Creating income for today, wealth for tomorrow | Issue 49, April 2017

Double-Digit Dividend Growth From an Unlikely (and Uncomfortable) Source

Dear Member,

I’ve always been picky about certain things.

When I was single, I went out on a lot of dates. But I wanted more than a pretty face. I wanted someone smart, fun and ambitious, who didn’t take themselves too seriously.

Then I met my wife, and the search was over.

Slight problem though. She had a boyfriend. But I knew she was the one, so I waited. Luckily, I only had to wait six months.

Twenty-two years and two kids later, I can safely say it was worth the wait.

When I’m picking stocks, it’s often a similar process. I know what I’m looking for, but sometimes I have to wait.

I want yield, dividend growth and an inexpensive valuation. I look for companies that are underfollowed or hated by Wall Street but moving in the right direction.

That’s where Domtar (NYSE: UFS) comes in. And by waiting a few months from when I first discovered it, we can get in at a 25% lower price.

The Fort Mill, South Carolina-based company makes paper products such as those used in religious books, textbooks and envelopes.

As you can imagine, with the world going digital, a papermaker isn’t the most popular idea on Wall Street.

But what everyone’s missing is Domtar’s blossoming personal care line.

Domtar makes fibers for diapers.

It makes and sells its own lines of diapers and, for babies, has the Fisher-Price brand, which it licenses from Compound Income Portfolio member Mattel (Nasdaq: MAT).

It also makes the fibers used in SleepWell and Fitti diapers, as well as other private label brands. But the big growth opportunity is in adult diapers. Seriously.

Between 2015 and 2021, adult diaper sales are expected to soar 57% in the U.S.

Within a decade, adult diapers will outsell infant diapers. In Japan, that’s expected to happen as early as 2020.

According to the Urology Care Foundation, one in three adults has bladder control issues.

Domtar is doubling down on adult diapers. Last October, it acquired Home Delivery Incontinent Supplies Co. (HDIS) for $45 million.

HDIS has annual revenue of about $65 million.

It’s the largest direct-to-consumer provider of incontinence supplies. And it’s been in business for 30 years.

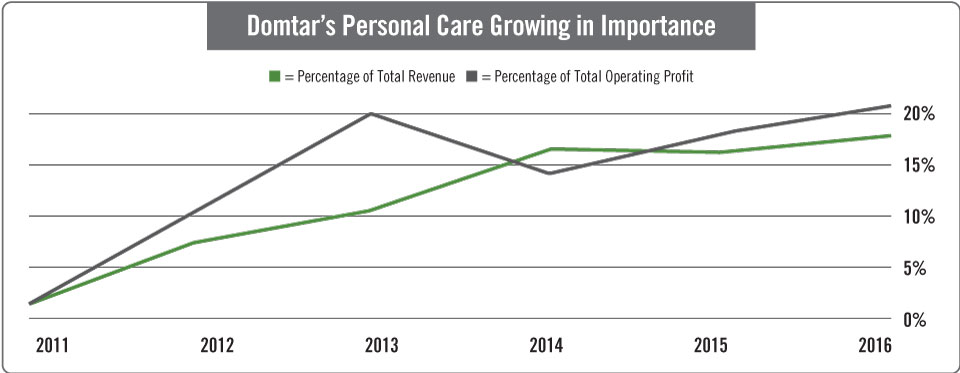

Domtar’s “personal care” segment (what it calls its diaper business) has become an increasingly meaningful part of its overall sales and profitability.

You can see from the chart below that in just five years, personal care has become an important part of Domtar’s revenue and profits.

And those percentages should increase over the coming years.

Diapers Stuffed With Cash

Domtar generates a lot of cash flow. In 2016, cash flow from operations was $465 million. It paid out $102 million in dividends.

However, capital expenditures were sky-high at $347 million, which means free cash flow (cash flow from operations minus capital expenditures) was just $118 million.

Normally, that would concern me. I like to see dividends paid make up only 75% of free cash flow (also called the “payout ratio”). Last year, the payout ratio was 86%.

