Swaps can be viewed as combinations of forward contracts

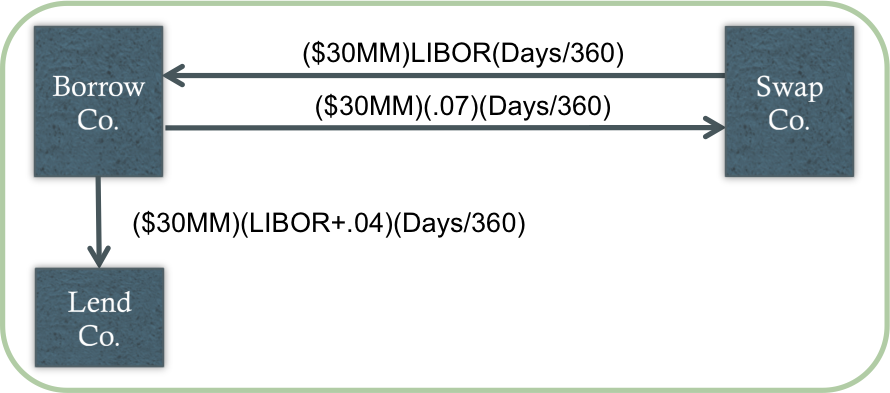

Converting Floating and Fixed Rates

Net effect: BorrowCo pay 7% + 4% = 11% fixed

Adjusting Duration with Swaps

Negative duration (pay fixed to receive floating)

Terms (maturity/payment frequency)

Notional principal: NP = B[(MDURT-MDURB)/MDURS]

For example, to adjust the duration of a $100MM portfolio from 6.00 to 3.75 using a swap with MDUR of -.50, the NP will be: $100MM(3.75-6.00)/-.50 = $450MM

