With Product Growth Outpacing the Entire Industry’s

By Matthew Carr, Emerging Trends Strategist, The Oxford Club

Dear Reader,

When our dishwasher went belly up after the holidays, I didn’t mind being forced to wash dishes by hand.

My father owned and operated a number of restaurants in his life. And my siblings and I worked various jobs at them growing up.

So I was standing at the kitchen sink, doing dishes and letting my mind wander where it so often goes: technology.

Anyone who’s followed my work over the years knows I’m a fan of science fiction humorist Douglas Adams. But Adams was also a technology and innovation advocate.

He penned essays about technology and our relationships with it. And he was the one who laid out three rules that govern our view of new innovations.

First, everything that’s already in the world when you’re born is normal. For most of us, that includes cars, computers, planes, televisions... all that humdrum stuff.

Second, anything that gets invented between the time you’re born and before you turn 30 is incredibly exciting and creative. If you’re lucky, you can make a career out of it.

And third, anything that gets invented after you’re 30 is against the natural order of things. It’s “the beginning of the end of civilization as we know it,” in Adams’ words.

That is, until it’s been around for about a decade. Then we realize it’s actually quite all right and it’s hard to remember a world without it.

The point is we’re often hurt by our own skepticism when we underestimate the potential of new technology. In investing, that skepticism can cause us to undervalue a new opportunity... and that can be costly.

Now, I’m sure when the dishwasher was invented, there were plenty who saw “the end of days” on the horizon. Those same people probably passed on Whirlpool (NYSE: WHR).

The same is probably true for Apple (Nasdaq: AAPL). And those people missed out on the first $1 trillion company.

Well, the company I’m highlighting this month has been at the forefront of a technological revolution multiple times. But it has also found itself guilty of Adams’ third rule – being skeptical of new advances and underestimating their potential.

Because of that, it has died multiple deaths.

But today it’s found new life on the cutting edge in an industry so many investors continue to underestimate.

The Rise, Fall and Rise Again of a Giant

There are two things people tend to think about when they think of Microsoft (Nasdaq: MSFT).

The first is Bill Gates. It’s almost impossible not to.

The bespectacled company founder has been one of the wealthiest men on the planet for decades. And he is the de facto face of Microsoft, even though he hasn’t been CEO since 2000 and has worked only part time as a technology advisor since 2006.

The second thing people think of is a laundry list of failures.

We all have a personal connection to Microsoft, via PC, Windows, Xbox or myriad other products. Needless to say, we’re well-acquainted with the times the company burned or frustrated us.

Not to mention when a tech giant trips, it doesn’t go unnoticed. Crowds gather.

The boisterous Steve Ballmer was at the helm of the company from 2000 to 2014.

And his more than decade-long tenure was rife with notorious missteps, including his infamous quip in a 2007 interview, “There’s no chance that the iPhone is going to get any significant market share. No chance.”

But that wasn’t the first time Apple embarrassed him. When the Silicon Valley darling took the MP3 market by storm with its iPod, Microsoft fired back with its own offering, the Zune.

The Zune was such a complete, enormous and laughable disaster that it’s earned cultlike status.

Not to mention Microsoft’s mobile phones in the early 2000s fell flat.

Couple those misses with a slew of high-profile operating system failures – Windows ME, Windows Vista, Windows Ultimate, etc. – and Microsoft found itself with a real image problem.

But here’s the deal...

At every great advance, Microsoft was there before most everyone else. It either didn’t rise to the occasion or was so far ahead of its time that it was doomed to fail.

A decade before Facebook (Nasdaq: FB), there was Microsoft’s MSN. Before Skype, back in the 1990s, there was Microsoft Portrait. Of course, Skype is commonplace today and owned by Microsoft.

Before we had Alphabet’s (Nasdaq: GOOG) Google Earth, there was TerraServer. This was also a brainchild of the mid-’90s.

And before the iPad, there was the Windows XP Tablet, Origami and the dead-on-arrival Courier. Gates spoke about tablet PCs in 2000.

The fact is the company was well ahead of its time with most of these products. And they were shut down or discontinued before today’s household names gained steam or even hit the market.

But thankfully, the days of Ballmer are in the past. Satya Nadella took the reins in 2014. Almost immediately, Microsoft was redefined.

