Creating income for today, wealth for tomorrow | Issue 58, January 2018

Annual Forecast Issue

The Prediction So Nice I’m Making It Twice

And a Company That Could Quadruple Your Money in the Next 10 Years and Pays You While You Wait

Dear Member,

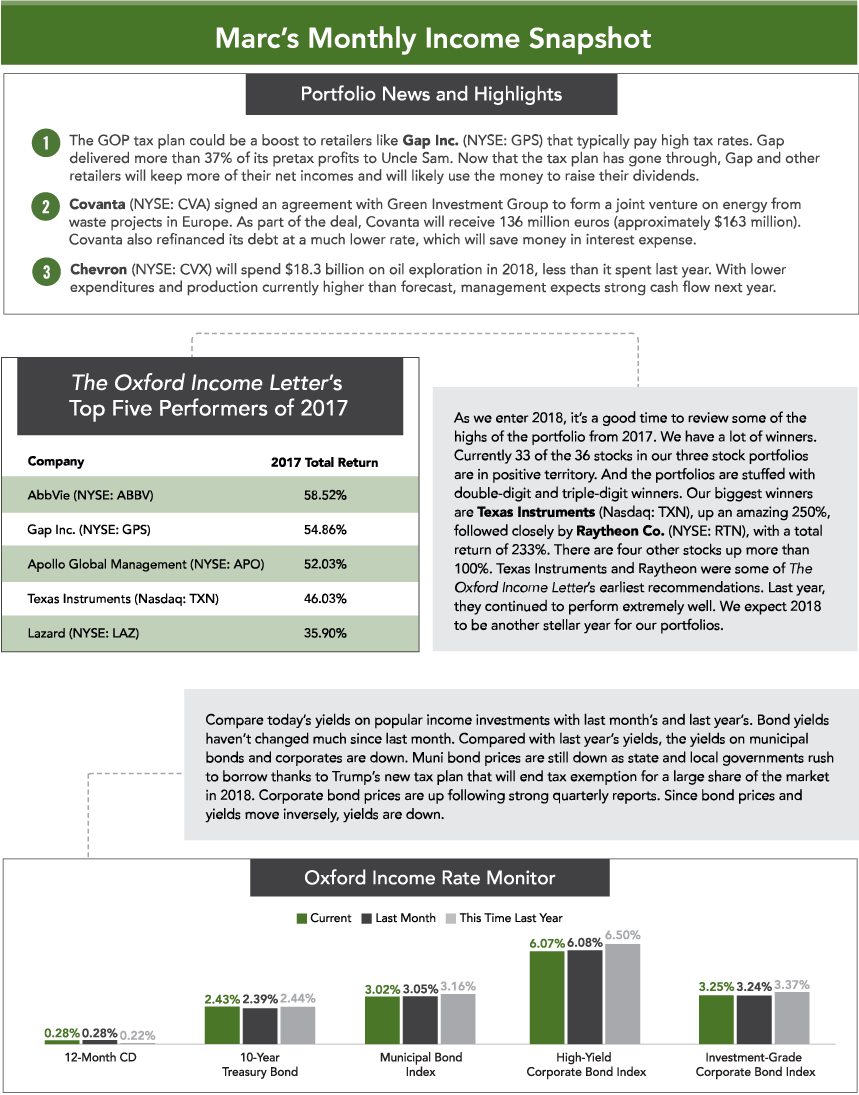

In last January’s prediction issue, I said I liked financials and healthcare for 2017. And the stocks in those sectors in our portfolio have done very well.

In that issue, I recommended investment bank and asset manager Lazard (NYSE: LAZ). Since then, it has returned 38% versus a 22% gain in the S&P 500. Apollo Global Management (NYSE: APO) is up 53% since it was recommended in February. Our lone bank stock, Northwest Bancshares (Nasdaq: NWBI), didn’t fare as well. Though we’re still up 43% on it, it had a slightly negative return in 2017.

Our lone healthcare stock, AbbVie (NYSE: ABBV), had a terrific year, climbing 59%.

In 2018, I once again expect financials and healthcare to outperform. And this year I’m adding another sector to my favorites.

The Yield Curve... and Financials

Financials should continue to perform well. Higher interest rates will generally help banks and other financial institutions as they’ll make more money on the capital they lend.

Additionally, the yield curve is very flat right now. The yield curve is the difference in interest rates between the two- and 10-year Treasurys. A small difference is seen as a flat yield curve. A growing difference is a widening curve.

When the yield curve is flat, it’s tougher for financial institutions to make money. As the economy heats up and interest rates rise, the yield curve should widen, which will be positive for the financial sector.