Structured Notes

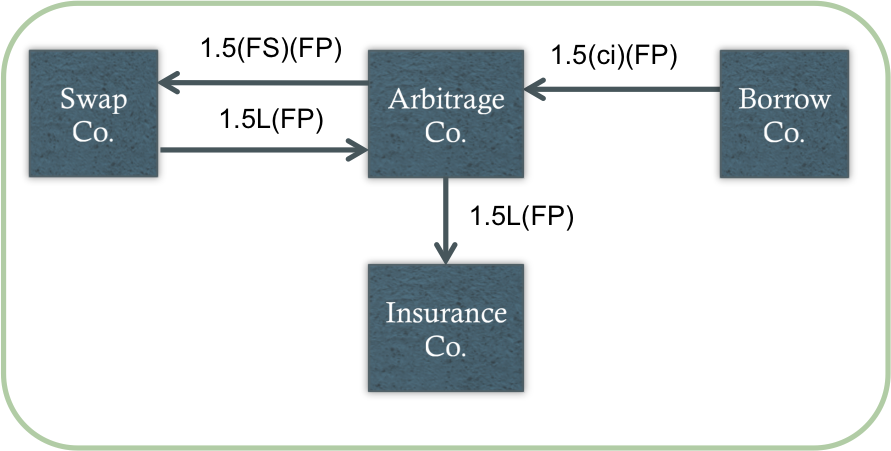

Leveraged floater

Net effect: ArbitrageCo earns 1.5(ci-FS)(FP) fixed

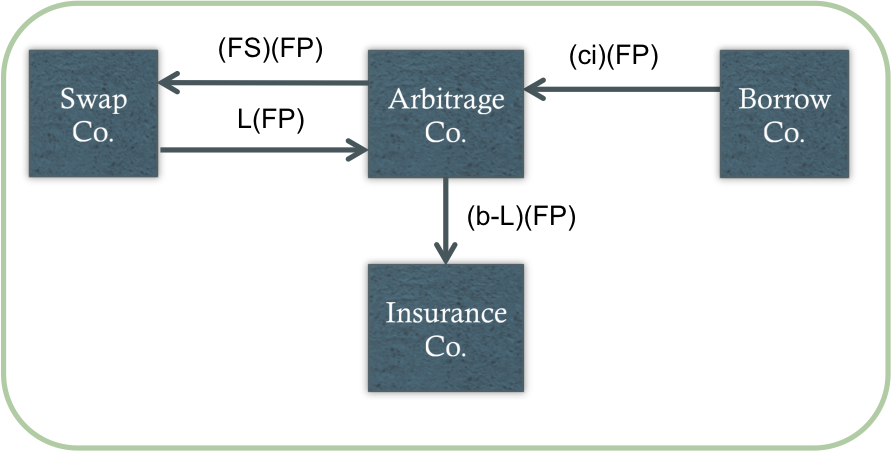

Structured Notes (cont'd)

Inverse floater

Net effect: ArbitrageCo earns FP(FS+ci-b) fixed

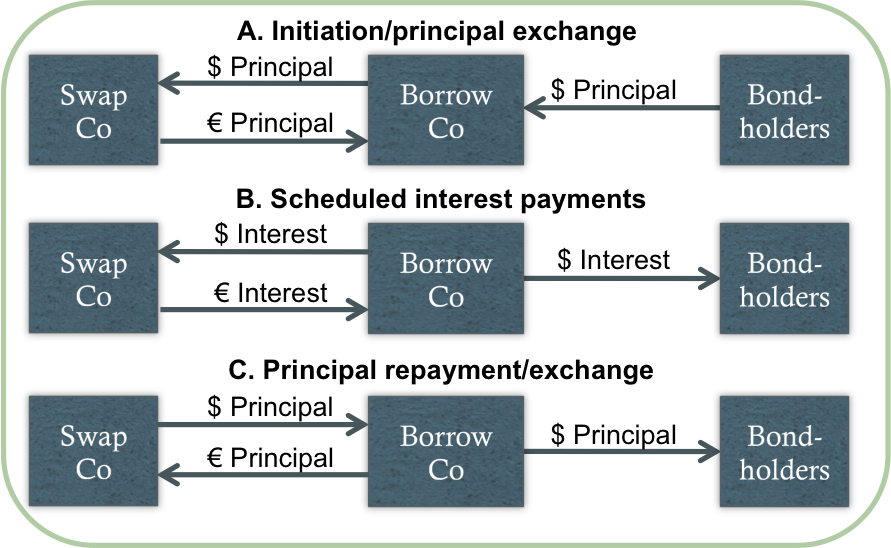

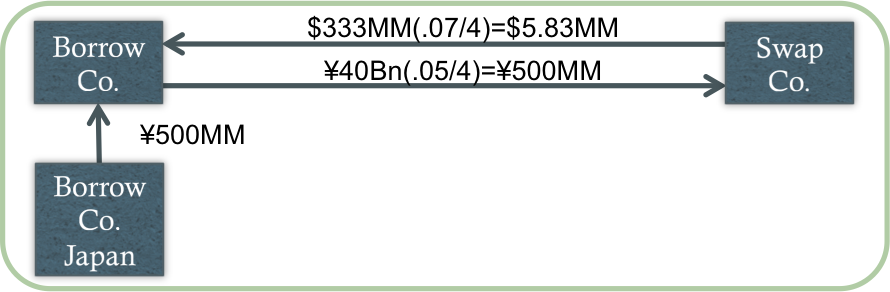

Converting a Loan to Another Currency

Converting Cash Receipts into Domestic Currency

Current spot exchange rate of ¥120/$

Net effect: BorrowCo converts its quarterly ¥500MM into ~$5.83MM at a fixed rate

Managing Dual-Currency Bonds

Diversifying a Concentrated Portfolio

Net effect: InvestCo pays the return on XYZ stock and receives the return on the specified index