He sent a memo to employees stating that Microsoft was going to be “the productivity and platform company for the mobile-first and cloud-first world.”

And that’s what it’s done. More importantly, it’s back on top of the industry, as well as the markets.

Profits for the Whole Family

Microsoft isn’t some unknown name to investors. It’s ubiquitous across a broad spectrum of products.

Revenues from these are funneled into a relatively even split between three segments: Intelligent Cloud, Productivity and Business Processes, and More Personal Computing.

In the company’s fiscal year 2019 first quarter, total revenue increased 19% year over year to $29.1 billion.

The Productivity and Business Processes segment, which includes Office 365 subscriptions, grew 19% to $9.8 billion. LinkedIn, which Microsoft bought in 2016, contributed 33% revenue growth here.

In its Intelligent Cloud division, servers and cloud services revenue surged 28% to $8.6 billion. But Microsoft’s Azure cloud platform is skyrocketing. Its revenue increased 76%.

In the More Personal Computing segment, revenue jumped 15% to $10.7 billion. The big winner was gaming revenue, which soared 44%.

That gaming revenue is helped by Microsoft’s Xbox One X. Xbox sales nearly doubled year over year. Plus, its Xbox software and services revenue jumped 36%.

The number of monthly active users for its Xbox Live subscription also ticked 8% higher to 57 million. Meanwhile, Office 365’s total number of subscribers increased 16% to 32.5 million.

By 2020, more than 80% of software vendors will switch to a subscription-based model. A lot of that has to do with the success Microsoft and other early adopters of the model have enjoyed.

Beyond that, Microsoft is making waves on the hardware side with its Surface tablet.

Football fans know these dot the NFL sidelines. Every Sunday, coaches and players review plays on the bright blue tablets. But mainstream consumers are gobbling them up as well.

In the third quarter, Microsoft moved into the top five best-selling PCs behind Apple. That shows its hardware sales are gaining momentum.

Overall, the company is firing on all cylinders.

For the year ahead, revenue is projected to increase nearly 12.5%. It should continue to move higher in 2020...

But I think we could see Microsoft top expectations. And that has to do with one of my favorite industries to cover: the cloud.

Two-Horse Race Into the Cloud

There was a time when Microsoft was viewed as a monopoly that needed to be broken up.

Even today, it’s not hard to imagine why.

Microsoft’s goal is to be everywhere. To be the epicenter of every home.

And it’s made strides to embed itself in every facet of our lives.

Our PCs and smartphones run Office 365. (I mean, what sort of anarchist – besides the Mac-owning Adams – doesn’t use Microsoft Word?!)

The Windows operating system is used on 9 in 10 computers on the planet. The company’s Xbox video game console is in tens of millions of homes.

Through that console not only can you play video games locally or online, but you can also buy video games and movies, and connect to Amazon, Netflix and Hulu. Plus it has a host of other functions.

In offices, Microsoft is again on PCs. I’ve never met a company that doesn’t rely on Excel, let alone PowerPoint.

