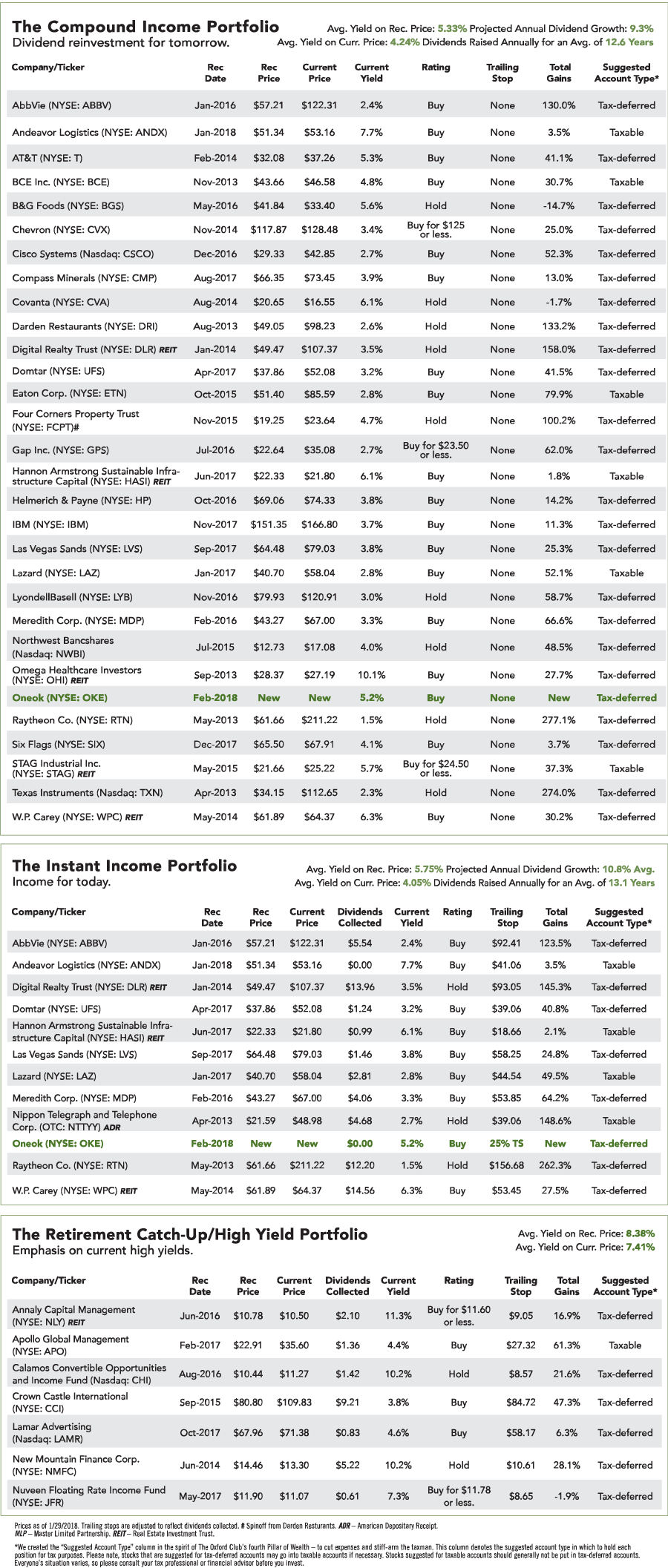

Creating income for today, wealth for tomorrow | Issue 59, February 2018

A Turnaround in the Energy Sector With a 5.2% and Growing Yield

Dear Member,

I love a good turnaround story.

The Golden State Warriors were mediocre, at best, for decades until their recent dominance of the NBA.

John Travolta, one of the biggest movie stars of the 1970s, was all but forgotten in the 1980s. Then, his role in Pulp Fiction brought his career back from the dead.

Heck, even Tonya Harding, who famously orchestrated the kneecapping of a figure skating rival, is now seen as a somewhat sympathetic character.

And our portfolio is filled with turnaround stories – Gap (NYSE: GPS), Chevron (NYSE: CVX), IBM (NYSE: IBM) and several others.

Today I have another for you, and it’s in a space that I’m particularly bullish on for 2018.

In the January issue of The Oxford Income Letter, I mentioned that I liked the energy sector – including master limited partnerships, or MLPs.

This month, I’m sticking with the business model of most MLPs – pipelines – but not the corporate structure.

Pipeline companies generate tons of cash as they don’t have large operating expenses. This particular pipeline company pays a 5.2% dividend yield that is rising by double digits each year.

But this company is a bit different from our other energy plays, such as Chevron. It doesn’t focus on oil. Its main business is transporting natural gas.

Demand for natural gas is huge thanks to this winter’s brutally cold temperatures. It’s in the 40s here in South Florida as I write this. I know I may not get much sympathy from those of you in the north, but I had to put on a jacket this morning.

Power plants have never burned as much natural gas as they do today. In fact, this winter we’re using 14% more gas than we did during the polar vortex of 2014.

