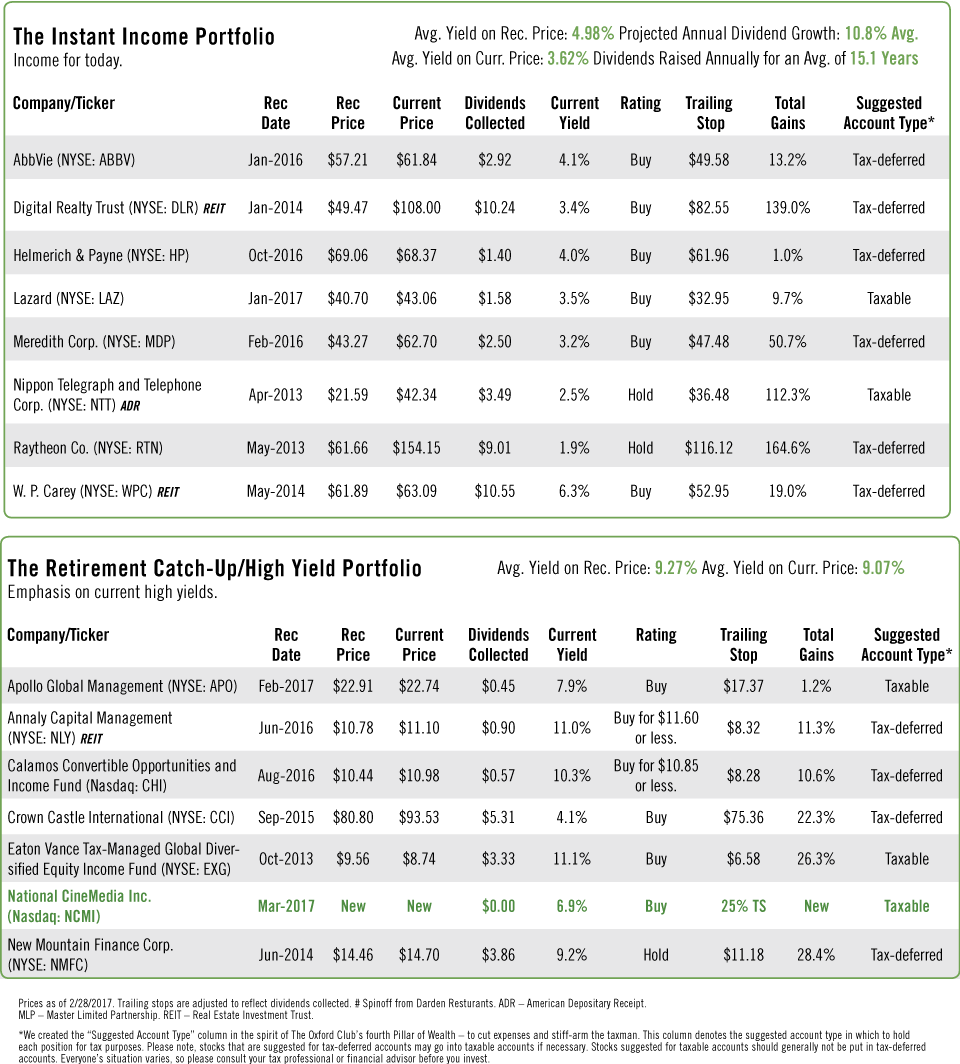

Creating income for today, wealth for tomorrow | Issue 48, March 2017

Lights, Camera, Cash In

Earn a 6.9% Yield From This Millennial Marketing Machine

Dear Member,

My brother loves movies.

He’s written books about movies, worked in the industry for more than two decades and taught college film classes. He’s also one of the most quoted authorities on action movies.

The topic of his undergrad thesis was Die Hard. Really.

Many Americans share his love of movies – though perhaps not quite as obsessively. In fact, 1.3 billion movie tickets were sold in the U.S. last year.

And with potential blockbusters like The Lego Batman Movie, Pirates of the Caribbean: Dead Men Tell No Tales, Cars 3, Despicable Me 3, Spider-Man: Homecoming and Star Wars: The Last Jedi coming out this year, it should be a very strong year for movie ticket sales.

I’ve found a unique way to earn a 6.9% yield on all those movie ticket sales... one that doesn’t involve popping popcorn that will make you reek of fake butter (like the job my brother had in high school).

If you’ve been to the movies in the past few years, no doubt you’ve seen National CineMedia Inc. (Nasdaq: NCMI) at work.

The company manages National CineMedia, which provides the trivia, quizzes, entertainment and, importantly, advertisements that are on screen while you’re tearing into your Milk Duds waiting for the previews to start.

Captive Audience

National CineMedia currently provides content to more than 20,500 screens in 48 states plus the District of Columbia.

Because it shows fun content and entertaining ads to moviegoers, its levels of brand recall and likeability are nearly 10 percentage points higher than those garnered by TV ads, according to Nielsen Brand Effect (IAG) data.