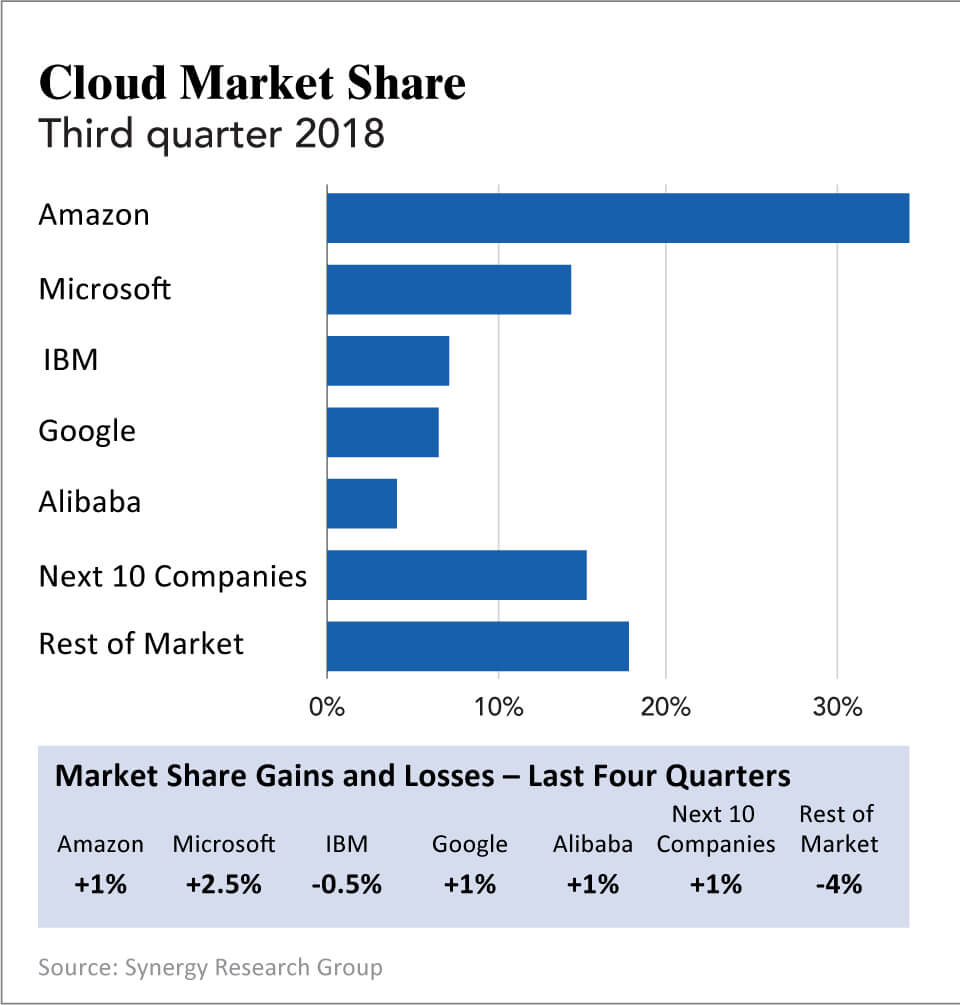

But Microsoft’s secret weapon is the cloud. And here, Microsoft Azure is gaining on the big dog, Amazon Web Services (AWS).

In the third quarter, total spending on cloud infrastructure services increased 45% to $17 billion. But Microsoft Azure’s growth outpaced the overall growth of the industry.

Now, AWS controls 34% of the cloud services market. Microsoft is a distant No. 2.

But there’s huge demand for the cloud.

And at this point, those service providers that aren’t in the top five are going to have to focus on niche markets. They simply can’t compete.

At No. 3, IBM (NYSE: IBM) is already starting to falter. And the next 10 largest cloud infrastructure service providers outside of the top five saw their market shares slip in the third quarter. Meanwhile, the rest of the market saw its share decline 4%.

Microsoft is winning out and making strides. At this point, it’s becoming a two-horse race between Microsoft Azure and AWS.

Microsoft doesn’t need to beat Amazon. It just needs to continue to steal market share from the lower rungs.

No doubt about it, Microsoft is a behemoth. But it’s become a fit and focused behemoth under Nadella.

Revenue is growing double digits... Earnings are growing double digits...

And the Azure cloud platform’s growth is even faster than the explosive growth of the cloud industry.

Microsoft shows attractive growth for a company its size. But in a market as volatile as the one we’ve recently seen, its ability to weather storms and offer a nearly 2% yield is just as important.

Not only is Microsoft gaining on Amazon in the cloud. But it’s also surpassed Apple and Amazon as the largest publicly traded company by market cap.

This isn’t the time to be a skeptic. It’s time to be a believer.