Additionally, the Trump administration’s removal of costly and burdensome regulations will give banks and other financial companies the flexibility to take on business they may not have been able to in the recent past.

I’ll be looking for new financial companies to add in 2018.

Big Government Won’t Slow Healthcare Down

Despite the tax reform bill recently signed into law, which is expected to cause 13 million more people to be uninsured, the demand for healthcare will continue to be strong.

As of 2015, there were nearly 48 million seniors in the United States, with 10,000 people turning 65 every day.

And we know that the older we get, the more healthcare products and services we consume.

So regardless of government policy, a demographic tidal wave is upon us, and it will continue to increase demand for healthcare for the next several decades.

In 2018, I’ll be looking to add some quality healthcare companies. In fact, as you read this, I’m at the J.P. Morgan Healthcare Conference meeting with CEOs, looking for the next great company in the sector.

My New Favorite Sector for 2018

Those two predictions – that financials and healthcare will outperform – are the same ones I made for 2017. This year I’m adding another group to the list: master limited partnerships (MLPs).

MLPs are pass-through entities that generally avoid federal and state corporate income taxes because they are classified as partnerships. The income is “passed through” to unit holders (MLP investors are called unit holders).

Most MLPs operate in the energy industry. That’s because, to maintain their tax benefits, they have to generate 90% of their income from “qualified activities,” i.e., exploration and development of natural resources.

As a result, if the energy sector does well, so do MLPs. And I expect the energy sector to outperform in 2018 for several reasons:

- The economy is heating up. Third quarter GDP growth in the U.S. was 3.3%, the highest it’s been since 2014. A stronger economy should increase the demand for oil and gas.

- OPEC recently agreed to reduce output. That puts pressure on the supply side of the supply-and-demand equation.

- Saudi Aramco is going public. The largest oil-producing company in the world is expected to IPO this year. You can be sure that the Saudis are going to do everything in their power to make this an extremely lucrative offering to refill their coffers after the oil price collapse of a few years ago. Some believe the recent arrests of senior government officials and royal family members were made to ensure that the IPO would be as big as it could be. Don’t be shocked by more volatility in Saudi Arabia.

So oil should do well... but MLPs should do even better.

When the price of oil crashed in 2015, all types of energy stocks, including MLPs, tanked with it. In theory, MLPs shouldn’t have because they are not dependent on the price of oil.

The majority of MLPs are pipeline companies that get paid contracted fees for allowing oil to flow through their pipelines.

The price of oil has to be at or above a certain level for an exploration company to make money extracting it from the ground. That’s not the case for a pipeline company. It doesn’t matter if oil is at $30 or $100 – those companies’ fees will be the same.

As long as an oil company is transporting its oil through a pipeline, the MLP gets paid.

When oil rebounded, the stocks of oil companies followed. MLPs did not, creating an opportunity.

