Our New “Dividend Aristocrat”

The Best MLP Is Not an MLP

Dear Member,

In life, it pays to be flexible, open and optimistic.

A family friend was once stood up on a blind date. Rather than go home and sulk, he stayed at the bar and met his future wife as they were both waiting in line for the restroom.

When I was a toddler, my parents were house shopping. The realtor had to drop something off at a house she didn’t think my folks would be interested in. I grew up in that house. My parents lived there for 34 years, and the sellers are our family’s closest friends.

As a college student, I missed an interview for a public relations position with a minor league baseball team because my car broke down (there were no cellphones back then). A friend drove me to the interview an hour late.

The hiring manager had already left. It was thundering outside, so they let me stay in the small office until my ride returned. Another manager talked with me while I waited. He hired me to be the team’s radio announcer.

So I have learned to be open to opportunities that are different from the ones I am looking for.

A few weeks ago, I started to believe it was time to get back into master limited partnerships, or MLPs. These companies, which are mostly pipeline businesses, offer great yields and tax-deferred income – so I thought I would choose an MLP for this month’s recommendation.

As I was digging into the research, there was one pipeline company that stood well above the rest.

It has a 6% yield, and it has raised its dividend for 24 years in a row. The dividend has increased at a double-digit annual rate for the past decade.

The only thing is it’s not an MLP.

In fact, the company acquired its two MLPs late last year when MLP prices got hammered. It was able to scoop them up at a bargain and keep all that cash flow for itself.

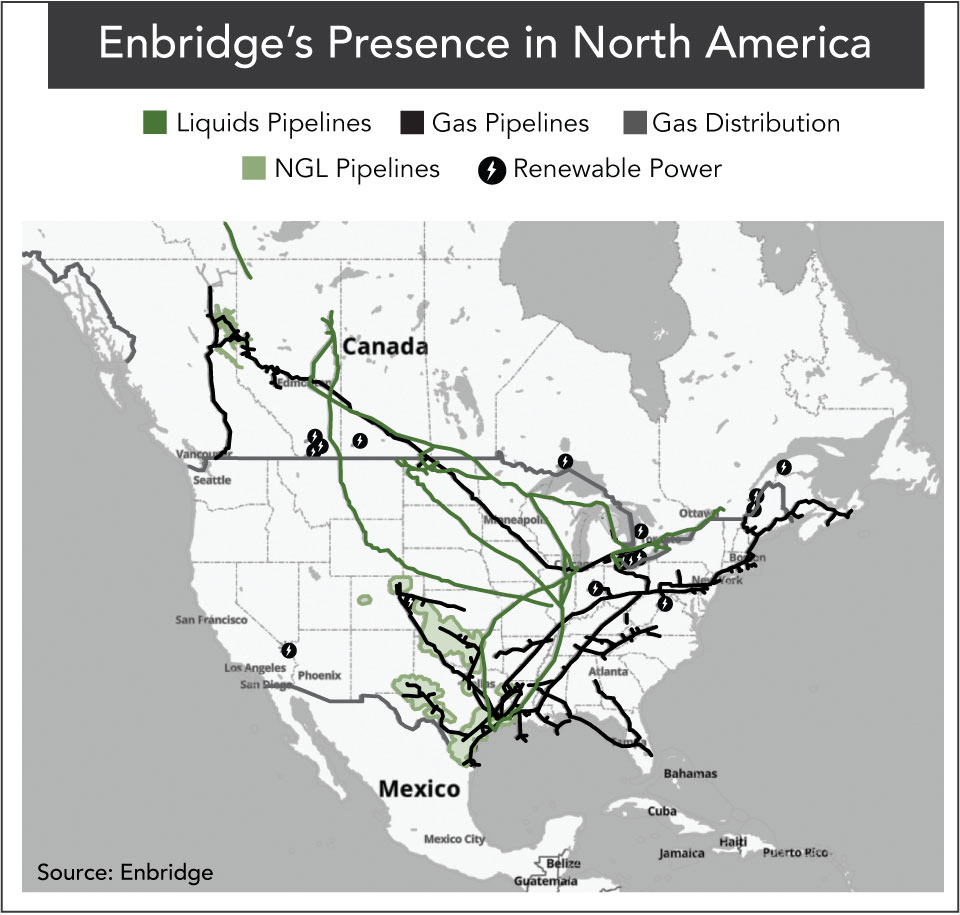

Enbridge (NYSE: ENB) owns and operates Canada’s largest pipeline. It transports oil from the oil sands in Western Canada across North America all the way down to the Gulf Coast. Eight of Canada’s 10 largest oil producers use Enbridge’s pipeline.

The company also has natural gas pipelines and is Canada’s largest natural gas distributor. It transports 25% of North America’s crude oil and 18% of its natural gas.