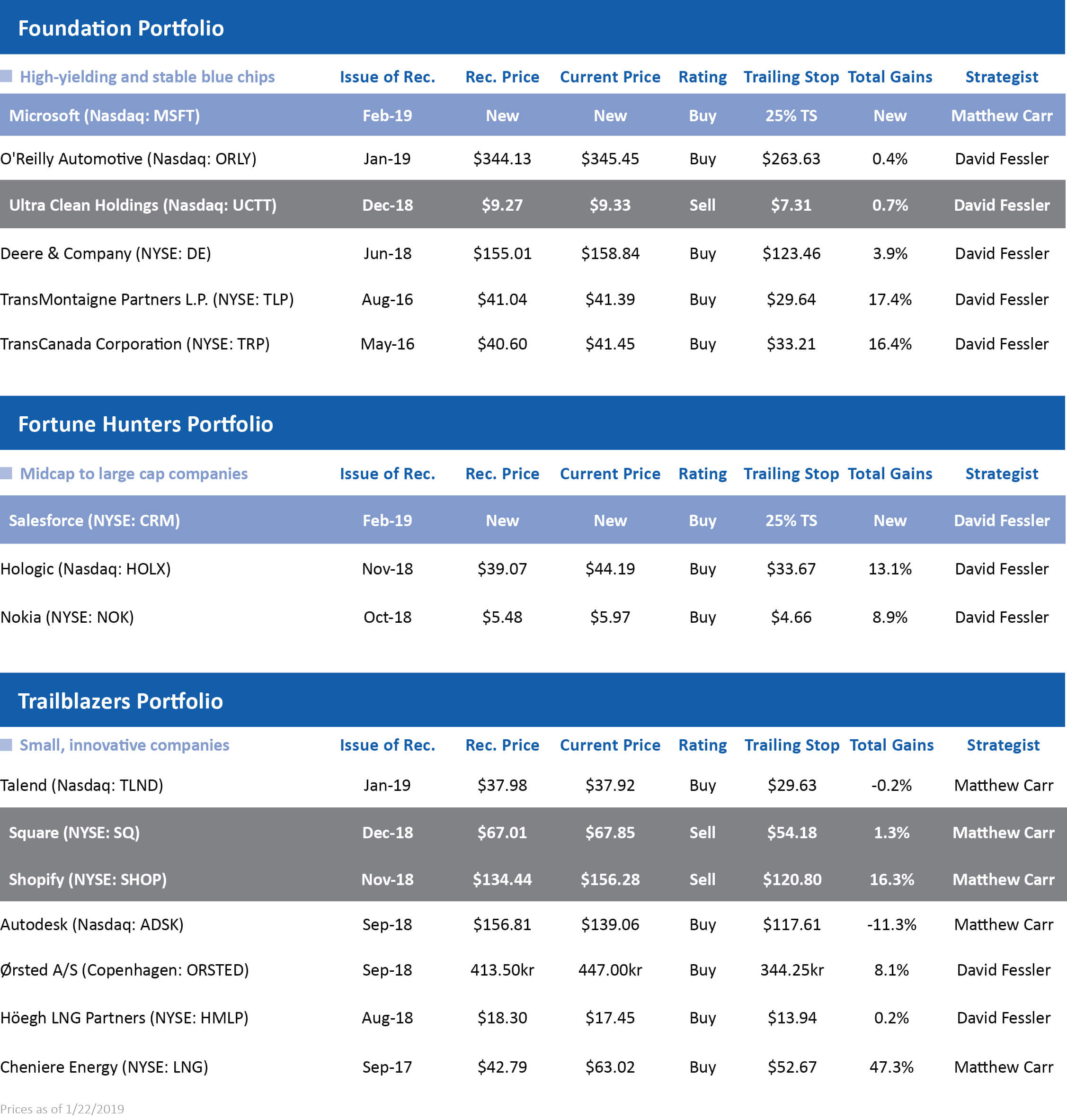

Action to Take: Buy Microsoft (Nasdaq: MSFT) at market. Immediately place a 25% trailing stop to protect your principal and your profits. This is a perfect fit for our Foundation Portfolio.

Heard it here first

The Three C’s of Successful Investing

By Matthew Carr, Emerging Trends Strategist, The Oxford Club

During my career, I’ve learned to rely on a systematic approach to investing. This has led to my record-breaking successes.

It’s also why I developed my basic criteria for finding the next life-changing stock. I call them my three C’s: Connectivity, Content and Community. These criteria apply to any company that relies on the modern consumer.

An increasing number of consumers are shopping online. Every quarter, brick-and-mortars struggle and e-commerce companies soar. This is where Connectivity is key.

At the same time, retailers are increasingly relying on social media. Many of today’s most successful ad campaigns involve “shareable” Content, whether it’s a viral video or public endorsement from a celebrity. Companies that don’t embrace these new platforms are virtually guaranteed to lose market share.

Finally, in the social media age we’re in, consumers are even more loyal to the brands they enjoy. Smart retailers are leveraging these Community relationships and turning them into sales.