And it’s not just the frigid Northeast and Midwest (and South Florida) that need gas.

Over the past five years, U.S. producers have more than doubled the amount of natural gas they export.

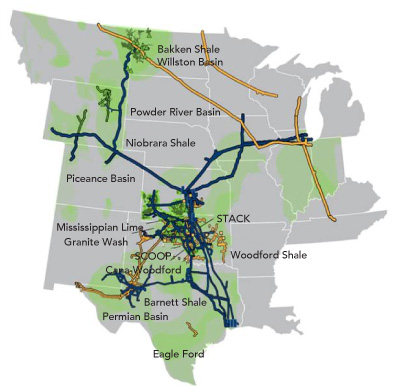

Oneok (NYSE: OKE) is positioned perfectly to take advantage of the growing demand for natural gas.

The 112-year-old company gathers, stores and transports natural gas liquids. It has 38,000 miles of pipelines in the United States and can store 58 billion cubic feet of natural gas.

Its assets are located in some of the country’s most active gas fields, including the Permian Basin.

Additionally, Oneok dominates the Bakken region, with two-thirds of gas rigs on Oneok’s footprint.

And in the states where Oneok operates, rig counts are up 70% in the past year. All that gas will need to be gathered, transported along pipelines and stored.

Oneok is in a perfect position for massive growth.

The company has invested heavily for the future, and it is starting to pay off.

In the third quarter of 2018, Oneok will complete a 120-mile pipeline expansion in West Texas.

Two more pipeline expansions will come online in Oklahoma in the fourth quarter. And a massive 900-mile pipeline from Montana to Colorado will be finished at the end of next year.

These and other projects should fuel growth in the near future as well as the long term.

A Game Changer

What I like about the pipeline business is that it’s not tied to the price of the commodity. If a gas company needs to get gas from point A to point B, it pays a set fee to the owner of the pipeline regardless of the price of gas.

Those fees are usually set months or even years earlier, so a fluctuation in the price of gas doesn’t change the fees collected by the pipeline.

Five years ago, 63% of Oneok’s revenue was fee-based. Today, 90% is.

Last year, the company took an important step in improving its financials. It absorbed its MLP, Oneok Partners.

Here’s why that’s a big deal:

- The acquisition of Oneok Partners immediately adds to earnings and free cash flow.

- It will result in Oneok owing no taxes through at least 2021.

- Oneok will have a lower cost of capital, making it cheaper to make future investments.

In fact, this year free cash flow is forecast to be more than double what it was in 2016, and it should jump another 22% in 2019.

Additionally, the company is paying down debt. It repaid $1 billion in July. Oneok plans to bring its debt-to-EBITDA ratio (a simple measure of cash flow) below 4.0. It was 4.6 at the end of the third quarter and 5.1 in 2016.

Impressive Dividend

Oneok has paid a dividend since 1972. It has raised the dividend every year since 2003. That includes the Great Recession from 2008 to 2009 and the collapse in energy prices from 2015 to 2016.

The dividend’s compound annual growth rate over that time has been an impressive 10.6%. The current quarterly dividend is up 25% year over year.

The company generates plenty of cash flow to pay the dividend. Through the first nine months of 2017, Oneok’s free cash flow totaled $1.02 billion. It paid out $747 million in dividends. And with free cash flow expected to rise to $1.9 billion next year, the dividend should increase sharply over the coming years.

There are many ways to invest in a rebound in natural gas, but Oneok is one of the only pure plays. With a yield of 5.2% and double-digit dividend growth expected, this stock fits perfectly into the 10-11-12 System.

Action to Take: Buy Oneok (NYSE: OKE) at the market, and add it to the Instant Income Portfolio and Compound Income Portfolio. Place a 25% trailing stop if you’re holding it in the Instant Income Portfolio (collecting the dividend income). Do not place the stop if you’re holding it in the Compound Income Portfolio (reinvesting the dividend). The stock should be held in a tax-deferred account if possible.

Marc’s New Best-Seller...

You Don’t Have to Drive an Uber in Retirement

Planning for retirement does not mean holding off on fun today; there are many simple ways the average American can boost their income and reduce everyday costs without living like a pauper or clipping coupons. Marc’s new book, You Don’t Have to Drive an Uber in Retirement, will help you take stock of what you have and what you’ll need, and will show you how to bridge the gap.

- Discover unique ways of generating a meaningful amount of income – without having to get a job.

- Adopt new everyday strategies that will help you increase your funds.

- Maximize your savings while minimizing the impact on your lifestyle.

- Learn just how much you’ll need for a comfortable retirement.

Add new income streams, optimize your portfolio and learn to spend less without living less – these are the factors key to making your golden years truly golden. You Don’t Have to Drive an Uber in Retirement is an important resource and insightful guide for those who want to maintain their comfortable lifestyle in retirement – without getting a job.

Pre-order your copy today, and receive a free bonus chapter: “How to Save Money Every Time You Visit the Doctor.” For all the details, click here.