Advertisers are increasingly turning to movie theaters because they know TV viewers fast-forward through

the ads.

In fact, 55% of TV viewership occurs “on demand,” on a DVR or via streaming. That number rises to 72% for millennials – a vital demographic for ad buyers.

Consider:

- Millennials make up 48% of National CineMedia’s audience versus just 11.2% for prime time network or local TV, and 20.5% for prime time cable.

- Millennials’ movie attendance grew 16% in 2015.

- Millennials make up 29% of box office sales.

So National CineMedia has a captive and engaged audience that advertisers not only want to talk to, but have a hard time reaching through more traditional methods.

Joint Venture

National CineMedia has an unusual structure. It’s majority-owned by a joint venture between three theater companies: AMC (NYSE: AMC), Regal (NYSE: RGC) and Cinemark (NYSE: CNK).

Regular shareholders (via National CineMedia Inc.) own 43.7% of the company.

But that’s about to change. AMC is buying Carmike Cinemas. And in order to complete the acquisition, the Department of Justice has ruled that AMC must divest theaters in 15 markets and sell its 17.4% stake in National CineMedia.

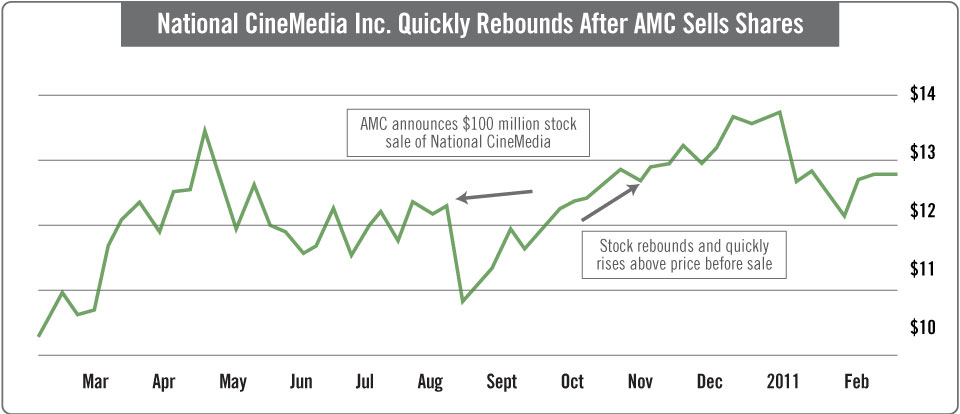

But this won’t be the first time AMC has sold shares of National CineMedia.

In August 2010, AMC announced plans to sell $100 million worth of the stock. National CineMedia Inc.’s share price declined temporarily, but as you can see from the chart below, the sale didn’t keep the price down for long.

The company won’t be selling everything at once. It’s required to bring its equity stake down to 15% by December 20, 2017, 7.5% by December 20, 2018, and 5% by June 20, 2019.

When AMC sold the stock last time, it didn’t just dump its shares on the market. They were sold through an investment banker.

That will very likely be the case again. This will be a very orderly sale.

There could be a short-term ceiling on the stock, which would allow us to buy more shares cheaply or reinvest the dividend at low prices. But over the long run, it shouldn’t matter. In fact, it’ll give public shareholders the majority stake in the company, which is a good thing.

Financial Performance

Through the first nine months of 2016, National CineMedia Inc.’s free cash flow grew to $98 million from $54 million.

During that time, it paid out about $41 million in dividends, giving it plenty of room to continue paying its current dividend or raise it if cash flow grows.

In 2017, earnings are projected to grow 21%. Assuming that cash flow follows earnings, I wouldn’t be shocked to see a dividend increase, particularly to attract investors who may be concerned about AMC’s sale of stock.

National CineMedia Inc. has paid a $0.22 quarterly dividend since 2011. It’s raised its dividend four times since it began paying one in 2007.

The dividend has never been cut.

In addition to the company’s solid financials, I like its business model. It’s not capital intensive. And it doesn’t need to invest in a lot of infrastructure and expensive technology. So any revenue growth should increase earnings and cash flow immediately.

This is a stock that may require some patience. As I mentioned, there are a lot of shares coming up for sale over the next two years.

But for investors with a long-term time horizon (like Oxford Income Letter subscribers, since we’re not a short-term trading service), you’ll collect a juicy 6.9% yield while owning a growing business... One that’s helping advertisers reach an elusive audience they wouldn’t otherwise have access to.

The next time you go to the movies, enjoy the content before the previews start, knowing that it’s putting money directly in your pocket.

Action to Take: Buy National CineMedia Inc. (Nasdaq: NCMI) at the market, and add it to the Retirement Catch-Up/High Yield Portfolio. Place a 25% trailing stop below your entry point.

Note: National Cinemedia’s dividend is a return of capital, which means you will not pay tax on the dividend in the years the dividend is received. Instead, your cost basis will be lowered by the amount of the dividend.