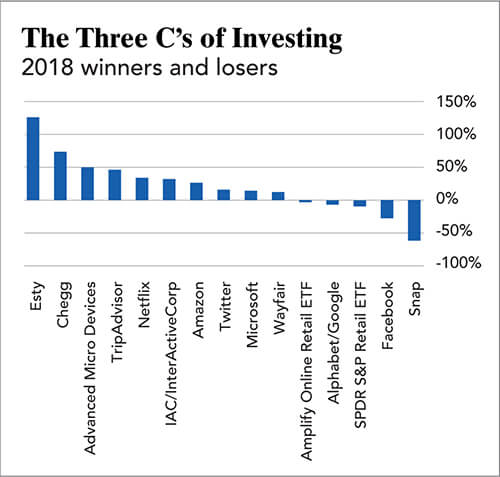

Last year was the worst year for the markets in a decade. But stocks that embraced my three C’s largely outperformed.

Etsy (Nasdaq: ETSY) gained more than 125%. Chegg (NYSE: CHGG) spiked more than 72%. Advanced Micro Devices (Nasdaq: AMD) finished the year up nearly 50%, despite the tech sell-off. As did TripAdvisor (Nasdaq: TRIP).

At the other end of the spectrum, Amplify Online Retail ETF (Nasdaq: IBUY) shares ended 2018 down a little more than 4%. But that was half of what traditional retail’s SPDR S&P Retail ETF (NYSE: XRT) lost.

Snap (NYSE: SNAP) lost more than 62% in 2018 in a losing battle against Facebook and Twitter. For most of us, the internet is simply a fact of life at this point. But the swift and massive shift online still caught retailers off guard.

I know from years of covering the sector that it’s always been a fickle beast. Brands go in and out of favor, and consumer tastes evolve.It’s sad that so many retailers are headed the way of J.C. Penney and Sears. But for investors looking to avoid those pitfalls, my three C’s can be their guide.

The best companies will use a variety of the three criteria to drive double-digit increases in revenue. And that means they’ll likely succeed, even in down years.

THE DIGITAL TRANSFORMATION

Right Place, Right Time, Right Product

How One Company Is Transforming Cloud Computing Software

By David Fessler, Energy and Infrastructure Strategist, The Oxford Club

I started my sales career back in 1980, working for a semiconductor electronic test equipment company.

All I had at work back then was a desktop phone, fax machine, copier, computer and printer.

But it quickly became clear to me that I needed software to help keep track of all kinds of things – customer contacts, quotes, orders and (most importantly) commission payments.

Today, customer relationship management (CRM) software does all this.

But back in 1980, it didn’t exist... at least not at a reasonable price.

So I developed my own CRM software using a program called FileMaker.

It worked great, but – like all software – it needed constant tweaking and updating.

I allowed other salesmen to use it, and they loved it.

After a few weeks, I started getting emails by the dozens with suggestions for new features.

Eventually, I was promoted to vice president of sales.

So I turned over management of my CRM software to our IT department.

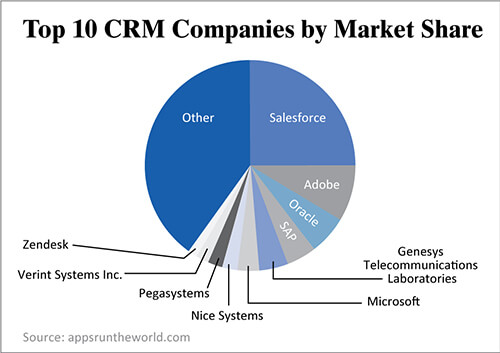

Now here we are in 2019, and there are dozens of CRM platforms and software packages companies to choose from.

Here are the top 10 CRM companies by market share.

But only one is considered the top gun. And that’s the one I’m adding to our Fortune Hunters Portfolio today.

The Digital Transformation

Today, companies are increasingly making the “digital transformation.”

In short, that means moving every single business platform into the cloud. Digital transformation initiatives are a priority for many companies trying to stay current.

By 2020, 60% of business enterprises will have a digital transformation platform strategy. And 90% of all companies will use more than one cloud platform or service.

So the opportunities for CRM are incredible. Today, the total available market for enterprise software is estimated at $140 billion.

But if software isn’t easy to use, widespread adoption won’t happen.