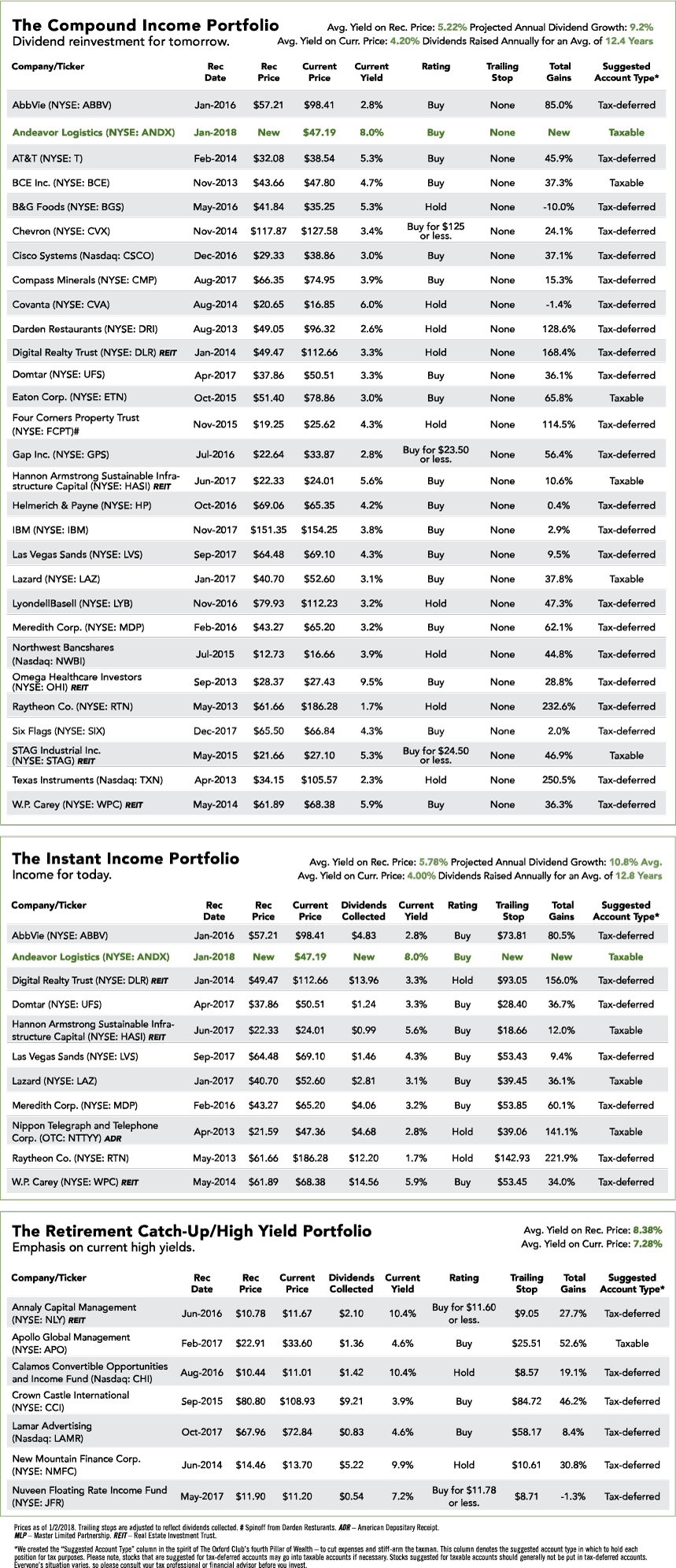

The one I want you to buy today is Andeavor Logistics (NYSE: ANDX).

The company has 5,800 miles of pipeline and 32 terminals, mostly in the western U.S.

Distributable cash flow (DCF) – a measure of cash flow used by MLPs – grew 19% in 2017, but growth should be even stronger in 2018 as the company acquired Western Refining Logistics in October.

At the same time, Andeavor Logistics issued 78 million units to its general partner, Andeavor (NYSE: ANDV), in exchange for eliminating distribution rights. In 2016, Andeavor Logistics paid Andeavor $148 million. It will no longer have to make those payouts.

One of the goals of that deal was to improve Andeavor Logistics’ financials in order to obtain an investment-grade rating from the credit rating agencies. That goal was achieved on October 31, and it should lower the partnership’s borrowing costs.

The Distribution

The stock pays around an 8% yield. Andeavor Logistics has raised the distribution (MLPs pay distributions, not dividends) for 26 straight quarters.

Management expects annual distribution growth of 6% per year with plenty of cash flow to cover it.

If the company can achieve that kind of growth, it should richly reward unit holders. Assuming Andeavor Logistics has an 8% starting yield and 6% distribution growth, and the stock matches the historical average return of the stock market, the investment should more than quadruple over 10 years.

If DCF continues to grow and the stock price mirrors that growth, the returns could be even higher.

Action to Take: Buy Andeavor Logistics (NYSE: ANDX) at the market, and add it to the Compound Income Portfolio and Instant Income Portfolio. Because this is an MLP, some or all of the distribution will be tax-deferred, so I recommend holding the stock in your taxable account.

The Oxford Club’s 2018 Private Wealth Seminar

Fairmont Chateau Whistler, British Columbia, Canada | July 23-24

You’re cordially invited to join us at our 2018 Private Wealth Seminar next July 23-24 at the beautiful Fairmont Chateau Whistler in British Columbia, Canada.

This is a wonderful opportunity for you to get up close to some of the world’s most accomplished investing minds... discover their best ideas for generating serious money in uncertain markets... and mingle with other like-minded Members, forging profitable, lifelong friendships.

You’ll hear from your favorite Oxford Club editors, including Chief Investment Strategist Alexander Green, Chief Income Strategist Marc Lichtenfeld, Bond Strategist Steve McDonald and our guest speaker, Sprott U.S. Holdings Chairman Rick Rule.

We’ve spent months preparing this exclusive event for you. And while we’re still putting together some of the final touches, we don’t want to keep you waiting. Registration for our July meeting is now open. Simply click here for more information.

P.S. Our second Private Wealth Seminar will be held October 1-2, 2018, at the Sanctuary Resort on Kiawah Island, South Carolina. If you’d like to join us at this meeting, please email conferences@oxfordclub.com to be added to our interest list. You’ll be the first to know when registration becomes available.