However, 2016 was not a normal year. The company shut down the largest paper machine in the U.S. and converted an entire facility in Ashdown, Arkansas, from making paper to making fluff pulp, used in diapers.

The conversion is done. That not only will lower capital expenditures but should increase revenue – all of which will add to free cash flow.

Management said capital expenditures should decline to between $210 million and $230 million, a drop of between 34% and 39% from last year’s total.

As a result, in 2017, analysts forecast Domtar’s free cash flow will more than double to $293 million.

The company has raised its dividend every year since 2011. And during those six years, the dividend’s compound annual growth rate was a whopping 22%.

If we assume that the growth rate will be just 10% going forward, the payout ratio will be a low 38% next year.

So it’s quite possible that there will be massive dividend growth in the future if cash flow continues to improve.

The stock currently pays a 4.4% yield, though I expect double-digit annual growth over the next decade.

Additionally, the stock is what the kids might call “crazy cheap.”

It trades at just 12 times forward earnings, 0.5 times sales and – incredibly – below book value at just 0.89. In other words, if the company were liquidated today, you’d be buying the stock for just $0.89 on the dollar.

Unsurprisingly, analysts who wait until stocks are performing well before they recommend them hate Domtar. Nine out of 14 analysts rate the stock a “Hold” or “Sell.”

Domtar reminds me of another company in our Compound Income Portfolio – Meredith Corp. (NYSE: MDP). We first bought the magazine publisher in 2013 when Wall Street didn’t understand that Meredith owned some of the most-visited (by women) sites on the web.

The stock was cheap and had a great dividend that it raised every year.

We made 40% on the stock when it received a buyout offer. A year ago, after the deal fell through and the stock dropped, we bought it again. We’re up 53% since February 2016.

Domtar has many of the same characteristics, and I expect it to do just as well.

A company whose stock is trading below book value, with a solid yield and growing cash flow, and that is a big player in a booming market is worth the wait.

Buy it now before the rest of Wall Street discovers the growth story no one else is talking about yet. You’ll be getting in before the adult diaper trend becomes mainstream news.