Private Wealth Seminars 2017

Grand Hotel • Mackinac Island • July 17-18

Four Seasons Resort Rancho Encantado • Santa Fe • September 25-26

Please join us as our experts reveal the sectors that stand to benefit the most under President Trump and give details on the companies they expect to skyrocket in 2017.

You’ll hear from many of your favorite editors, including Chief Income Strategist Marc Lichtenfeld and Chief Investment Strategist Alex Green. And you’ll have the opportunity to mingle with them at an exclusive reception.

But hurry! These events are strictly limited to just 100 attendees...

And Mackinac Island is nearly sold out. To save $300 on your registration, go here now.

STEVE’S BOND INSIGHTS

Profit From the Bank Everyone Loves to Hate

Every once in a while, I come across a bond so good, with so many positives, it seems almost too obvious to recommend.

This month’s pick is one of those.

Goldman Sachs (NYSE: GS).

The Goldman Sachs Group Inc. is a global investment banking, securities and investment management company.

It generates its revenues from four operations groups: Investment Banking (21% of net revenues), Investment Management (19% of net revenues), Institutional Client Services (47% of net revenues), and Investing and Lending (13% of net revenues).

Since the 2008 debacle, this has been the company everyone loves to hate.

I lost count of how many regulators and congressional committees made their reputations by grilling and penalizing it.

But, as has always been the case, Goldman hit every pitch thrown at it out of the park.

And the recent spurt of optimism about the economy and markets will drive profits in all four of its operations groups.

Shortly after last fall’s election, the company’s investment banking group was up 18.9% year to date compared to the S&P’s 6.7% increase for the same period.

Since the election (and thanks to the expectation of fewer banking regulations), its stock has run up more than 35%.

The market appears certain big things are in the company’s future.

The Trump administration’s promises of deregulation and the potential easing of antitrust policies are also expected to drive mergers and acquisitions activity, which is a key revenue source for the investment banking group.

Goldman also expects the current flight to risk from bonds to stocks (driven by renewed confidence in the economy and expected infrastructure spending) to improve capital markets, a key driver of its investment banking and trading revenues.

The improving stock market is expected to drive a rebound in its equity underwriting revenues – IPOs – as early as the fourth quarter of 2017.

Goldman’s trading and investment management fees will benefit as well from increasing confidence in stocks.

And the company is in the right place at the right time to expand its international footprint.

Several European banks are in the process of reducing their investment banking activities, which has opened the door for a significant increase in market share in that area.

The company’s short-term fundamentals are impressive as well.

Between this year and next, Goldman expects to increase earnings from $19.90 per share to $21.80, or to a high estimate of $25.20 per share, which would be a 26% increase.

Revenues are expected to increase by 4.1% during the same period. The company’s five-year growth estimate is 12.68% per year.

For a $100 billion company, 12% growth per year is phenomenal.

Goldman currently has $380 billion in debt and $728 billion in cash. That kind of cash-to-debt ratio is unheard of in any sector or industry.

And despite the pounding every bank took in 2008, it’s retained a BBB+ rating from Standard & Poor’s.

And if the Trump-driven tailwinds and near-term estimates aren’t enough, the bond I’m recommending this month also has a “death put.”

A death put is an estate planning tool that guarantees your heirs will never receive less than par, or $1,000, for the bond.

No matter how low the price of this bond may drop, your heirs can put the bond to Goldman for $1,000.

And I’m sure you have a pretty good idea of how many people in this world would love to “put it to”

Goldman Sachs!

Before we get to the recommendation, the maturity of this bond requires a little explanation.

It matures on March 15, 2034. That’s a 17-year maturity, which is longer than the maturities of most bonds I recommend.

But the combination of the excellent short- and long-term prospects, a BBB+ rating, and the market price security the death put offers more than makes up for the extra holding time.

Plus, as deregulation drives both revenues and earnings higher, I expect the bond’s rating to be bumped up a notch or two to the A to A+ area.

And as the bond’s market price follows its improving fundamentals, I expect to be able to take a capital gain before maturity.

At 109.5, or a $1,095 price, this bond’s yield to maturity is 4.5%. This assumes the premium of $95 per bond.

I would prefer if it were priced at par or – better yet – at a discount. But for a bond of this quality, with Goldman’s prospects, in today’s market, 109.5 is a bargain.

This bond offers an enormous amount of secure income and reliability, and it’s the perfect addition to our Blue Chip Bond Portfolio.

Action to Take: Buy the Goldman Sachs 5.5% bond (CUSIP 38141ey45) that matures on March 15, 2034, for 109.5, or $1,095 per bond, and add it to the Blue Chip Bond Portfolio.

The Only Thing You Should Look for in a Stock Chart Today

If you can see 2 lines crossing each other, you can follow this moneymaking pattern over and over.

With these 3 stocks, you could capture $54,000, and it would only take you around 100 days.