $30 billion in growth areas such as cloud technology, security, analytics and mobile technology. The cloud alone is expected to grow from a $33 billion market in 2015 to $228 billion in 2026, a 591% increase.

And of course, IBM’s Watson is the leader in artificial intelligence. Watson is famous for having won the game show Jeopardy! but its real-world uses go beyond impressing Alex Trebek.

Watson helps diagnose and treat patients with a wide variety of illnesses, helps financial managers analyze risk, and personalizes retail experiences for customers.

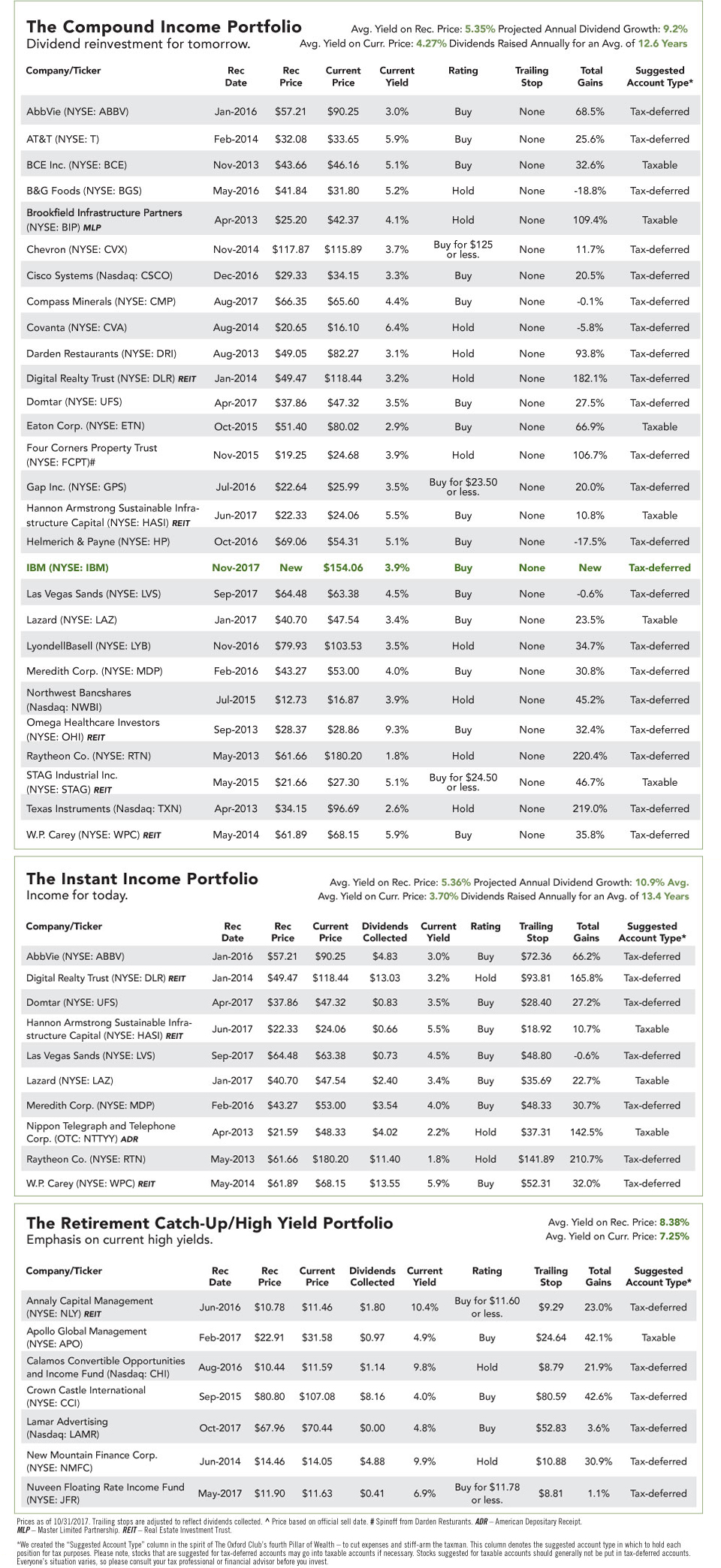

The Dividend

IBM pays a $6 annual dividend. That comes out to a 3.9% annual yield. Through the first nine months of the year, IBM’s free cash flow was $8.7 billion while it paid out half of that in dividends.

The company has raised its dividend for 22 straight years by an average of more than 10% for three-, five- and 10-year periods.

And if President Trump’s proposed tax holiday for companies with overseas profits becomes law, there could be a windfall of dividends for IBM shareholders. The company holds more than $71 billion in cash overseas.

The last time there was a tax holiday, in 2004, IBM repatriated $9.5 billion. If IBM were to do the same this time, it would equal $10.10 per share in cash. That could be spent on share buybacks, a special dividend... or both. I’d expect IBM to bring home more cash than it did in 2004, should the tax holiday take place.

Of course, the late-to-the-party Wall Street analysts don’t like IBM. Twenty out of 27 rate it a “Hold” or “Sell,” reinforcing the idea that this is a contrarian play.

You won’t get rich overnight holding IBM. The blockchain is in its infancy. But you’re going to reap a lot of dividends and profits as it grows up.

IBM is the best way to play the blockchain and even cryptocurrency if you don’t want to take on a lot of risk or don’t understand crypto.

That’s the beauty of this play. If cryptocurrencies continue their monster run, blockchain and IBM will be a part of that. If not, the blockchain is so much more than cryptocurrency. It’s going to change the way the world does business.

And IBM is the leader in this technology.

It fits perfectly with the 10-11-12 System and is a terrific addition to the Compound Income Portfolio.

But no, Dad, I still haven’t sent them my resume.

Action to Take: Buy IBM (NYSE: IBM) at the market, and add it to the Compound Income Portfolio.