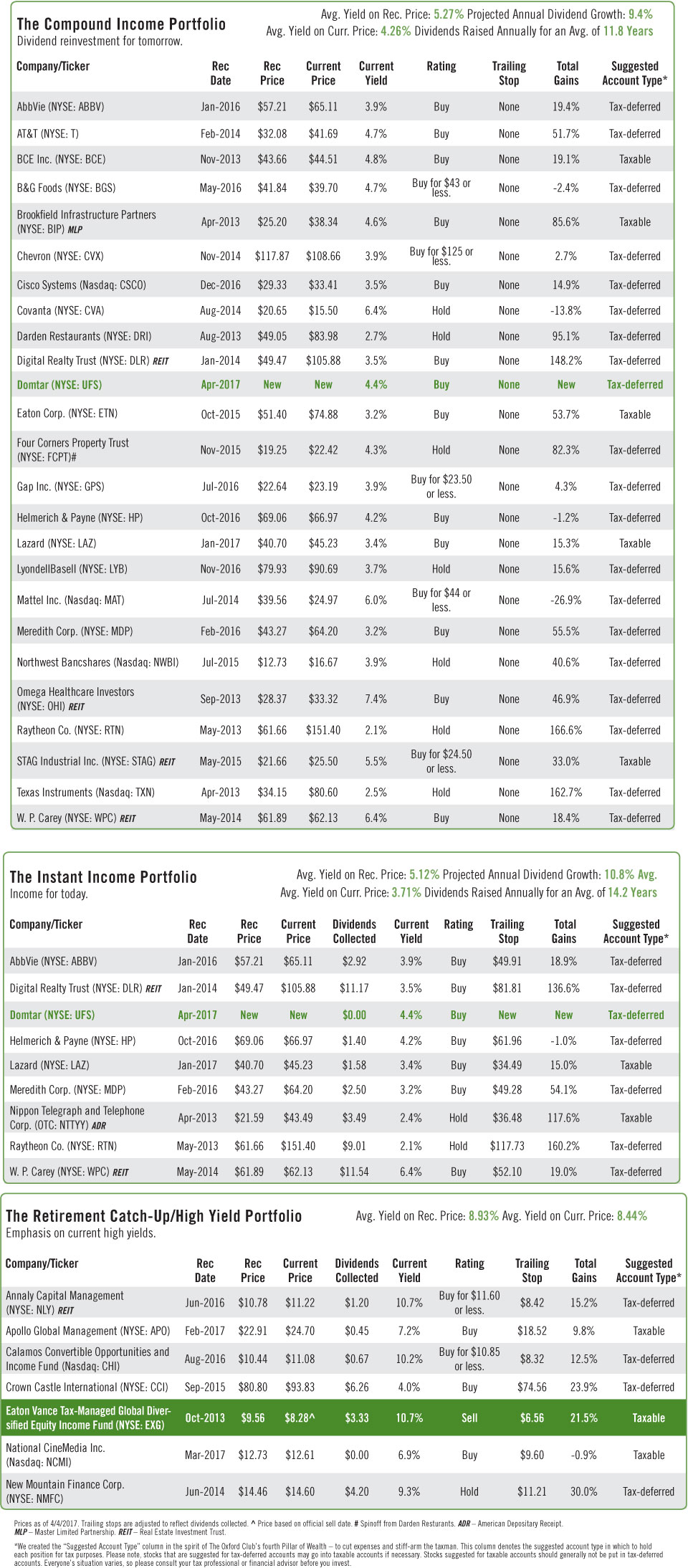

Action to Take: Buy Domtar (NYSE: UFS) at the market, and add it to the Instant Income Portfolio and Compound Income Portfolio. Place a trailing stop 25% below your entry point in the Instant Income Portfolio.

A Private Wealth Seminar You'll Never Forget

Chief Investment Strategist Alex Green, Chief Income Strategist Marc Lichtenfeld, Bond Strategist Steve McDonald, and Energy and Infrastructure Strategist Dave Fessler

Chief Investment Strategist Alex Green, Chief Income Strategist Marc Lichtenfeld, Bond Strategist Steve McDonald, and Energy and Infrastructure Strategist Dave Fessler

An unforgettable two-day getaway melding adventure and top-notch investment education in the heart of New Mexico... You’ll wine, dine and meet with the Club’s top advisors during this intimate investment retreat, and discuss what the next four years under Trump’s presidency will mean for your portfolio.

An unforgettable two-day getaway melding adventure and top-notch investment education in the heart of New Mexico... You’ll wine, dine and meet with the Club’s top advisors during this intimate investment retreat, and discuss what the next four years under Trump’s presidency will mean for your portfolio.

September 25-26, 2017

September 25-26, 2017

The Four Seasons Resort Rancho Encantado, nestled in Santa Fe’s Rio Grande River Valley, overlooking the peaks of the Jemez Mountains

The Four Seasons Resort Rancho Encantado, nestled in Santa Fe’s Rio Grande River Valley, overlooking the peaks of the Jemez Mountains

Please join us! To book and to receive a $300 discount on registration, email Kiara Laughran at voyager@oxfordclub.com.

STEVE’S BOND INSIGHTS

Why It Pays to Focus on More Than Just Yield

In my 34 years in the markets, I’ve always been amazed at how the bond and stock markets seem to have the magical ability to take in all the predictions of analysts and experts and then do the exact opposite.

Experts’ predictions about the death of the bond market have been a recurring theme for almost 10 years.

And year after year, those of us on the bond side of the house have had to suffer through calls for sell-offs and bond market disasters that never materialized.

If you play bonds correctly, those will never happen. But that’s a topic for another time...

Recently, the more the so-called “experts” called for a disaster in bonds, the more the market threw it back in their faces.

And, I have to admit, it’s been entertaining to watch.

If the stock market’s activity (since the November presidential election) is any indication, its ability to outsmart the pros is exploding on the equity side of the house, too.