That’s where Salesforce (NYSE: CRM) fits in. Based in San Francisco, Salesforce is helping its customers take that digital transformation leap.

The company builds enterprise cloud computing software solutions, with the widest and deepest product offerings in the industry.

On Cloud Nine

Like many companies today, Salesforce has made all of its software cloud-based.

Its Sales Cloud, Marketing Cloud and Service Cloud platforms are comprehensive and enable customers to perform day-to-day business tasks with ease and efficiency.

In 2017, it increased its market share and revenue by more than any other CRM company, including Oracle, SAP and Adobe. Today, its share of the $27.1 billion CRM sector is a market-leading 25%.

In fact, Salesforce has been the No. 1 CRM software vendor worldwide for five years running.

Right now, even medium and small companies are embracing CRM software. And when you look at projected revenue growth, you can see why...

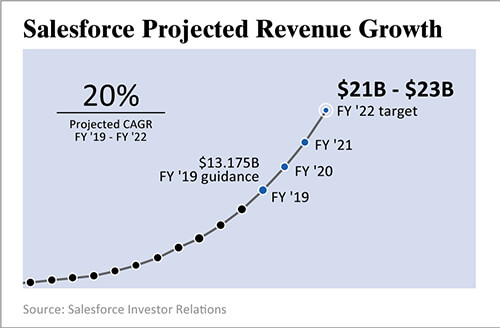

Salesforce is projecting a 20% compound annual growth rate through at least 2022. Others are predicting a $29.7 billion market by 2022.

There aren’t many businesses that have near-term growth curves that look like that.

But CRM is the fastest-growing segment in the enterprise software sector.

And Salesforce just happens to be in the right market at the right time with the right products.

Revving Up Revenue

One of the things I like about Salesforce is that its products are extremely sticky.

That is, once companies start to use them, they can’t stop. They want more.

It’s all incremental revenue. And it all goes right to Salesforce’s bottom line.

In fact, roughly 48% of Salesforce’s revenues in fiscal year 2018 were from new products sold into its existing installed base.

Plus 52% of revenues came from selling product upgrades and adding seats from the installed base.

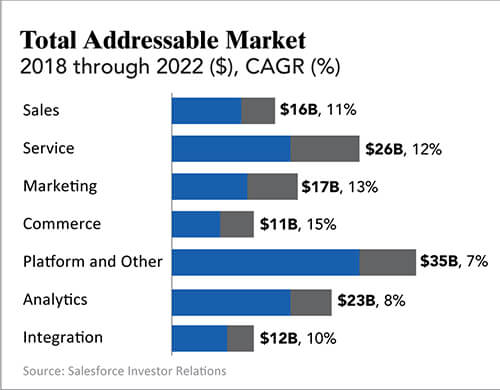

Salesforce’s products address large and growing markets. The following are the company’s top markets, their sizes and their projected compound annual growth rates through 2022.

Salesforce is in a fantastic position. Only 38% of its customers are multicloud, meaning they use more than one of Salesforce’s products.

But 92% of the company’s revenue comes from its multicloud users. So Salesforce is focused on upselling to gain more multicloud customers.

With this kind of growth, Salesforce is on track to be the fastest-growing enterprise software company to hit $20 billion in annual sales. The chart below shows how quickly that could happen.

As I write, Salesforce’s 52-week high is $161.19. Because it’s a quickly growing company, it trades at a high price-to-earnings (P/E) ratio of 151.38. However, I believe the P/E is warranted.

Growth of CRM software sales is predicted to be fast and furious for at least the next four or five years. Salesforce is in a position to profit big-time.

Action to Take: Buy Salesforce (NYSE: CRM) at market. Use a 25% trailing stop to protect your principal and your profits. This company will make an excellent addition to our Fortune Hunters Portfolio.

Dave's New Endeavor...

The Energy Disruption Triangle:

Three Sectors That Will Change How We Generate, Use, and Store Energy

The Energy Disruption Triangle explores the state of U.S. energy from source to consumer. And it provides insight into the three sectors that are changing the world: solar energy, electric vehicles and energy storage.

Order your copy today to...

Learn how our energy supplies – and usage – are changing

Understand why energy storage matters and how the technology is evolving

Explore the history and future of groundbreaking energy technologies

Delve into the disruption of the U.S. energy supply and the possibility of energy independence.