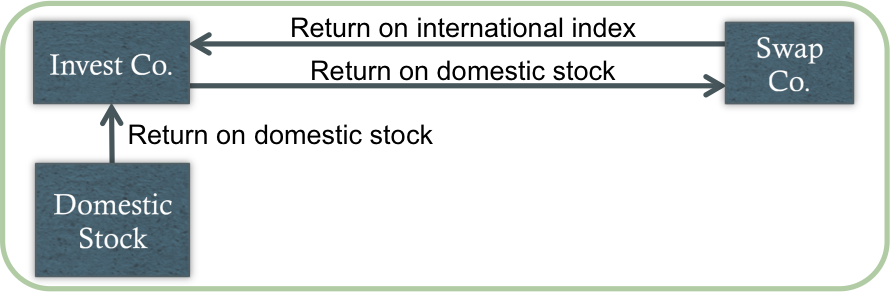

Achieving International Diversification

Net effect: InvestCo earns the return on the domestic stock and enters a swap paying that domestic return and receiving the return on an international index

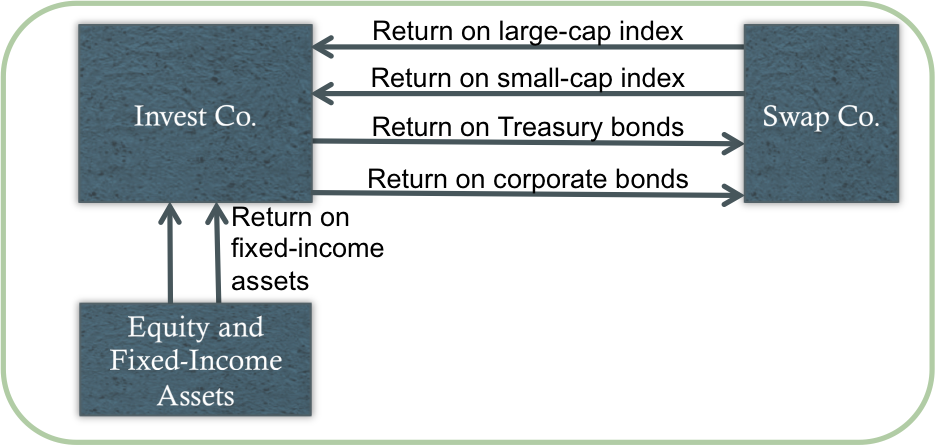

Changing Asset Allocation

Net effect: InvestCo changes its asset allocation to weight equities more heavily

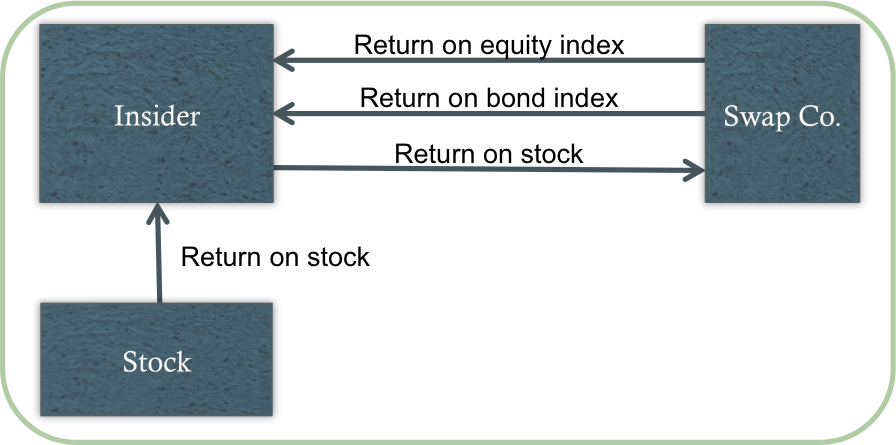

Reducing Insider Exposure

Net effect: The insider effectively sells his exposure and receives a return of an equivalent amount in equity and/or bonds

Swaptions

Payer vs. receiver swaptions

American vs. European swaptions

Strategies/applications:

Anticipating future borrowing

Terminating a swap

Synthetically removing (adding) a call feature in callable (noncallable) debt