Before the election, virtually every expert in the world – financial and otherwise – didn’t think or wonder but knew “for a fact” that the stock market would crumble in the unlikely event of a Trump victory.

They were wrong on both counts!

And since the election, the number of experts calling for the collapse of the Trump rally has been growing daily.

In my experience, that means we’re nowhere near a top.

But the most convincing evidence of the market’s ability to prove the herd wrong emerged after the Fed increased rates in its March meeting...

Despite weeks of the mainstream financial media calling for another sell-off in bonds and despite the Fed’s rate hike, bond prices actually went up and Treasury yields moved down.

Eventually, though, rising interest rates will cause a drop in the bond market.

And finally, after years of incorrectly predicting a sell-off, the anti-bond experts will be right! Or, at least, sort of...

A Short-Lived Rout

The news behind the news is that consumer confidence is taking off. There are increasing indications of moderately higher inflation, rising to the 2.5% area. And the tax reform and infrastructure spending Trump’s promising is seen as a big growth booster.

If consumer confidence, growth and inflation are showing signs of improvement – and they are – rising bonds yields are not far behind.

If we are to avoid the losses in the bond portion of our income portfolios, it’s time to shift gears. Here’s what you need to do now...

If you’re sitting on gains in any kind of bond fund, cash out now! I’ve written endlessly in my Wealthy Retirement columns about why bond funds will be crushed when the rate shift finally happens.

In today’s environment, if you’re sitting on cash – but want the safety, predictability and reliability that bonds offer – but you’re concerned about an eventual sell-off (which is reasonable), you have to focus on more than just yield.

Keep Your Eye on Duration

Going forward, the name of the game is duration. Duration, unlike other bond concepts, is based on common sense and is actually easy to understand.

It’s a measure of how much a bond’s price will fall when interest rates move up. It’s based on the credit quality of a bond, the number of calls it has and its interest rate.The higher the quality of a bond, the less its price will fall when rates increase.

This makes a lot of sense if you think of it in terms of which bonds you would hold if the market went against you. Investment-grade bonds (rated BBB and higher) have the lowest chances of defaulting.

So most folks hold their higher-rated bonds no matter what the market does.

Your Best Option

The idea here is simple: the less time your money is exposed to the market, the less chance you have of a loss. And the more opportunities you have to reinvest your money in a rising rate market, the greater your average return. Very simple!

Remember, duration (although it’s expressed as a number of years) is not the same thing as maturity. They are two very different things.

A bond with a duration of one year will fall about one point, or $10 in price, with each one-point increase in interest rates. Very bearable.

But duration can be as high as 10 or 15. And 10% to 15% would be a big drop in a bond price for a 1% increase in rates. Plus, that kind of volatility can drive panic-selling, which accounts for almost all bond losses.

Coupon

The higher a bond’s coupon (or annual interest rate), the less likely it is that you’ll sell into a falling market. And panic-selling into a correction is the root of almost all bond losses.

If you’re holding a bond with a 10% coupon versus one with a 3% coupon, common sense says you’re a lot less likely to sell the 10% bond. It pays too much to dump.

Calls

Calls are preplanned opportunities for a company (or municipality) to buy back a bond before maturity at a preset price... usually well above par, $1,000 per bond. As such, the duration of a corporate or municipal bond with multiple calls would be lower than that of a Treasury, which has no calls.

When rates finally move up and bond prices drop, you’ll be very happy if you hold only low-duration bonds. Drops of 5% to 8% are much more bearable than drops of 10%, 15% or more.

Our Blue Chip Bond Portfolio has an average duration of 7.6.

And a 7.6% drop in value is more than tolerable for everyone except the most risk-averse.

If the Fed continues to raise rates at one-quarter of a percent at a time, a 1% increase will take a full year.

In the meantime, keep in mind that bonds with high durations and long maturities are just one element of your income portfolio. If rates don’t rise as much or as quickly as expected (which many believe could happen), these bonds will be fine.

My advice? Turn off the TV, and focus on duration. It’ll limit your downside and help keep you in your bonds... which is where you make money.