As technology continues to evolve, the nation’s energy habits will experience a dramatic upheaval. Dave’s book provides actionable guidance to help you adapt in the age of the energy revolution.

By Anthony Summers, Senior Research Analyst, The Oxford Club

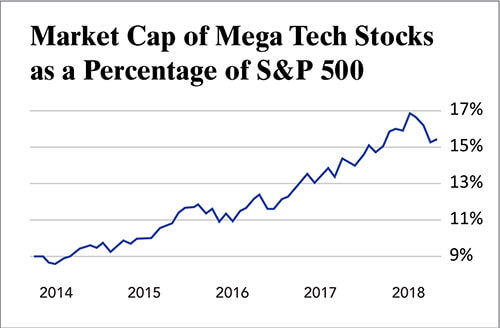

Mega tech stocks have provided investors with extraordinary returns for a decade. In that time, investors have gleefully ridden the coattails of these stocks without much concern that government might intervene.

But government has a history of breaking up businesses that have too good of a thing going.

For instance, at the time AT&T was broken up in the early 1980s, the company controlled about 93% of all phone traffic in the U.S. This lines up with the kind of market dominance we’re seeing today in tech.

Microsoft (Nasdaq: MSFT) dominates the computer operating system space with roughly 75% of global market share.

Apple (Nasdaq: AAPL) owns only about 12% of that space. But Apple’s dominance lies elsewhere.

Apple’s iPhones account for about 39% of worldwide smartphone shipments, but the company brings in more than half of all global smartphone sales revenue.

Monopolies aren’t necessarily bad for consumers. The Sherman Antitrust Act allows for “innocent” market dominance, provided it results from “fair” business practices. Of course, there’s room for interpretation there.

For example, Google parent company Alphabet (Nasdaq: GOOG) owns 81% of online searches. It also dominates 85% of search ad revenue. As such, one company effectively controls access to the internet... and the fate of nearly all businesses that advertise online.

Facebook (Nasdaq: FB) and its subsidiaries own 77% of mobile social media traffic, with more than 2 billion users globally. But concerns over user privacy and how personal data are used has drawn attention.

There’s also the larger debate about the economic impact of mega tech monopolies on small business growth and job creation.

The e-commerce boom has both disrupted and revolutionized the retail space, with Amazon (Nasdaq: AMZN) leading the pack. The company receives nearly half of all online consumer spending and has snatched away market share from even the biggest brick-and-mortar retailers.

If these companies were a small part of the market, things would be different. Instead, mega techs account for a significant portion of the stock market’s total value. In fact, these five stocks alone account for more than 15% of the S&P 500’s roughly $21 trillion value, with a combined market cap of nearly $3.4 trillion.

It’s not a stretch to say that the fate of mega techs determines the fate of the entire U.S. stock market. Therefore, investors should be mindful of the potential political threats that these companies face.

portfolio review

Portfolio Review

Cheniere Energy, Autodesk, Talend and More

By Matthew Carr, Emerging Trends Strategist, The Oxford Club

Energy and optimism are once again in focus. The markets are rebounding from their Christmas Eve lows. And crude prices are surging.

U.S. oil is back over $50 per barrel as OPEC and its allies are reining in output. Of course, the resurgence in global crude prices has lifted the entire energy complex. And we’re enjoying the benefits.

It was only a handful of years ago that the U.S. lifted restrictions on exporting fossil fuels like liquefied natural gas (LNG) and crude oil. America has quickly become one of the largest exporters in the world since then, disrupting the global energy hierarchy. And that’s been fueling gains in our shares of Cheniere Energy (NYSE: LNG).

On top of that, while warmer-than-average temperatures in the U.S. are driving down natural gas prices, the story is the opposite on the other side of the world. Colder-than-normal temperatures have slipped their icy fingers across Asia, the world’s largest LNG market. In turn, Asian LNG spot deliveries hit a new all-time high in December. This was good news for low-cost U.S. LNG exporters like Cheniere.

In 2018, the company inked multidecade supply agreements with Malaysia’s Petronas, Taiwan’s CPC Corp. and China’s China National Petroleum Corp. Currently, Cheniere exports LNG to more than 30 countries. And it supplies a lot of spot market cargos in Asia. The region’s soaring demand isn’t just a short-term blip. I believe Cheniere’s 2019 revenue will jump more than 30%. But LNG isn’t the only industry making headlines.

