Education Budget

Recommendations

While school boards control much of the educational, organizational, and financial operations of school districts, local governments can guide districts toward maintaining an efficient, responsive, and high-performing public school system.

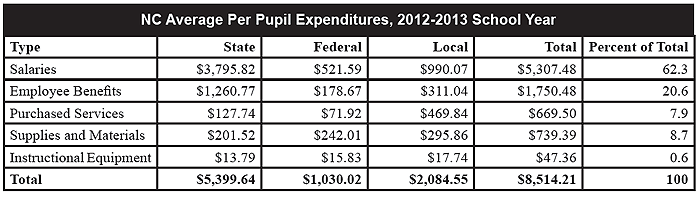

Local governments should closely monitor county appropriations to school districts and measure the effectiveness of the funding. For the 2012-13 school year, local governments in North Carolina allocated nearly $3 billion — an average of $2,085 per pupil — in county appropriations, supplemental taxes, and other revenue sources for public schools. Given the amount of money involved, local government officials have the responsibility to monitor and hold school boards accountable for the use or misuse of local tax dollars allocated to school districts.

|

Local governments should pay special attention to spending on school district personnel. Salary and benefits for school personnel represent the largest single category of expenditures by local government in North Carolina. Collectively, local governments spent $1.4 billion on salaries and benefits for school personnel last year, accounting for approximately 60 percent of their total expenditures on public education. The use of local funds for the salaries and benefits of teachers, administrators, and other personnel should be closely tied to various performance measures as well as adjusted to reflect yearly enrollment changes.

Specifically, school systems should use outcome-based measures, including test scores and value-added analyses, to reward the efforts of successful teachers and administrators. An incentive pay program that utilizes local funds should also be adopted to attract highly qualified science, mathematics, and special education teachers to low-performing schools.

Local governments should ensure a transparent public school budget process. All budget reports and documents used in the public school budget process should be complete, accurate, and relatively free of jargon, acronyms, and technical language. Moreover, taxpayers should be able to access and download all budget documents quickly and easily from a local government website.

Local governments should revise the budget process to include a host of quantifiable or measurable goals and specific strategies used to achieve those goals. The state and federal governments provide several measures of student achievement, but not enough information to anyone attempting to determine whether a school district uses its local funding to increase student achievement.

As part of the budget process, local governments should require school districts to supplement state and federal data with annual studies, audits, and surveys, providing a comprehensive assessment of school district performance. These data would provide measurable goals to form the basis of a sound budget process that ultimately determines whether school districts spend local tax dollars productively.

Background

"Money and buildings" is one way to describe the two primary responsibilities of local governments when it comes to the district schools in their jurisdictions. State law also directs local governments to oversee school district consolidations and mergers when they occur.

Arguably, the most important function of local government is determining how much local tax revenue to appropriate to public schools. County funding makes up a sizable portion of public school budgets. Approximately 25 percent of total spending on public education in North Carolina comes from local sources.

Analysis

On the local level, the public school budget process takes at least two months to complete. School district budgets must be presented to boards of education by May 1 and approved budgets must be forwarded to county commissions by May 15 or on a date agreed upon by both parties. County commissions must approve appropriations to the public school entities in their jurisdictions by July 1 or on a mutually approved date.

During budget deliberations, state law allows county commissioners to examine all documentation, reports, and other information bearing on the financial operation of the recipient school districts. Commissioners may also itemize their appropriations by purpose, function, or project so long as they follow the uniform budget format.

There is no statutory language that specifies how much county commissions should appropriate to school districts, but state law does not obligate commissions to fund deficits incurred by school systems. Rather, budget decisions are left to the discretion of county commissions. General Statute 115C-426(e) states,

The local current expense fund shall include appropriations sufficient, when added to appropriations from the State Public School Fund, for the current operating expense of the public school system in conformity with the educational goals and policies of the State and the local board of education, within the financial resources and consistent with the fiscal policies of the board of county commissioners.

To fulfill this requirement, state statute encourages, but does not require, boards of education and county commissions to conduct joint meetings and develop common strategic plans. It may be advantageous for a school board and county commission to agree on a funding formula that takes inflation, student enrollment, and other factors into account. This requires two safeguards. First, the formula must be sensitive to fluctuations in local tax revenues and changes to state and federal appropriations. Second, it must consider that district expenditures are dependent on the student populations that they serve, e.g. legally mandated services for special needs students often require additional funds. Student characteristics should be an integral part of the formula.

The budget process does not necessarily conclude when a county commission agrees on an appropriation for a public school district. If a board of education objects to a budgeted amount, it may compel a county commission to participate in a joint meeting and, if no resolution is agreed upon, mediation. If mediation fails, the issue is settled in the courts.

Some advocacy groups would like to discard this process entirely. The North Carolina School Boards Association (NCSBA) has long been a champion of granting school districts taxing authority or so-called "fiscal independence." They argue that the system of funding schools through county commission appropriations is obsolete, as over 90 percent of school districts nationwide have the power to set tax rates. The NCSBA further contends that granting school boards taxing authority would increase accountability, enhance local control, remove politics from education, and save taxpayers time and money. On the other hand, those who believe in granting "fiscal independence" to school boards fail to acknowledge the critical role of the county commission in apportioning scarce resources to meet the demands of multiple local government entities.

Analyst: Dr. Terry Stoops

Director of Education Studies

919-828-3876 • tstoops@johnlocke.org

The entire 2014 City & County Issue Guide, is available for download as a 3.6MB Adobe Acrobat file.

The free Adobe Acrobat Reader is required to view or print this document.

|