The stock dipped in early March after a pipeline expansion expected to come online at the end of the year was delayed until the second half of 2020. This expansion will add 400,000 barrels per day to the oil coming out of Canada.

Fantastic Financials

I’m a big fan of the company’s business model. Enbridge’s management and pipelines are considered the best in the business, but it’s the company’s financials that are especially enticing.

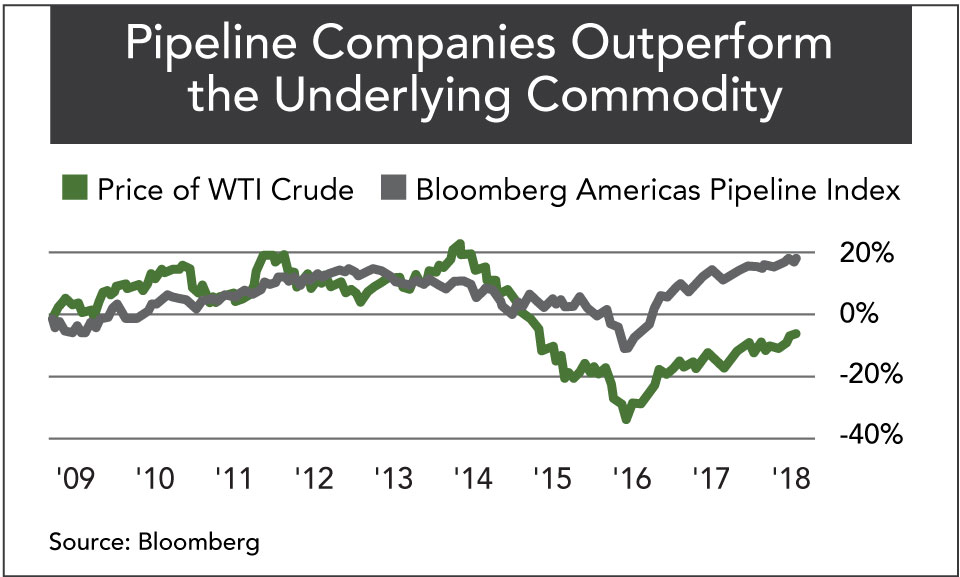

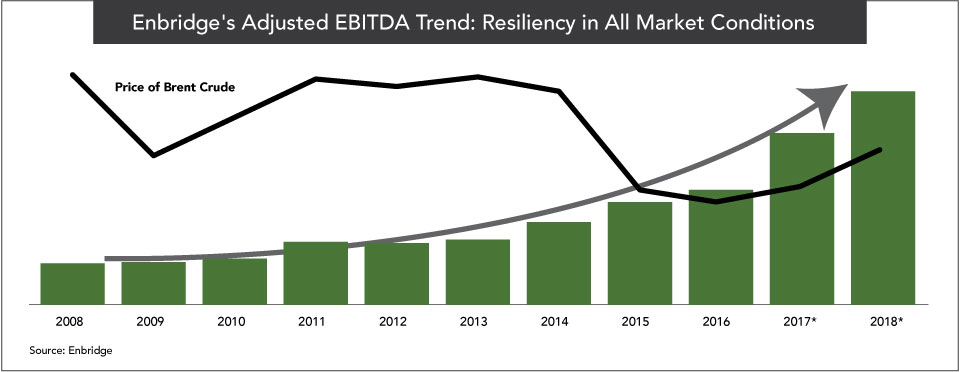

What’s most impressive is that Enbridge has grown its business regardless of the price of oil.

You can see in the chart below that even during the Great Recession and oil price collapse, Enbridge grew its EBITDA (earnings before interest, taxes, depreciation and amortization).

That’s because Enbridge doesn’t sell oil – it transports other companies’ oil and gas products through its pipelines, collecting a contracted fee every time, whether oil is trading at $30 or $100.

Enbridge is executing on $11 billion in secured contracts, and it has another $2 billion in future opportunities after 2020.

In 2018, distributable cash flow (DCF) grew 35% to CA$7.6 billion.

Management said that DCF per share should rise 12.5% in 2020 and 5% to 7% after 2020.

Matched by just two other companies, Enbridge has the highest credit rating in the industry.

Dividend Growth Galore

The company has set a target dividend payout of less than 65% of DCF, which gives me confidence that it can continue to fund and raise its dividend even if DCF falls at some time in the future.

In the first quarter of this year, management raised the dividend by 10%, and it expects to do the same in 2020.

If it does increase the dividend next year, it will be for the 25th year in a row. That would qualify Enbridge for the prestigious Dividend Aristocrats designation – if it were a member of the S&P 500.

Enbridge is a Canadian company, so it is not eligible for inclusion in the S&P 500. Nevertheless, the current 24-year streak – soon to be 25-year – is impressive, Aristocrat or not.