We also have our additive manufacturing and generative design play, Autodesk (Nasdaq: ADSK).

In December, the software company completed its acquisition of construction software provider PlanGrid. It also gobbled up another construction platform, BuildingConnected. That’s doubling down on an industry that gets little attention.

But here’s why these deals are great news for us. These two platforms are being folded into Autodesk’s BIM 360 construction software suite.

By 2020, Autodesk forecasts its design- and construction-related opportunities will top $22 billion. Not to mention the global construction industry will need to add 200 million jobs over the next decade to keep up with demand.

A one-stop shop for design and project management like Autodesk’s BIM 360 is poised to win out big. Already, in just three years, subscriptions for BIM 360 have increased more than tenfold.

Today, 68% of Autodesk’s revenue comes from subscriptions. And revenue is increasing more than 25% year over year each quarter. I think revenue will increase more than 23.5% in 2019 and then jump nearly 27% in 2020.

Then there’s Talend (Nasdaq: TLND). Our cloud data analytics play gave preliminary fourth quarter revenue guidance of $55.4 million to $55.8 million. That’s good for 33% to 34% year-over-year growth. But it was lower than the $56.6 million to $57.4 million guidance it previously provided.

Now, subscription revenue is still cranking higher by between 37% and 38%, and it makes up the majority of Talend’s business. The slowdown is in Talend Professional Services.

I think the stumble from Professional Services is short term. I believe Talend is poised to have an extremely profitable 2019.

From the Desk of David Fessler

There’s been a lot of buzz lately about the world’s next-generation communications platform: 5G.

5G is going to completely revolutionize how we communicate with each other and everything else.

Ever since 5G was announced, the race has been on to see which mobile carrier will announce this capability first. Verizon started pitching it last fall, and AT&T began an ad campaign soon after.

But, in my opinion, the best way to play the 5G space is Nokia (NYSE: NOK). We are in early with Nokia. But we are already up 8.9%... and the real rush to 5G hasn’t even started. I think Nokia could be an eventual 10-bagger. So now is a great time to accumulate shares.

Another sector I have my eye on of late is the natural gas sector. One of the recommendations we have is America’s largest LNG producer, Cheniere Energy.

However, we also have an LNG shipper, Höegh LNG Partners L.P. (NYSE: HMLP). The company is growing rapidly. It increased revenues 4% year over year and its diluted earnings per share by more than 600% in the last quarter.

Höegh recently signed a long-term charter with Australian energy retailer AGL. It plans to lease floating storage and regasification units to liquefy natural gas at the plant at Crib Point in Victoria.

I like Höegh for its stable business model. Plus, what’s not to like about a forward dividend yield of 10.29%? If you are an income-oriented investor, Höegh belongs in your portfolio.

It’s windy here today in Pennsylvania, and that brings up another company I like: Ørsted A/S (Copenhagen: ORSTED).

In the U.S., offshore wind is just getting started. So Ørsted – with its decades of experience building and operating offshore wind farms – was a logical choice for projects in New England.

The company has a construction pipeline in New England that already totals 830 megawatts. Most of its current backlog is in projects off of Rhode Island’s and Connecticut’s shores. I believe Ørsted is the best way to play the coming boom here. n

The Oxford Club’s 21st Annual Investment U Conference

Announcing Our Keynote Speaker: Walter Cruttenden

The Oxford Club is excited to announce one of our keynote speakers for our 21st Annual Investment U Conference, fintech innovator, author and researcher Walter Cruttenden.

Cruttenden founded and served as CEO of Roth Capital, a leader in funding emerging growth companies since 1983. He also founded and served as CEO of the investment banking arm of E-Trade, which became the No. 1 provider of online IPOs before its sale. Walter then co-founded Acorns, the first and largest micro investing platform, with 4.5 million accounts opened to date.

In addition to Cruttenden, Matthew, David and the rest of the Club’s strategists will present to attendees.

Don’t wait to secure your seat for this exclusive event at the Vinoy Renaissance Resort & Golf Club in St. Petersburg, Florida, this coming March 28-30. Please visit us here.