The company recently suspended its dividend reinvestment plan, which means you cannot automatically reinvest your dividends directly with the company.

But as I usually suggest, investors are better off reinvesting their dividends through their brokers anyway (see my article on Page 6 for reasons you shouldn’t).

I confirmed with many of the largest discount brokers that you can automatically reinvest your Enbridge dividends with them.

Because Enbridge is Canadian, U.S. investors will automatically have a 15% tax taken out of their dividend payments by the Canadian government.

If you hold the stock in a taxable account, you will receive a tax credit from the IRS for the amount paid to Canada.

If you hold the stock in a tax-deferred account, you will not be able to claim that credit.

If you are outside of the United States, your tax situation will depend on your taxing authority and any agreement it has with Canada.

Like when my job search got derailed and I found a better opportunity, I was looking for an MLP but instead found the best pipeline company on the market.

Announcing games on the radio for the Albany Yankees was one of the most fun jobs I’ve ever had.

If the Enbridge position works out half as well, the income and stock price appreciation will make it one of your favorite stock holdings in your portfolio.

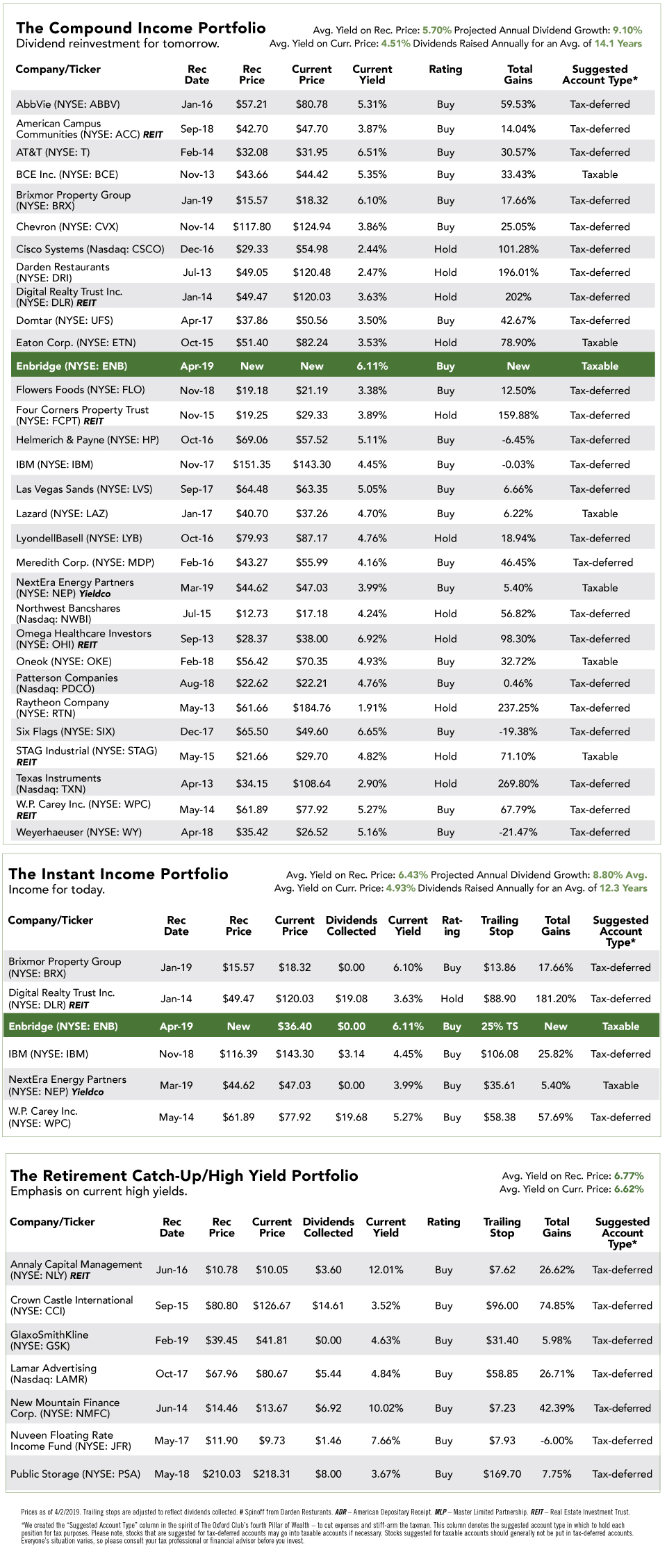

Action to Take: Buy Enbridge (NYSE: ENB), and add it to the Instant Income and Compound Income portfolios. Place a 25% trailing stop on the stock if you’re holding it in the Instant Income Portfolio (no dividend reinvestment). I recommend holding the stock in a taxable account in order to receive the foreign tax credit from the IRS. n